By Preserve Gold Research

It’s easy to mistake China’s digital yuan for just another payment app, the kind that slips into daily life without much notice. The surface resemblance is there. People scan codes, funds move instantly, and the experience feels familiar. But that framing misses the deeper shift underway, one less about convenience and more about control, structure, and the reshaping of how money itself is defined.

The ambition behind the project becomes clearer when you step back and look at the language surrounding it. Officials don’t describe the digital yuan as a feature or a product. They describe it as infrastructure, something closer to a foundation than an add-on. That framing carries implications beyond design, extending into how the system is governed and controlled.

As Agustín Carstens, general manager of the Bank for International Settlements, argued in IMF discussions, central banks would retain “absolute control on the rules and regulations” governing the use of digital currency. Analysts who have followed the rollout closely tend to reach a similar conclusion, noting that the system is being positioned as a new layer within both domestic finance and the broader international order.

That distinction matters. Payment tools come and go, shaped by user preference and competition, while infrastructure tends to persist, shaping everything built on top of it. In that sense, the digital yuan begins to look less like a rival to existing apps and more like an attempt to redraw the lines beneath them. For individuals and institutions alike, that raises a quieter question: where does value sit when the systems governing money become more tightly defined?

From Digital Cash to a State-Linked Deposit System

The shift became clearer with reforms that took effect at the start of 2026. What was initially framed as digital cash was redefined into something closer to a deposit system. That may sound technical, but it meaningfully changes the instrument’s character. Instead of sitting outside the banking system, the digital yuan now lives inside it, linked to balance sheets and interest rates.

There’s a certain pragmatism in that move. Earlier versions raised concerns about pulling deposits away from banks, a dynamic that could have introduced instability over time. By bringing the digital currency back into the banking structure, policymakers avoided that tension. The system no longer competes with banks for funding. It reinforces them.

Yet the change also blurs categories that once felt settled. If the digital yuan behaves like a bank deposit, earns interest like one, and sits on a bank’s balance sheet, what distinguishes it from traditional money? The answer lies not in what it is, but in what it allows.

Programmability and the Quiet Expansion of Policy Power

Programmability is often cited here, though the term can feel abstract until you consider its implications. Payments that execute automatically when certain conditions are met. Funds that can be directed, restricted, or timed with precision. These are not features most people think about when they tap a screen, but they introduce new possibilities into the system.

Those possibilities become more concrete when you move from abstraction to application. A payment that only clears if it’s spent within a defined time window. A subsidy that can be used only within a specific sector, such as housing or energy. Transfers that arrive with embedded conditions, shaping not just how much is spent, but where and when. These aren’t distant hypotheticals. They extend capabilities already being tested in controlled environments.

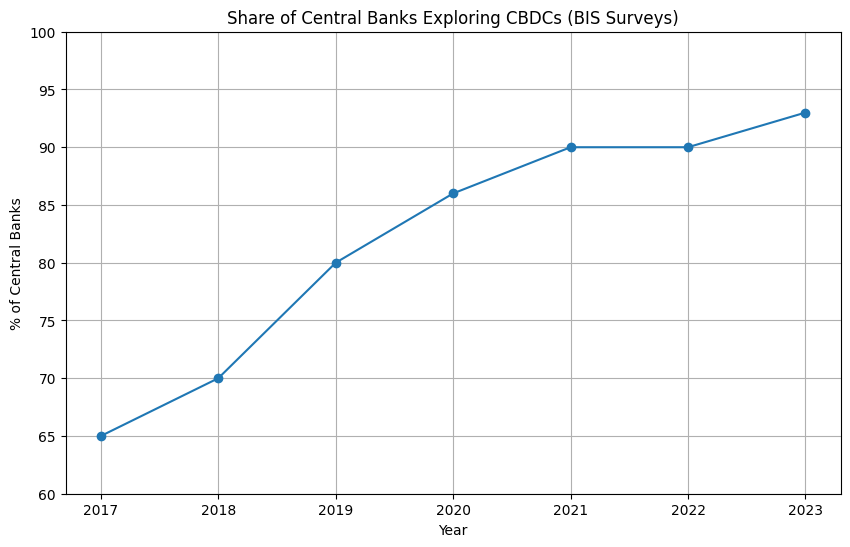

Interest in central bank digital currencies has expanded rapidly across monetary authorities worldwide over the past decade. Source: Bank for International Settlements (BIS)

Over time, that changes the role money can play in policy. Instead of broad tools that operate through incentives and expectations, governments can shape outcomes with greater precision. Stimulus can be targeted not just to households, but to behaviors. Support can be directed not only to sectors but also to specific types of activity within them. The line between fiscal policy and system design begins to blur. As the International Monetary Fund has noted, CBDCs could facilitate targeted transfers and improve the effectiveness of fiscal policy—a shift that also implies a more direct role for the state in guiding how money is used.

Researchers have suggested that this is where the digital yuan begins to absorb ideas from the world of cryptocurrencies while keeping them within a regulated framework. The appeal is clear. You get speed and flexibility without surrendering oversight. The system evolves, but it remains anchored to the state.

Adoption Driven by Design, Not Demand

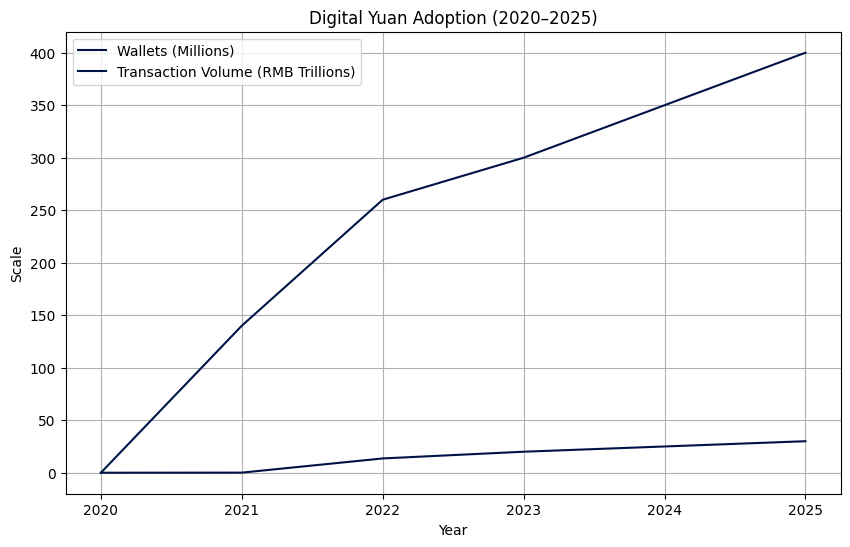

At the same time, adoption inside China has moved forward with deliberate restraint. The numbers have grown quickly, with hundreds of millions of wallets and trillions of yuan in transactions. Even so, those figures sit within a much larger landscape. The country’s population is vast, and existing payment platforms remain deeply embedded in everyday life.

For most users, there has been little urgency to switch. Alipay and WeChat Pay still dominate, handling the overwhelming majority of mobile transactions. They are familiar, reliable, and already woven into daily routines. Changing that behavior takes more than a new option. It requires a reason.

That reason, at least for now, has often come from the state itself. Local governments have distributed digital yuan directly to citizens, sometimes as part of promotional campaigns, sometimes tied to specific events. These efforts nudge people toward the system, but they also reveal something about its current stage. Demand is still being cultivated rather than pulled organically.

There is no sign that policymakers see this as a problem. Rather than forcing a rapid shift, the approach has been to expand participation while allowing habits to adjust over time.

That gap between user experience and system design is part of what makes the transition difficult to notice. From the perspective of the individual, little appears to change. The same gestures, the same interfaces, the same routines. Yet beneath that familiarity, the underlying structure becomes more integrated, more visible to policymakers, and more capable of shaping outcomes in subtle ways.

Part of that reconfiguration involves the private sector, which has been brought into the system rather than pushed aside. Major banks, both state-owned and private, have been integrated into the infrastructure. Even firms that once dominated digital payments now operate within the broader digital yuan framework.

Adoption of China’s digital yuan has moved quickly from pilot programs into broader usage, with wallet growth and transaction volume rising in parallel. What began as a controlled experiment is increasingly taking on the characteristics of embedded financial infrastructure. Source: People’s Bank of China

This avoids the disruption that might come from replacing existing platforms outright, but it also changes their role. Instead of sitting at the center of the payment ecosystem, they now operate within a structure defined elsewhere. The balance of power shifts, even if the user experience does not. Analysts have also pointed out that this creates parallel rails within the system. Traditional apps continue to function, but alongside them runs a state-backed alternative that gathers data, enforces rules, and gradually expands its reach.

Building Parallel Financial Rails Beyond the Dollar System

That design extends beyond domestic borders. Cross-border initiatives have become a central part of the digital yuan’s development, with pilot programs linking multiple countries through shared platforms. These efforts are still in their early stages, but they hint at a broader ambition.

International payments have long been shaped by constraints that are as much political as they are technical. Transactions move through established channels, often slowly and with limited transparency. For a country seeking to expand its financial influence, those constraints can feel restrictive. The digital yuan offers a potential way around them. By building new infrastructure for cross-border transactions, China can reduce reliance on existing systems while offering partners an alternative. The appeal isn’t just speed or cost, but the possibility of operating within a different system.

If those pathways deepen over time, they may begin to create forms of alignment that extend beyond payments themselves. Systems that share infrastructure tend to adopt common standards, and those standards tend to shape behavior. Once embedded, those connections can be difficult to unwind. The result may not be the replacement of existing systems, but the gradual emergence of parallel ones, each with its own rules, incentives, and points of influence.

Policy discussions within China have touched on this more openly in recent years. There is a recurring theme of creating a more balanced monetary environment, one not dominated by a single currency. The language is measured, but the direction is clear. The digital yuan is part of that vision.

Outside observers tend to read these moves through a geopolitical lens. Some see the system as a tool for expanding influence, particularly in regions where China already plays a significant economic role. Others focus on its potential to reshape how trade is settled. But regardless of which interpretation proves more accurate, the broader point is harder to dismiss. Money is not only an economic tool. It’s also a form of architecture. The systems through which payments move can influence who has visibility, who has leverage, and who sets the terms when pressure rises. And that leads into a quieter set of questions, ones that are less visible than geopolitics but no less consequential over time.

Privacy, Surveillance, and Behavioral Shifts

There are also tensions within those choices. Privacy is one of them, often discussed but not easily resolved. The idea of “controllable anonymity” suggests a balance between user privacy and regulatory oversight, but defining the line between the two can be difficult in practice. Critics have raised concerns about the potential for surveillance, particularly in a system where transactions are more visible than with cash. Officials counter that traceability is necessary for preventing illicit activity. Both arguments carry weight, and neither fully settles the question.

Less discussed, but equally important, is how visibility can influence behavior over time. When transactions become more traceable, even within defined limits, users may begin to adjust how they spend, save, or transfer funds. The shift does not require explicit enforcement. It can emerge gradually, shaped by awareness of the system itself. In that environment, the distinction between assets fully embedded in financial infrastructure and those outside it may carry more weight.

Interest-bearing balances, reserve requirements, and the interaction with monetary policy all add complexity. Some warn that smaller banks could face new pressures, particularly if deposit flows become more sensitive to system design. As the Federal Reserve has cautioned, a “widely available CBDC could serve as a close substitute for commercial bank money and could therefore affect bank deposits.” Others see opportunities to more efficiently transmit policy, with fewer frictions between intent and outcome.

Those questions are not unique to China. In the United States and other advanced economies, debates around central bank digital currencies have often centered on similar concerns: how to preserve the role of commercial banks, balance privacy with compliance, and introduce new capabilities without destabilizing existing systems.

What makes China’s approach distinct is not just its pace, but its willingness to resolve those tensions through integration rather than avoidance. Instead of keeping digital currency separate from the banking system, it has been folded into it. Instead of limiting functionality to reduce risk, capabilities have been expanded within a controlled framework.

That does not mean other countries will follow the same path. But it does raise the possibility that elements of the model may travel. Policy ideas have a way of crossing borders, especially when they prove effective in practice. Features such as targeted stimulus, conditional transfers, or more direct forms of policy transmission may begin to appear in different forms elsewhere.

Redefining the Boundaries of Public Money

What stands out is the willingness to experiment within a structured environment. The digital yuan isn’t being introduced as a finished product. It’s evolving, shaped by feedback, adjusted through policy, and tested in different contexts. That direction becomes clearer when viewed against the broader arc of China’s financial development. Over the past two decades, the country has built a sophisticated digital payment ecosystem. The digital yuan doesn’t replace that system. It builds on it while shifting its center of gravity.

In that sense, the project reflects both continuity and change. Continuity in extending existing capabilities through familiar interfaces. Change in redefining who ultimately controls the underlying infrastructure. Some analysts have suggested that this dual approach is what gives the digital yuan its resilience. It integrates with what users already know, gradually altering the landscape from within.

That raises questions about how other countries will respond. Central banks around the world have been exploring their own digital currencies, but progress has been uneven. Some have moved cautiously, concerned about unintended consequences. Others have focused on narrower use cases. China’s approach stands out for its scope. It aims to reshape multiple layers of the system at once, from retail payments to cross-border settlement. That breadth makes it harder to replicate, but it also sets a reference point.

International institutions have taken note, often framing the digital yuan as an example of how public infrastructure can coexist with private innovation. They highlight its role as a backup to existing systems, ensuring continuity in the event of disruption. That perspective emphasizes stability, though it doesn’t fully capture the strategic dimension.

The strategic dimension becomes more apparent when you consider how the system might evolve. If cross-border usage expands and more countries participate in shared platforms, its influence could grow in ways that aren’t immediately visible. That growth would not necessarily come at the expense of other currencies. But it could create a more fragmented landscape, where multiple systems operate in parallel.

There’s also an internal logic to the project that goes beyond external ambitions. As cash usage declines and digital payments become the norm, the question of what constitutes public money becomes more pressing. If private platforms dominate transactions, the role of the central bank begins to shift. The digital yuan addresses that shift directly, providing a state-backed alternative that operates within the digital environment while preserving a form of public money.

For now, the digital yuan exists alongside the systems it may one day reshape. People continue to pay as they always have, often without thinking about the infrastructure that supports those payments. But that infrastructure is changing. And as it does, the question becomes less whether the digital yuan will replace existing methods and more how it will redefine the space in which those methods operate. In that kind of environment, where the boundaries of money are increasingly shaped by policy and design, the appeal of holding at least some value in assets that sit outside those systems has a way of resurfacing.