By Preserve Gold Research

Confidence doesn’t usually collapse in a single clean motion. It frays. It gives way first at the gas pump, in grocery aisles, in car payments, and in the sense that each month takes more effort just to stand still. By the time that mood appears in national surveys, it’s rarely about one forecast or figure. It’s about a broader feeling that the headline data and lived experience are no longer moving together.

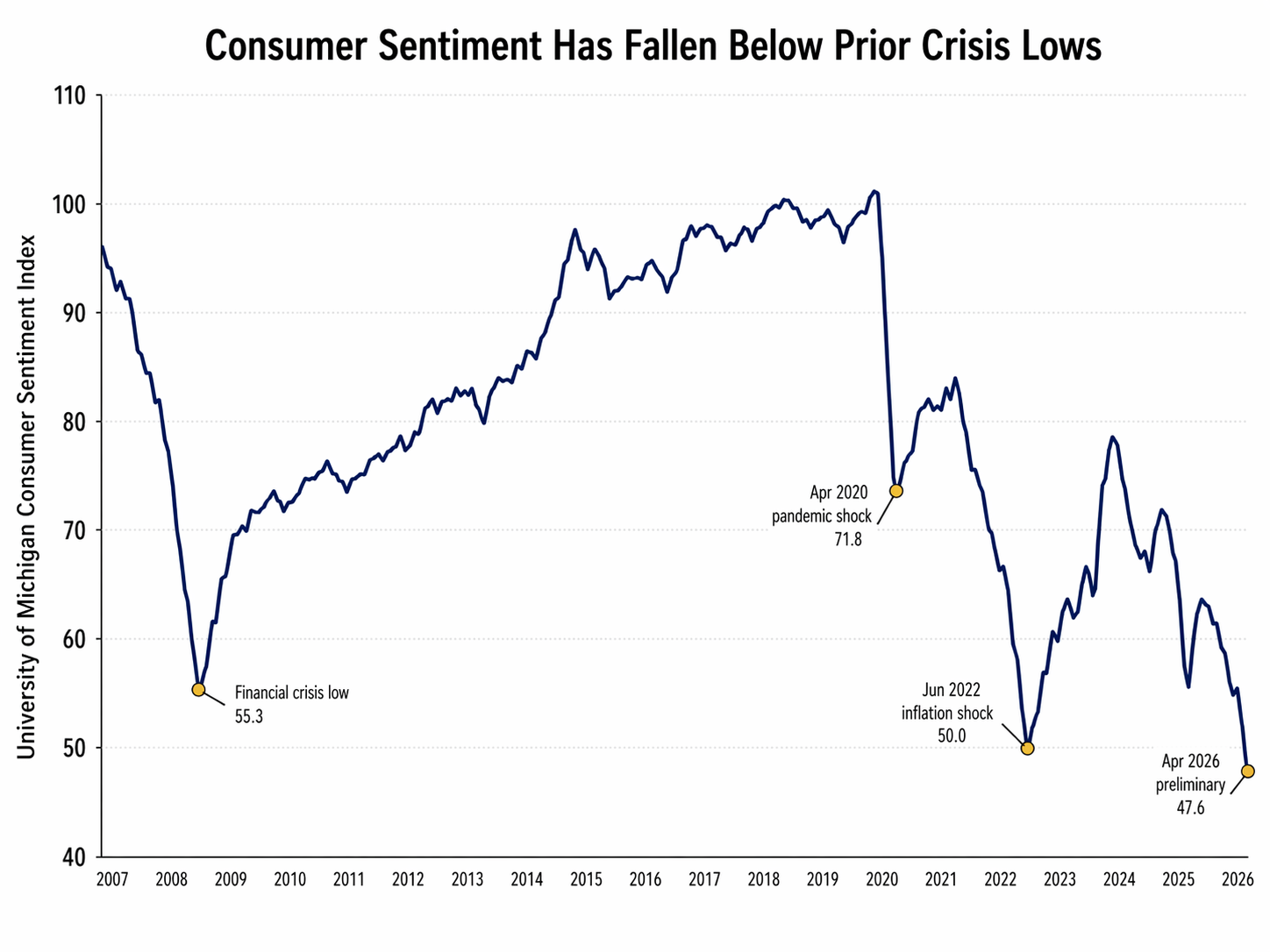

That gap is now impossible to ignore. The University of Michigan’s preliminary consumer sentiment index fell to 47.6 in April. The weakest reading in the history of the series, it was below the lows associated with the financial crisis, below the inflation panic of 2022, and far below the level seen during the first pandemic lockdowns. The headline is important, but what matters more is what the reading says about the public’s sense of control. Households are being told that unemployment is still low, that wages are still rising, that the economy has not yet cracked. Many of them clearly do not feel reassured.

When the Headline Data Stops Reassuring

What makes the April reading concerning is how broad the deterioration appears to be. The measure of current conditions fell to 50.1. Expectations dropped to 46.1. That split matters because it suggests the public is not only unhappy with present conditions but increasingly doubtful about where things are headed. Joanne Hsu, who directs the Michigan survey, said consumer sentiment “sank about 11% this month, extending a decline that began with the start of the Iran conflict.” That’s more than a passing reaction to a bad headline. It points to a chain of pressure that households understand intuitively, even when economists debate the details.

Energy prices sit at the center of that chain. Inflation had cooled from its 2022 peak, but March brought a fresh jolt. Gasoline surged more than 21% in the month, pushing the broader energy index sharply higher and lifting headline inflation back up to 3.3% year over year. Core inflation remained more contained, but consumers don’t live in the core basket. They live in the visible one. They fill their tanks, pay utility bills, buy food, and absorb insurance costs. A burst in energy prices does more than strain budgets. It revives a fear people thought they had just started to outgrow.

That shift explains the sharp rise in inflation expectations. In the Michigan survey, one-year expectations jumped to 4.8% from 3.8% in March. Such increases matter because they influence behavior before official data does: households become cautious, businesses test higher prices, and workers act defensively on wages. The mood darkens, then the economy may follow.

Oil Shock, War Risk, and Daily Prices

The shock of the war in the Middle East added force to an already unsettled backdrop. Most of the Michigan interviews were completed before the temporary cease-fire announcement in early April, meaning respondents were answering during an escalation that threatened oil flows and raised the possibility of a wider regional conflict.

Hsu noted that many consumers blamed the Iran conflict for unfavorable changes in economic conditions. Federal Reserve governor Christopher Waller put the macro risk more plainly when he warned that an extended disruption around the Strait of Hormuz could “have a lasting effect on inflation and U.S. economic growth.” Consumers may not follow the mechanics of shipping lanes or futures curves, but they understand what sustained instability in a major oil-producing region usually means. Higher fuel costs are immediate, as we’ve seen. The rest tends to arrive with a lag.

The timing could hardly be worse for policymakers. Inflation isn’t running at the extremes that forced the most aggressive tightening, but it remains high enough to keep the Fed from sounding relieved. The labor market has cooled only gradually. Unemployment was 4.3% in March, still low by historical standards, and wage growth held around 3.5% year over year. On paper, that doesn’t look like an economy in distress. It looks more like an economy losing momentum while still carrying old inflation scars. That’s a harder condition to manage because neither side of the mandate gives the Fed much room to relax.

High Rates, Low Relief

Rates remain restrictive, and households feel that in ways economic averages tend to miss. Mortgage rates near 7% have kept the housing market tight and punishing for first-time buyers. Auto financing is expensive. Credit card balances cost more to carry. Even people who are fully employed can feel poorer when so much of ordinary life has to be financed at higher rates. The result is a kind of diffuse pressure rather than a single breaking point. Nothing has to snap for confidence to weaken. It’s enough for the monthly math to keep getting worse.

That’s also why the standard “hard data versus soft data” distinction can be misleading here. Consumer sentiment is often dismissed when job growth is still positive or retail spending has not rolled over. Yet surveys capture something the monthly production figures can’t: the public’s forward-looking tolerance for continued strain. People can keep spending and still feel deeply pessimistic. And that combination may be one of the clearest signs that the expansion is becoming more brittle. Spending continues, but with less emotional cushion underneath it.

The historical comparison sharpens the point. During the financial crisis, Michigan sentiment bottomed out at 55.3. During the 2022 inflation spike, it fell to near 50. In April 2020, amid lockdowns and a deliberately frozen economy, the index held far above the latest reading.

Consumer sentiment has fallen below levels reached during the financial crisis, the pandemic lockdown shock, and the 2022 inflation surge, underscoring how deeply affordability pressure has damaged household confidence. Source: University of Michigan Surveys of Consumers / FRED, Consumer Sentiment Index.

That doesn’t mean conditions today are worse than during the Pandemic across every category. But it does suggest that today’s pessimism is reaching into places that standard macro figures don’t fully capture. There is a growing sense among many Americans that daily life has become less affordable while the official economy keeps insisting it’s still performing reasonably well.

The Soft Data Problem Gets Harder to Ignore

The disconnect has shown up elsewhere, too. The Conference Board’s confidence index has been weak, though not nearly as catastrophic, and its latest data still showed households growing more anxious about inflation and employment. A record share reported that finding jobs was becoming harder.

Job openings have come down. Payroll growth continues, but at a more modest pace. That combination can weigh on households even before layoffs arrive. The economy doesn’t need to be shedding jobs rapidly for workers to become cautious. It only needs to stop feeling generous.

There’s also a psychological residue from the last few years that many macro models underweight. Real wages have improved, and output held up better than many expected. Markets remained strong until recently. Yet much of the public still feels poorer, or at least more exposed. That sounds contradictory only if you assume sentiment should mechanically track income. But it rarely does. Households remember what costs used to be. They remember when borrowing was cheaper, when housing looked more attainable, when a jump in food or energy prices did not feel like a threat to the month. Recovery in aggregate income doesn’t erase that memory.

Tariffs complicate the picture further by embedding inflation risk into policy itself. Stanford researchers from the Institute for Economic Policy Research argue that the tariffs imposed by early 2026 could add roughly a percentage point to inflation through midyear. That isn’t the dominant driver of April’s mood collapse, but it matters because it reinforces the sense that some price pressure is being chosen rather than merely endured. Most consumers don’t parse the legal arguments around trade policy. They simply experience a world in which goods remain expensive, and relief keeps getting pushed further out.

Affordability Has Become a Credibility Test

In an election year, that matters. Voters rarely separate inflation expectations, borrowing costs, and job security into neat categories. They judge the economy by whether life feels more manageable. Right now, for many households, it does not.

Affordability has become a test of political trust across much of the developed world. When prices keep rising faster than many households can comfortably absorb, leaders lose authority even if the headline economy still looks intact. The issue becomes personal when people feel their well-being is at risk, and traditional metrics like GDP growth or low unemployment rates no longer reflect their reality.

April’s collapse in sentiment, therefore, carries more weight than a single month’s survey normally would. It doesn’t prove a recession is imminent. Nor does it cancel out stronger labor-market or output data. But it does suggest that the margin for error has narrowed. When consumers are already defensive, new shocks do not have to be severe to matter. A few more months of elevated gasoline prices, another rise in insurance costs, a modest increase in unemployment, or renewed market volatility could all land harder than they would in a more confident economy.

Credit-sensitive areas are where that caution is likely to show up first. Weaker confidence can quickly translate into softer demand for mortgages, auto loans, and consumer credit, especially when borrowing costs are already high. Households may still be employed, but that doesn’t mean they are eager to take on new monthly obligations.

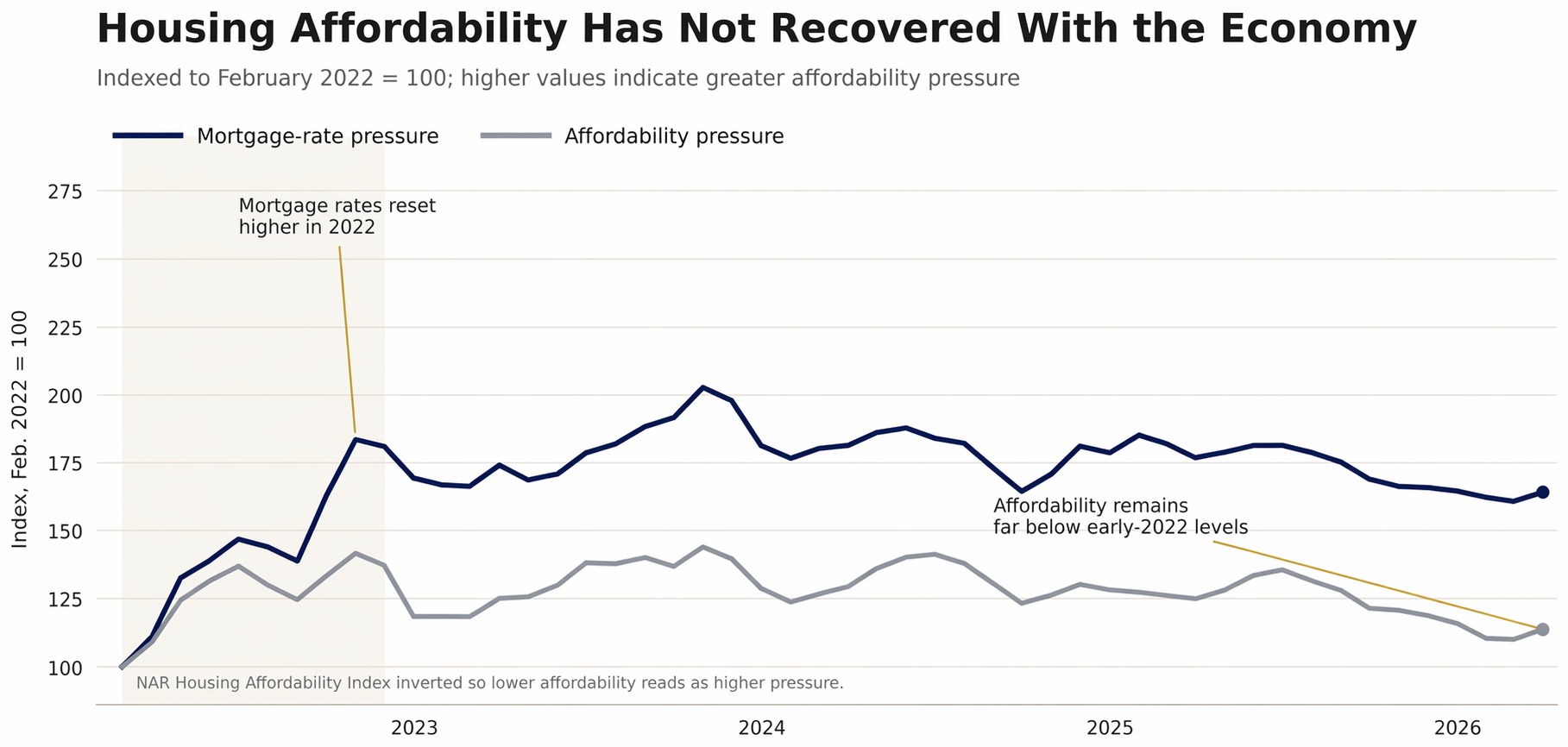

Housing is the clearest example. Prices have flattened in many markets, but mortgage rates remain high enough to discourage both buyers and sellers. Existing homeowners are reluctant to give up older fixed-rate loans. New buyers face monthly payments increasingly out of step with incomes. The result is a market caught between limited supply, poor affordability, and weak turnover. That matters because housing typically supports confidence through mobility, construction, lending activity, and the wealth effect. Right now, much of that support is missing.

Mortgage rates have stayed high enough to keep affordability under pressure, leaving many households with little sense of relief even as broader economic data remains comparatively resilient. Source: Freddie Mac Primary Mortgage Market Survey; National Association of Realtors Housing Affordability Index.

A Fading Wealth Effect

The wealth effect from financial markets has also done less to stabilize the public mood than textbook models would suggest. Major equity indices spent much of the past year near highs, yet the typical household does not experience that as a durable offset when financing costs are elevated, and essential expenses are volatile. Market gains can support confidence at the margin, but they do not erase the shock of watching fuel prices jump or realizing that the next home purchase is out of reach. Wealth that exists mainly on paper is a weak answer to recurring cash flow pressures.

That leaves the Federal Reserve in a narrow corridor. A central bank can respond cleanly when inflation is accelerating amid an overheated labor market, or when growth is collapsing, and demand clearly needs support. The present mix is messier. Inflation has cooled from its peak but remains unstable. Growth is slower but not gone. Sentiment is historically awful, but unemployment is still relatively contained. If the recent shocks prove temporary, policymakers can “look through” them, as Waller suggests. But if tariffs, energy prices, and geopolitical instability begin reinforcing one another, the Fed has less room to treat inflationary pressures as temporary.

A Slow-Growth Economy Can Still Feel Fragile

Analysts at the Peterson Institute of International Economics say the most likely path still looks like a slow-growth, no-relief environment rather than an outright collapse. That’s one reason forecasters remain divided. Some recession models show elevated but far from certain odds of a downturn. Others still lean toward a soft landing, though one with softer consumption, weaker business confidence, and continued pressure on households. In practical terms, that means growth probably slows toward something closer to 2% than the stronger pace seen last year. Unemployment may drift higher. Inflation may ease only fitfully. None of that qualifies as a disaster, but it is enough to keep most people on edge.

And that may be the more important point. Consumer sentiment doesn’t need to predict a recession with precision to matter. It can still shape one. When households become more cautious, they delay big purchases, avoid new debt, trade down, rebuild savings if they can, and react more sharply to every new price shock. Businesses then see softer demand and become less willing to hire or invest aggressively. What begins as a mood can turn into a spending pattern. What begins as a spending pattern can become a growth problem. The path from one to the other is often cumulative.

There’s a tendency among market commentators to treat confidence data as emotional excess until the numbers catch up. Sometimes that skepticism is warranted, as surveys can reflect politics as much as economics. But a record low is not just noise. A reading beneath the crisis lows of 2008 and 2022 signals that something deeper is happening in the household sector, even if it doesn’t fit neatly into a standard cyclical template. People are responding to a regime of recurring shocks in which each improvement feels conditional, and each setback arrives before the last one has been absorbed.

When Stability Stops Feeling Assumed

Policy can help at the margins, but it can’t quickly rebuild confidence once households begin to doubt the basic terms of economic stability. The Fed can avoid tightening into a softer economy unless inflation forces its hand. Lawmakers can reduce avoidable price pressure rather than add to it. Rolling back some tariff burdens would help. But what won’t work is asking Americans to trust headline figures that no longer match the pressure they feel each month.

That’s the deeper message in the sentiment collapse. A solid job market can still feel insecure. Wage growth can be positive and still fail to restore confidence. Inflation can decline from its peak and still leave households feeling that the cost of everyday life has moved permanently higher. Once that view takes hold, it changes more than spending. It changes how people think about cash, debt, homeownership, and safety itself.

That shift matters beyond the next quarter’s growth estimate. In calmer periods, investors can treat purchasing power as a background assumption. In a more unsettled period, they start asking harder questions about how much of their financial security depends on stable prices, falling rates, and the credibility of policy promises. Diversification becomes less of a slogan and more of a practical response to uncertainty.

None of this requires assuming a collapse is coming or abandoning conventional assets. It simply recognizes that prolonged affordability pressure, policy strain, and geopolitical shocks can change behavior before they change the official outlook. People become more cautious with debt, more sensitive to liquidity, and less willing to rely on a smooth disinflation story.

That may be the lasting significance of the latest sentiment reading. It is not just that consumers are unhappy. It is that many no longer feel they can assume stability will return on its own. When that assumption weakens, households and investors begin to view risk, resilience, and what it really means to feel financially secure differently.