By Preserve Gold Research

Economists say the danger, if it comes, is unlikely to arrive as a failed Treasury auction or a sudden buyers’ strike. For a large, advanced economy that borrows in its own currency, fiscal trouble more often takes a slower form. The government can still finance itself. It simply does so at higher average rates, with less room for emergency action, and with a growing share of the budget locked into past commitments. Sustainability erodes gradually until policy choices narrow in ways hard to reverse.

That’s the context for the unusually aligned signals that arrived in February. In its Article IV concluding statement, the International Monetary Fund (IMF) urged a “clear, frontloaded fiscal consolidation plan” and argued that putting debt on a decisively downward trajectory would require shifting to a general government primary surplus of around 1% of GDP, an adjustment of roughly 4% of GDP relative to its baseline. The Congressional Budget Office’s latest Budget and Economic Outlook, meanwhile, described a federal budget that remains far from balance even without a recession.

Early FY2026 budget execution already echoes previous patterns. CBO’s January 2026 Monthly Budget Review estimates a $696 billion deficit for the first four months. Receipts have risen, driven by income and payroll taxes and higher customs duties. But outlays have also increased, mainly from major mandatory programs and net interest.

Markets are not pricing an imminent U.S. fiscal accident. In late February, 10-year Treasury yields hovered around 4% and 30-year yields stayed in the high-4s. Corporate credit spreads stayed tight. However, financeable does not mean stable. Large debt and higher rates constrain fiscal choices and increase the risk that a future shock will force hurried, high-cost decisions rather than a deliberate plan.

The question is not whether the United States will suddenly be unable to borrow. Instead, it is whether the country is drifting toward a fiscal posture that depends on good luck, steady growth, contained inflation, and calm financial markets year after year. Meanwhile, mandatory spending and interest costs keep rising. The convergence between the IMF’s warning and CBO’s projections suggests near-term sovereign stress risk remains low. However, medium-term risks to economic stability and institutional durability are mounting.

The IMF warning and why it is landing differently now

While the IMF staff has stated “the risk of sovereign stress in the U.S. is low,” their concern is about cumulative pressure. The Fund expects a high-deficit environment to persist, with the general government deficit running in the 7% to 8% of GDP range and general government debt reaching roughly 140% of GDP by 2031. Officials also point to the rising public debt trajectory and “increasing levels of short-term debt-GDP” as growing stability risks for both the U.S. economy and the global financial system.

The warning gains weight from its specificity. IMF staff contend that a “decisively downward” debt path requires front-loaded fiscal consolidation, raising the general government primary surplus to about 1% of GDP—an adjustment of roughly 4% of GDP relative to the current baseline. The IMF notes that discretionary non-defense spending accounts for a small share of the federal budget. Thus, significant stabilization must rely mainly on higher revenues and reforms to large entitlement programs.

The Fund also offers a near-term interpretation of recent U.S. policy choices that have implications for markets. It estimates that tax and spending measures legislated in 2025 provide a short-term boost to economic activity in 2026 and 2027. Those same measures, however, also increase the deficit. The IMF further notes that higher tariffs can raise government revenue in the near term. At the same time, it characterizes tariffs as a negative supply shock that raises prices and reduces overall economic output.

Distribution is another IMF concern. Staff assesses recent changes as having “important distributional effects.” Some tax changes should raise household incomes, but reductions in Medicaid and food assistance, combined with higher tariffs, would, in staff models, lower real disposable income for the bottom third and raise the poverty rate. The Fund also projects that, after 2029, when more progressive income tax provisions expire, the combined policy effects could reduce real disposable income for the bottom half of the income distribution.

Fiscal reforms that impose losses on vulnerable households are harder to enact and easier to reverse. Durability is crucial when debt dynamics demand policy commitments lasting years, not months.

The CBO baseline and the early FY2026 signal

If the IMF provides an external warning, the Congressional Budget Office provides the internal benchmark against which U.S. fiscal policy can be judged. CBO’s Budget and Economic Outlook is deliberately non-normative. It projects what happens under the current law, given demographic trends, macroeconomic assumptions, and existing program rules. Its central message is that the federal budget remains structurally imbalanced. CBO projects a deficit of roughly $1.9 trillion in FY2026, rising toward about $3.1 trillion by FY2036, with deficits remaining well above historical norms for a period without a major war or recession.

Debt follows that imbalance almost mechanically. CBO projects debt held by the public will rise from about 101% of GDP in 2026 to roughly 120% in 2036, exceeding the post-World War II record. In a longer-term extension, the agency projects debt will climb to about 175% of GDP by 2056. CBO warns that, to avoid the economic consequences of large and rising debt, lawmakers must make substantial changes in tax and spending policy. The required adjustment grows larger as lawmakers delay action.

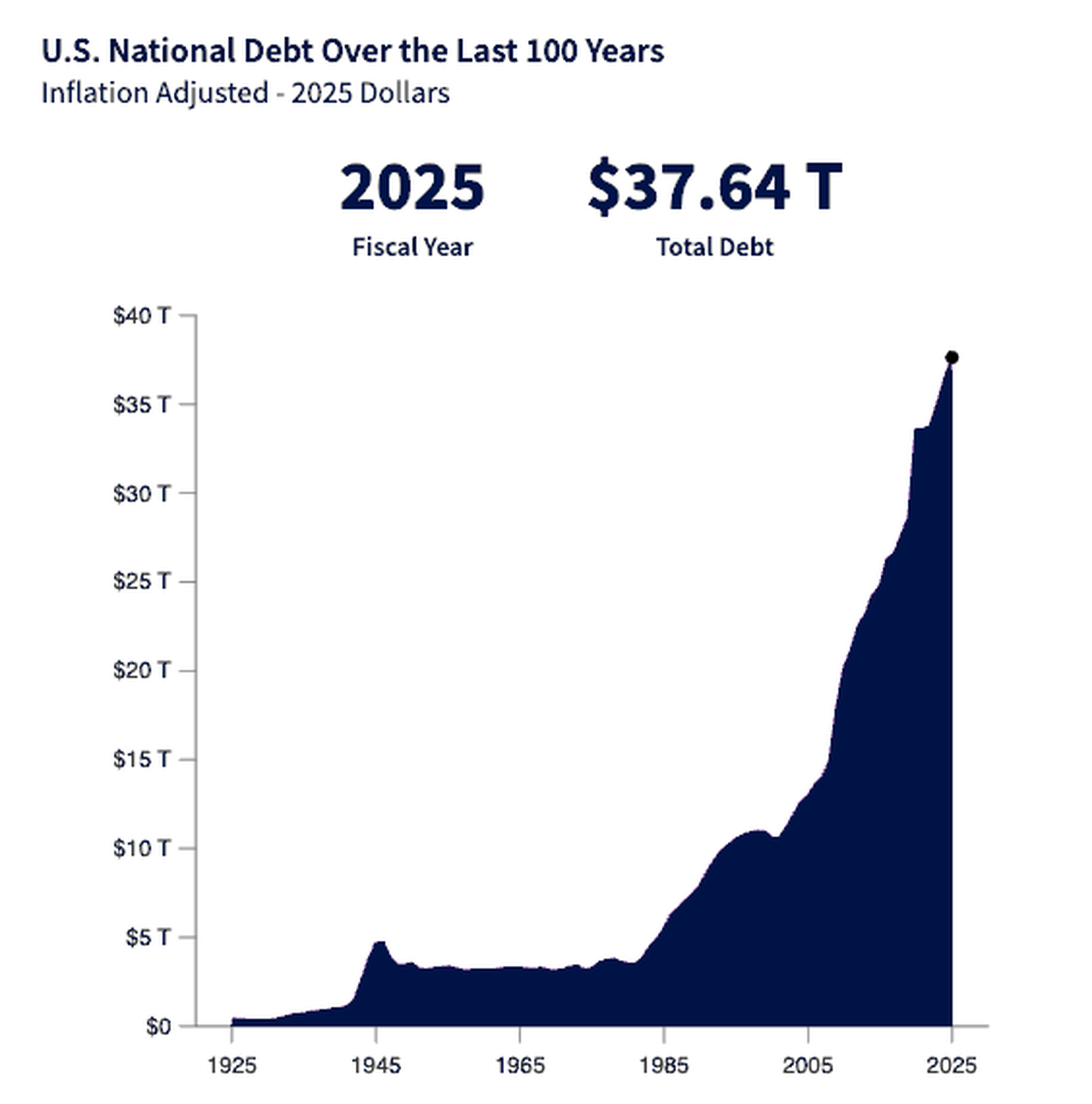

U.S. federal debt has grown dramatically over the past century, accelerating after the 2008 financial crisis and again following pandemic-era spending. By fiscal year 2025, total debt reached roughly $37.6 trillion. Source: U.S. Treasury; Federal Reserve Economic Data (FRED)

In CBO’s baseline, revenues rise modestly but stay below 18% of GDP. Outlays remain above 23% and continue to climb. The gap reflects a familiar structural pattern. Mandatory programs expand as the population ages and health care costs rise. Net interest rises as well, due to the growing debt and current interest rates. In CBO’s “By the Numbers” summary, net interest is about 3.3% of GDP in 2026 and rises to roughly 4.6% by 2036. Nominal interest payments more than double in that period.

CBO’s Monthly Budget Review for January 2026 offers a near-term snapshot of the same forces. The report estimates a $696 billion deficit from October through January. Receipts are up 12% year over year while outlays are up 2%. Much of the recent revenue strength has been tied to tariffs imposed by the Trump administration.

However, that source of revenue has become less certain recently. In February 2026, the U.S. Supreme Court ruled that the International Emergency Economic Powers Act does not authorize the president to impose tariffs. This invalidates several of the administration’s sweeping trade duties. The decision creates uncertainty around how long those revenues can persist. It also raises the possibility of large refund claims from companies that paid the duties. On the spending side, the underlying trend is unchanged. Outlays for Social Security, Medicare, and Medicaid continue rising. Net interest again accounts for much of the year-over-year spending growth.

These figures help interpret the narrative of “early FY2026 deficit widening” without over-reading short-term fluctuations. Through January, the cumulative deficit is actually smaller than in the same period a year earlier. This is partly because of timing effects and stronger revenue collections. Yet the overall level of borrowing remains extraordinarily large. CBO still projects that the full-year FY2026 deficit will exceed the FY2025 deficit.

The tightening arithmetic of debt, growth, and interest costs

A fiscal path is unsustainable when stabilizing debt needs changes that are too large, politically unworkable, or too abrupt. The accounting is straightforward. Primary deficits increase debt, and government debt rises when interest rates exceed economic growth. Improving primary balances or keeping growth above interest costs stabilizes debt. As debt nears the size of the economy, the math becomes more sensitive. Even small changes in interest rates or growth can shift the trajectory.

CBO’s long-horizon extension clearly shows the compounding effect. By 2056, the agency projects net interest spending will reach 6.9% of GDP. That will exceed projected spending on Social Security (6.0% of GDP) and Medicare (5.5%). In practical terms, servicing past borrowing will become one of the federal government’s largest expenditures. Yet it produces no direct public service.

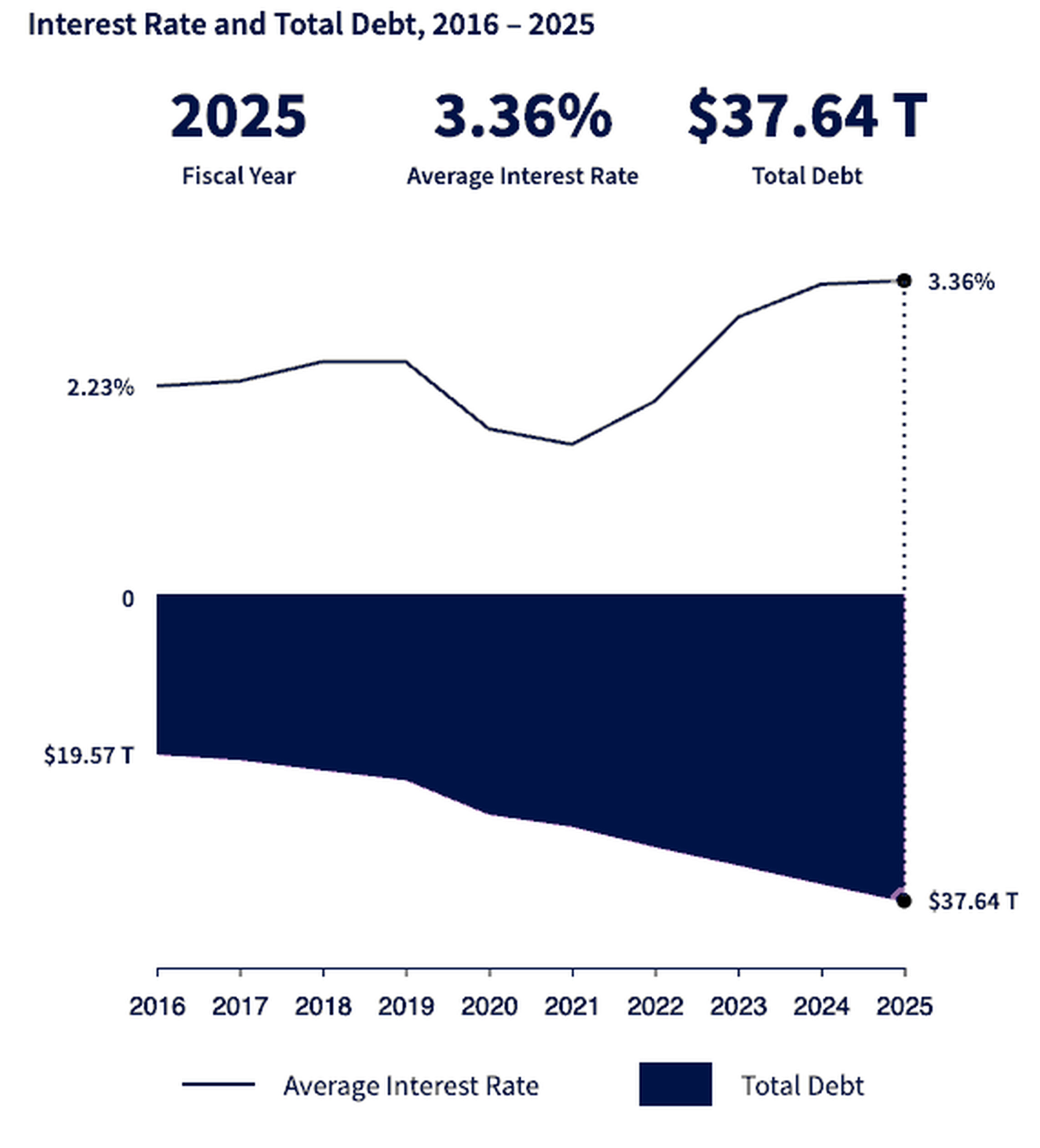

Federal debt has continued to rise while borrowing costs have moved higher. By the end of 2025, the U.S. was carrying about $37.6 trillion in debt with an average interest rate near 3.36%. Source: U.S. Treasury; Congressional Budget Office (CBO)

The distinction between the primary balance and the total deficit is central to this dynamic. The primary balance reflects the part of the budget policymakers can influence most directly through taxes and program rules. Net interest reflects the interaction between yesterday’s borrowing and today’s interest rates. In a low-rate environment, a country can run persistent primary deficits without immediate stress because interest costs remain modest. In a higher-rate environment, interest payments grow more quickly and begin to compound. Preventing debt from accelerating then requires a stronger primary balance. CBO’s baseline, which combines large deficits with rising interest costs, reflects that higher-rate logic.

Over time, the consequences appear through the channel economists describe as crowding out. CBO notes that higher federal borrowing increases competition for available savings and can place upward pressure on interest rates. That dynamic can discourage private investment, which eventually feeds through to slower productivity growth and weaker wage gains. Because the United States borrows in deep global capital markets and because saving behavior can shift, the magnitude is difficult to estimate, but the direction is clear. Fiscal sustainability matters not only because of crisis risk but because persistent deficits can gradually weaken long-term growth.

Term premiums provide a link between fiscal arithmetic and financial markets. In its latest outlook, the CBO revises its estimate of the effect of rising debt on interest rates. The agency now concludes that increases in debt relative to GDP raise the term premium investors demand for holding long-dated Treasury securities. The term premium represents the portion of long-term yields that can rise even when inflation expectations and the expected path of short-term policy rates remain stable. If larger Treasury issuance increases the compensation investors require for duration risk, the federal budget absorbs the effect through higher borrowing costs even in a relatively stable macroeconomic environment.

This dynamic explains why the IMF’s proposed adjustment of roughly 4% of GDP carries weight. Once net interest grows large, marginal savings in smaller parts of the budget cannot plausibly reverse the trajectory. CBO’s projections tell a similar story. Federal outlays remain well above revenues, and the gap reflects durable political support for programs combined with an interest bill that compounds automatically.

Politics, distribution, and what credible consolidation could look like

U.S. policymakers have long understood the arithmetic behind the growing fiscal imbalance. The challenge lies in politics. Fiscal consolidation requires decisions about burden sharing, and political systems often struggle to reach an agreement on how the adjustment should be distributed.

IMF staff emphasize that recent policy changes have meaningful distributional consequences. In their analysis, some policy combinations could raise poverty and reduce real disposable income for lower-income households. Even readers who view the IMF skeptically should recognize its political economy implications. Reforms perceived as unfair are harder to pass and easier to reverse. When debt stabilization requires policy commitments lasting many years, that fragility becomes a market-relevant risk.

Sustainability also has an institutional dimension that receives less public attention. IMF staff stress the importance of preserving the U.S. institutional framework for economic and regulatory policymaking and of fully resourcing agencies responsible for revenue administration, financial oversight, and economic statistics.

The reasoning is practical. Weak tax administration reduces revenue collection. Weak financial oversight increases the risk of crises. Weak statistical systems undermine the quality of policy decisions. Fiscal strain can gradually erode this state capacity long before financial markets show obvious signs of stress.

Any credible consolidation plan must address the drivers of long-run spending growth. IMF staff argue that stabilization can’t be achieved primarily through cuts to non-defense discretionary spending. Most of the adjustment must come from higher revenues and changes to entitlement programs. CBO’s baseline supports the same conclusion. Discretionary spending declines as a share of GDP while mandatory programs and net interest continue to expand. Regardless of political ideology, the arithmetic implies that freezing discretionary spending alone will not stabilize the debt trajectory.

That doesn’t mean consolidation must take the form of blunt austerity. The IMF outlines an illustrative alternative policy mix designed to improve distributional outcomes while supporting growth. Its proposal includes measures to reduce imbalances in Medicare and Social Security, close avenues for tax avoidance, strengthen work-support programs such as the earned income tax credit, and replace tariffs with a destination-based consumption tax. The precise details remain open to debate. The broader point is that fiscal consolidation is not simply a choice between higher taxes and lower spending. It is also about incentives, compliance, and the structure of social protection.

Policy design matters for growth. Fiscal multipliers, the effect of spending cuts or tax increases on economic activity, vary with the business cycle and with the composition of policy changes. IMF research finds that multipliers tend to be larger during economic downturns than during expansions. Abrupt fiscal tightening in weak conditions can therefore impose larger output losses than policymakers expect.

Research following the global financial crisis also found that growth forecasts were often overly optimistic when consolidation programs proved stronger than anticipated, suggesting that multipliers had been underestimated. The implication for U.S. policy is that consolidation should be designed and timed carefully so that near-term economic drag is limited while long-term fiscal credibility is strengthened.

Delay carries its own costs. CBO has analyzed the economic effects of postponing debt stabilization and concludes that the longer policymakers wait, the larger future policy changes must be to stabilize debt relative to GDP. The adjustment will ultimately occur through higher taxes, lower benefits, or some combination of both. The intergenerational trade-off is clear. Avoiding political conflict today does not eliminate the adjustment. It transfers the burden to future taxpayers and beneficiaries, who may also face weaker growth if rising debt reduces investment and wages over time.

Debates about whether high debt is less dangerous when interest rates remain below the economy’s growth rate shaped policy thinking during the 2010s. Renowned Economist Olivier Blanchard has argued that persistently low interest rates could make higher debt less costly than traditional models suggested. He also emphasized that rising debt continues to increase fiscal risk and reduce policy space during future shocks. But the current environment challenges those assertions. Long-term interest rates are higher, term premiums have returned, and projections show net interest costs rising steadily.

What “unsustainable” is likely to mean in the United States

If the U.S. fiscal path becomes meaningfully unsustainable, it’s unlikely to begin with a sudden inability to sell Treasury securities. The more plausible pattern is a gradual tightening of constraints. Net interest could absorb a growing share of federal revenue, leaving less room for other priorities and steadily narrowing fiscal flexibility.

Financial markets would likely reflect the same pressure. Investors could demand greater compensation for holding long-term Treasury debt, keeping long-term interest rates elevated even if inflation remains contained. CBO now incorporates this channel directly into its modeling, concluding that higher debt levels tend to raise term premiums. While estimates remain positive in early 2026, even modest increases in the compensation investors require for duration risk would raise borrowing costs and reinforce the upward trajectory of federal debt.

Fiscal strain can also surface through political and institutional channels. Governments facing rising fiscal pressure may struggle to sustain the administrative capacity needed to manage complex fiscal adjustments. Revenue collection, financial oversight, and credible economic statistics depend on institutions that must remain adequately resourced. Distributional tensions can further complicate reform if consolidation policies increase poverty or reduce incomes for lower-income households.

Taken together, the IMF’s external warning and the CBO’s internal baseline indicate that the U.S.’s fiscal trajectory is becoming harder to describe as stable. Persistent borrowing during ordinary economic conditions, combined with a rising interest burden in a higher-rate environment, steadily narrows policy flexibility.

For policymakers, the implication is clear. Credible fiscal consolidation that stabilizes debt while protecting vulnerable households would strengthen long-term stability. For investors and households, the lesson is related but different. Fiscal systems tend to adjust slowly, often over years marked by higher borrowing costs, inflation risk, or financial repression. Periods like these have historically encouraged diversification beyond purely financial claims on government balance sheets. Hard assets such as gold have often played a role in that process, serving as a store of value when fiscal trajectories become more uncertain, and policy space narrows.