By Preserve Gold Research

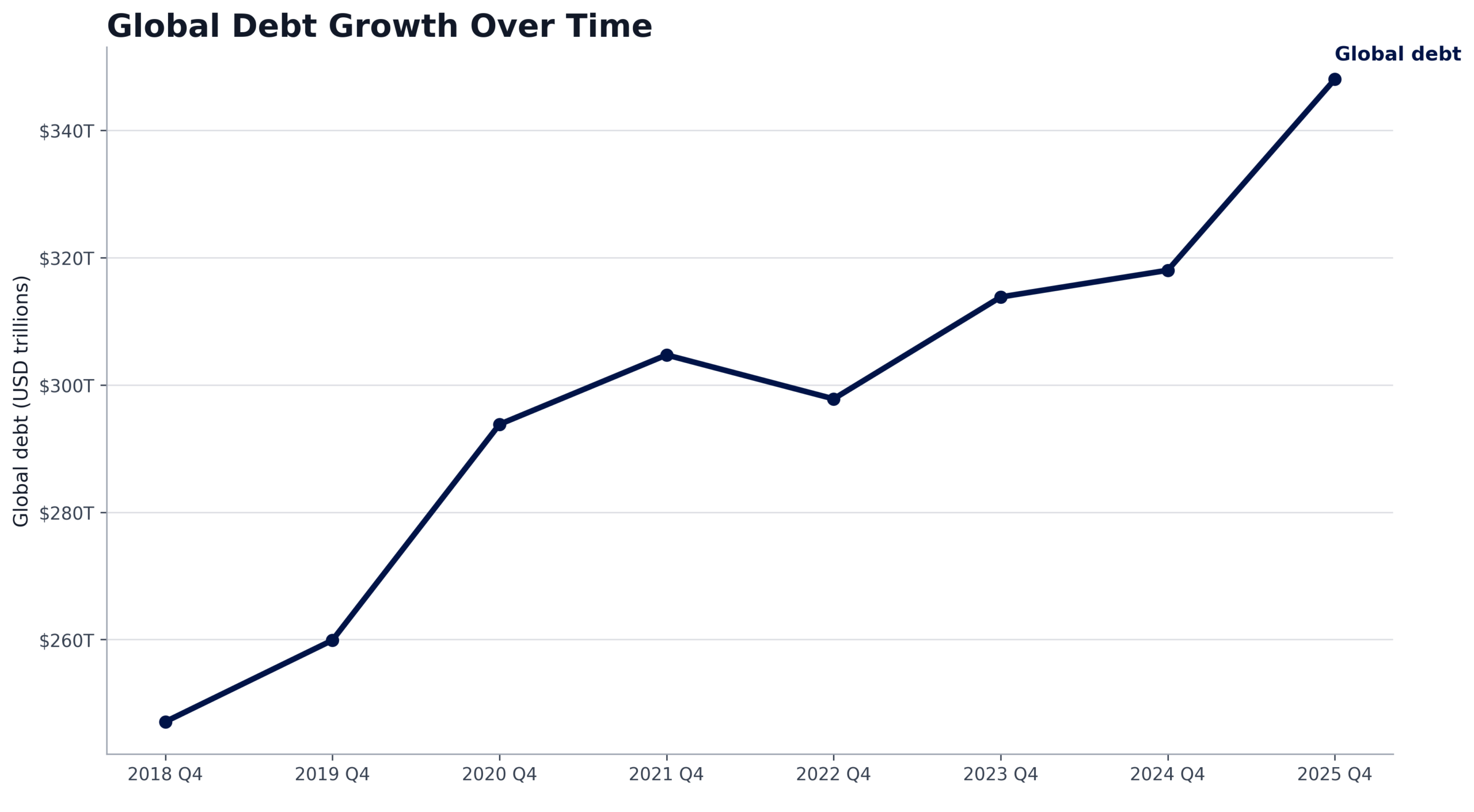

Debt used to sit quietly in the background of the global economy. Today, it plays a far more active role, influencing what governments can spend, how central banks respond to inflation, and how financial markets react when confidence begins to wobble. By the end of 2025, global debt reached about $348 trillion, according to figures compiled by the Institute of International Finance. The group said the roughly $29 trillion increase during the year marked the fastest annual rise since the pandemic era. Governments accounted for more than $10 trillion of that expansion.

While the headline figure is striking, it’s often misunderstood. Global debt extends far beyond sovereign bonds, encompassing borrowing by households, corporations, financial institutions, and governments. On its own, the number doesn’t signal an immediate crisis. The more consequential questions involve how the debt is financed, how costly it is to carry, who ultimately holds it, and how easily existing obligations can be refinanced as interest rates change.

International institutions have begun issuing more direct warnings about the long-term trajectory. The International Monetary Fund projects global public debt could exceed 100% of world GDP by 2029. That would represent the highest level since 1948, with risks that the ratio could climb further if fiscal pressures intensify.

Attention is also turning to the mechanics of government borrowing. In its 2026 Global Debt Report, the Organisation for Economic Co‑operation and Development (OECD) warns that sovereign financing needs are reaching record levels as the investor base shifts. Central banks that once absorbed large volumes of government debt are stepping back, leaving private investors to play a larger role.

For developing economies, the pressure has taken a different form. The World Bank reports that external debt among low- and middle-income countries reached record levels in 2024. At the same time, interest rates on newly issued public debt climbed to multi-decade highs, while net financial flows to creditors have remained unusually large.

As global borrowing continues to expand, the central question is less the size of the debt stock than the conditions under which it must be sustained. In a world of higher interest rates and shifting capital flows, the cost of carrying that burden is becoming an increasingly important variable in the global economic outlook.

Breaking Down the $348 Trillion Global Debt Total

The phrase “global debt” can hide more than it reveals. In the IIF framing that underlies the $348 trillion figure, the total is an economy-wide stock that aggregates what governments, households, non-financial businesses, and the financial sector owe. In the 2025 estimates cited in public reporting, government debt was about $106.7 trillion, non-financial corporate debt about $100.6 trillion, household debt about $64.6 trillion, and financial-sector debt about $76.4 trillion.

Global debt has climbed steadily over the past decade, reaching roughly $348 trillion by the end of 2025, with government borrowing driving much of the increase. Source: Institute of International Finance (Global Debt Monitor)

That breakdown matters because these categories behave differently in downturns. Household debt stress shows up in consumption and housing. Corporate debt stress shows up in investment and layoffs. Public debt stress shows up in budgets and bond auctions. Financial-sector debt stress can show up as a funding squeeze that amplifies everything else.

It also matters that debt is a stock, while the political debate often focuses on the flow. A country can have a large debt stock and still be stable if it can roll that debt reliably at reasonable rates. But the risk rises when refinancing becomes harder, or when debt service rises faster than the economy’s capacity to pay. This is why institutional reports keep returning to refinancing calendars, investor base shifts, and debt-service metrics.

Different institutions also use different “global debt” lenses. The IMF’s Global Debt Database work, for example, emphasizes comparable public debt definitions and flags how public and private debt ratios evolved after the pandemic. In its 2025 Global Debt Monitor note, the IMF describes a post‑COVID picture in which global public liabilities fell from about 100% of GDP to below 93% of GDP, while private debt fell more sharply, from about 159% to under 143% of GDP.

Taken together, these perspectives suggest a two-layered story. The first layer is the level. Debt remains historically high and, in dollar terms, continues to set records. The second layer is the structure. The burden is shifting back to public balance sheets, while ultra‑low rates no longer cushion the cost of carrying debt.

Government Spending, Interest Rates, and the New Debt Reality

The IIF’s 2025 framing points squarely to fiscal choices. The reported global increase was “mainly” driven by government spending, and public borrowing contributed more than $10 trillion of the annual gain, with large contributors including the US, China, and the euro area.

This is the part of the story many already recognize. Governments ran large deficits during the pandemic and then faced new pressures. Defense spending rose, energy transitions grew more expensive, industrial policy competition intensified, and aging-related programs proved politically difficult to scale back. The International Monetary Fund noted that the expected medium-term path for global public debt is now higher and steeper than it appeared before the pandemic. The institution also warned that risks remain tilted toward debt accumulating even faster.

The change that has quietly reshaped everything is the interest-rate regime. When rates were near zero, many governments could extend maturities and lock in low coupons, making rising debt stocks feel manageable. When rates rose sharply in 2022 and stayed elevated longer than expected, debt service stopped being a distant, technical line item and became a visible budget constraint. The BIS has warned that high public debt combined with rising interest rates and sluggish growth increases the odds of adverse scenarios, including refinancing difficulties and pressure on monetary policy frameworks.

The OECD adds a market-structure angle that is easy to miss if only deficits are tracked. In its 2026 Global Debt Report, the group estimates that governments and companies will borrow about $29 trillion from bond markets in 2026. The report also notes a shift in the investor base. Buyers today are often more sensitive to price moves and, in some cases, more leveraged, as central banks have reduced bond holdings. OECD’s report also highlights a tendency to issue shorter maturities as borrowers adapt, which can reduce immediate interest expense but increases refinancing exposure.

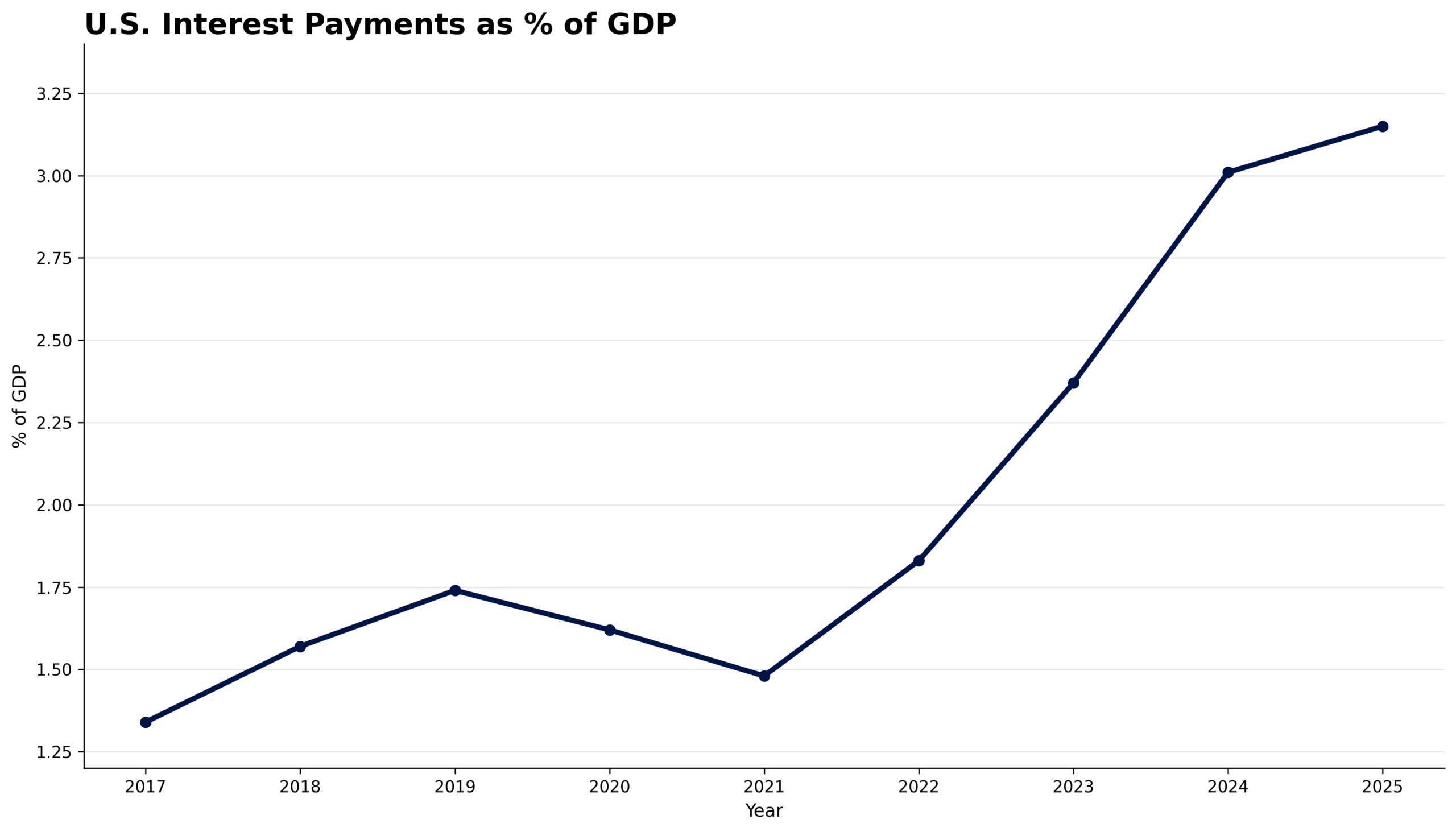

U.S. interest payments have risen sharply as higher rates reset borrowing costs, turning debt service into a growing share of the economy. Source: Federal Reserve (FRED), U.S. Bureau of Economic Analysis

This isn’t just speculation. Financial stability discussions increasingly focus on the “plumbing” around government bonds, because that plumbing is where small confidence shocks can turn into big liquidity events. Recent analyses point to vulnerabilities in the government bond-backed repo market, where leverage and dependence on short-term funding can amplify stress when conditions tighten.

Several episodes serve as reminders of how quickly market functioning can deteriorate. The sudden spike in US repo rates in 2019 and the sharp turmoil in the U.K. gilt market in 2022 both showed how strains in funding markets can spread rapidly through the financial system once confidence begins to slip.

In other words, higher debt would be less concerning if the world had a stable, cheap funding environment and a deep pool of steady buyers. But institutions are warning that debt is growing into a world with more volatile rates, less central bank absorption, and a greater role for fast-moving holders.

How Debt Risks Differ Across the United States, Europe, China, and Emerging Markets

The country story is not a single story. The most important differences are currency, investor base, maturity profile, and the link between government balance sheets and domestic financial systems.

In the United States, one stabilizing feature is that the government borrows in its own currency, and US Treasuries sit at the center of global finance. But the long-run challenge is the arithmetic of persistent deficits plus higher interest costs. The IMF has repeatedly argued for credible fiscal consolidation, and public reporting on IMF analysis has pointed to debt ratios rising through the decade even under baseline assumptions.

Japan is often described as the “high-debt country that never breaks.” That reputation rests on a large domestic savings base, a deep home bias in government bond holdings, and a central bank willing to intervene aggressively when markets become unstable. Yet the trade-off is that debt remains high even in calm times, and demographic pressures make long-term fiscal adjustment difficult. IMF and BIS both stress that high debt increases vulnerability when rates rise, and growth is weak, even if crisis timing is unpredictable.

Europe is best viewed as a set of overlapping systems. The euro area has a shared currency but national fiscal policies, and the market still prices sovereign risk country by country. Eurostat’s numbers show the euro area government debt ratio around the high‑80s percent of GDP in 2025, with both the level and composition clearly spelled out: debt is mostly securities, with a smaller share in loans and a very small share in currency and deposits.

That composition sounds technical, but it points to a practical issue. A bond-heavy debt structure means governments are constantly exposed to market repricing, especially as older low‑coupon bonds mature and must be replaced. This is one reason the OECD’s emphasis on refinancing needs resonates in Europe, where the “rollover” question can quickly become political.

China’s debt picture is difficult to capture with a single number. The lines between central government debt, local government borrowing, and state-linked entities often blur. Analysts frequently note that fiscal stimulus can move through quasi-fiscal channels rather than traditional budgets. When that happens, potential liabilities can grow outside the most visible parts of the system. China’s debt concerns are also tied to broader economic pressures, including slower growth, stress in the property sector, and the need to support local government finances, all of which add to the strain.

Major emerging markets show why currency and maturity matter as much as the debt ratio itself. Countries with a higher share of external or foreign‑currency borrowing can be forced into painful adjustment when global rates rise or when the dollar strengthens, because debt service becomes more expensive just as capital becomes harder to attract. This is why international institutions often focus on liquidity needs and near-term maturities as warning lights rather than treating every debt stock as equally dangerous.

The World Bank’s 2025 International Debt Report brings this into focus for low- and middle-income countries as a group. It reports record external debt levels in 2024 and unusually large net outflows to creditors during 2022-2024, while also noting that the interest rates paid on newly contracted public debt reached multi-decade highs. That combination can produce “squeeze” conditions even when headline debt ratios look moderate.

A practical way to hold these differences in mind is to separate “solvency” from “liquidity.” A country can be solvent (able to pay over time) and still face a liquidity crunch (unable to refinance smoothly at a given moment). Much of the recent institutional concern centers on exactly that window where refinancing calendars meet fickle markets.

Why Refinancing Pressure Is the Hidden Risk in Global Debt

The biggest near-term risk is not that the world runs out of money. It’s that refinancing becomes more fragile in pockets of the system, and fragile pockets can spread through trade links, banking exposures, and risk sentiment.

One channel runs through interest payments. As bonds reset from low coupons to higher ones, interest consumes a rising share of revenue, pushing governments toward either higher taxes, lower spending, or more borrowing. The IMF’s fiscal work emphasizes that debt dynamics can deteriorate quickly when higher rates meet weak growth, and it also stresses that risks are tilted toward worse outcomes than baseline projections.

Another channel runs through market structure. The OECD argues that central banks’ reduced bond holdings and the rise of more price-sensitive investors can make markets more vulnerable to shocks. This matters because in a stress episode, the marginal buyer determines the price, and prices determine whether refinancing remains smooth or becomes destabilizing.

A third channel runs through the financial system’s use of government debt as collateral. Government bonds are treated as safe building blocks in repo markets and derivatives margining, which is why disruptions in those markets can ripple outward. Recent regulatory and stability discussions have highlighted leverage and concentration risks in large government-backed repo markets.

For emerging markets, the first break is often external. When global risk appetite falls, capital outflows can force exchange-rate depreciation, and that can raise the local cost of servicing foreign-currency debt. Even when borrowing is mostly local currency, a sudden stop can still hit through higher domestic rates and forced fiscal tightening. The World Bank’s emphasis on net outflows and high borrowing costs is essentially a warning about this kind of external squeeze.

Over the medium term, demographics become a slow but relentless driver. Aging societies tend to spend more on health care and pensions while their workforces grow slowly. That makes it harder to “grow out” of debt without deliberate policy changes. The IMF frames this as part of a broader set of pressures (defense, disasters, and social demands) that make the public debt outlook structurally more challenging than it was a decade ago.

Geopolitics pulls in the same direction. A world with greater fragmentation and greater security competition tends to produce parallel industrial policies, supply chain redundancy, and higher defense budgets. Those choices may be rational responses to risk, but they are rarely cheap and often pile on existing obligations rather than replacing them.

At a deeper level, the danger is a feedback loop between fiscal and financial conditions. The BIS has warned that high public debt can increase the financial system’s vulnerability when interest rates rise, and asset values fall. The institution has also pointed to a broader risk. Central banks could face pressure to keep policy too loose to protect government finances. Over time, that kind of pressure can blur the line between monetary policy and fiscal needs.

Possible Paths for the Global Debt Outlook

The policy challenge is not simply to “cut debt.” The real task is to keep governments able to respond to shocks without letting borrowing costs or refinancing risks spiral out of control. That balance varies across countries, but several themes recur in major institutional reports.

One of them is credibility. Investors don’t expect perfection, but they do need a believable path that stabilizes debt in the medium term. The IMF has repeated this point often. Its guidance stresses credible fiscal consolidation where it’s needed, designed in ways that do not choke off growth.

Another theme is composition. Countries can reduce risk even when debt remains high by extending maturities when market conditions allow, limiting foreign-currency exposure, and improving transparency around contingent liabilities. Eurostat’s breakdown of euro area debt instruments illustrates how composition can be tracked systematically, and the OECD has warned that a shift toward shorter maturities can raise refinancing risk even if it eases near-term interest expense.

For developing economies, the World Bank emphasizes using any easing in financial conditions to strengthen fiscal positions rather than rushing back into external markets on expensive terms. Its data on high net outflows and elevated interest rates on new public borrowing make the practical case: when liquidity is tight, waiting for better terms and strengthening domestic revenue can be the difference between stability and repeated crisis management.

If you translate the policy debate into scenarios, three broad paths stand out.

In a managed-adjustment scenario, growth remains steady, inflation continues to cool, and governments gradually shift from broad support programs toward more targeted spending and revenue measures. Debt doesn’t fall fast, but it stabilizes because nominal growth and primary balances stop deteriorating. This is the outcome the IMF is trying to make more likely when it describes the need to rebuild buffers and prevent debt from compounding.

In a higher‑for‑longer scenario, rates remain elevated, and term premia rise as investors demand greater compensation for holding long-run fiscal risk. The OECD’s warning about a more price-sensitive investor base and borrowing tilting to shorter maturities fits naturally here, because shorter maturities can make the debt stock reset faster into higher coupons. Under this scenario, even countries that avoid outright crisis face a slow grind as interest costs crowd out other priorities.

In a shock scenario, the trigger could be geopolitical escalation, an energy shock, a sharp repricing of risk assets, or a liquidity event in core bond markets. The BIS’s concerns about adverse scenarios under high debt and higher rates, and its discussions on stability around leveraged government-bond financing channels, both point to this possibility. The likely pattern is not a synchronized global default but a sequence of stress episodes among the most exposed borrowers, with spillovers through banks, funds, and exchange rates.

Where does that leave the $348 trillion headline? It’s best read as a sign of political and economic reality. Governments have taken on a larger share of the world’s balance-sheet risk, and they are doing so in a world where markets are less forgiving than they were in the 2010s.

That doesn’t guarantee a crisis. It does, however, make ordinary fiscal discipline more important. Transparent budgets, stable borrowing structures, and credible institutions serve as safeguards that prevent rising debt from turning into instability. When those disciplines weaken, markets tend to impose their own version of discipline, often far more abruptly.