By Preserve Gold Research

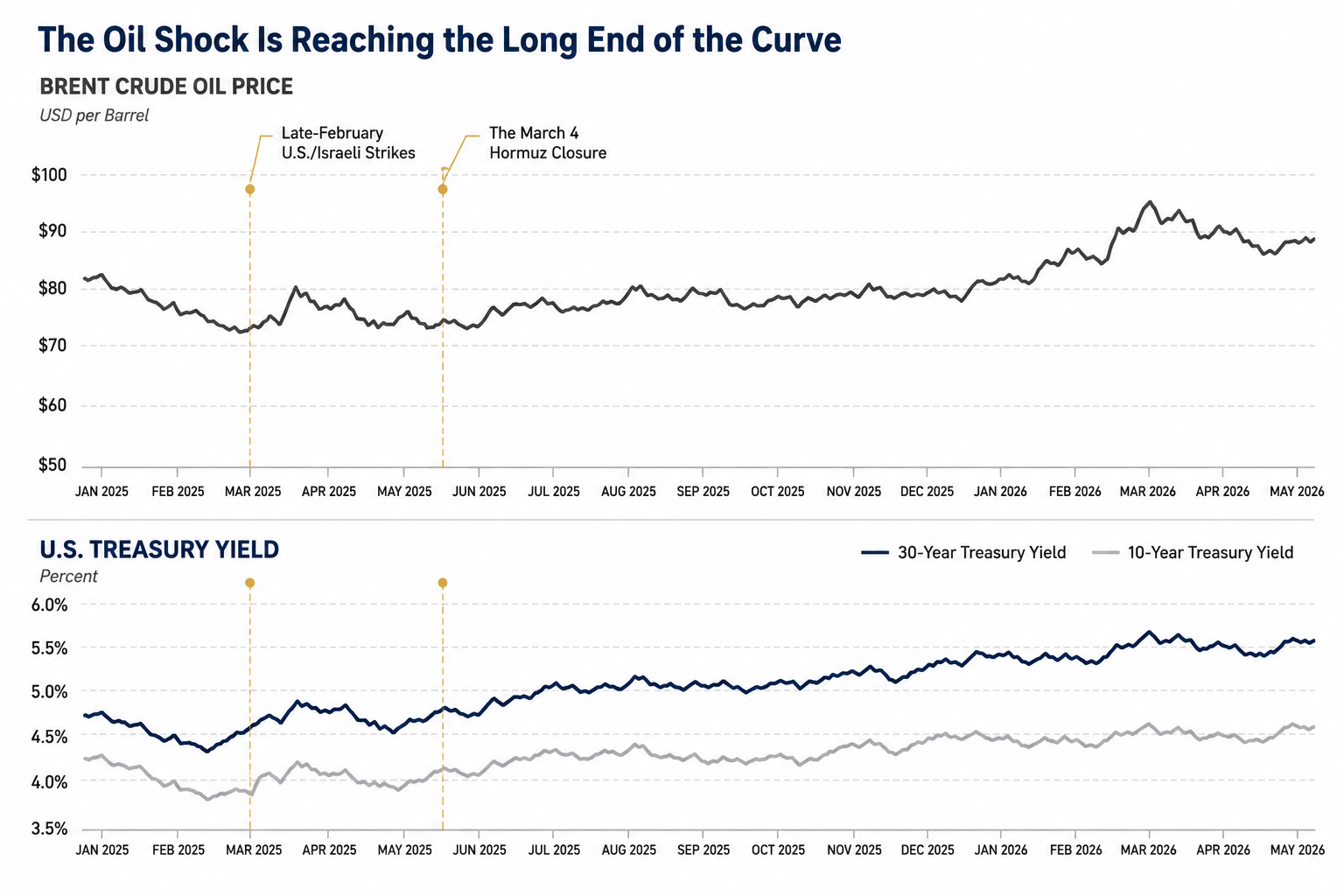

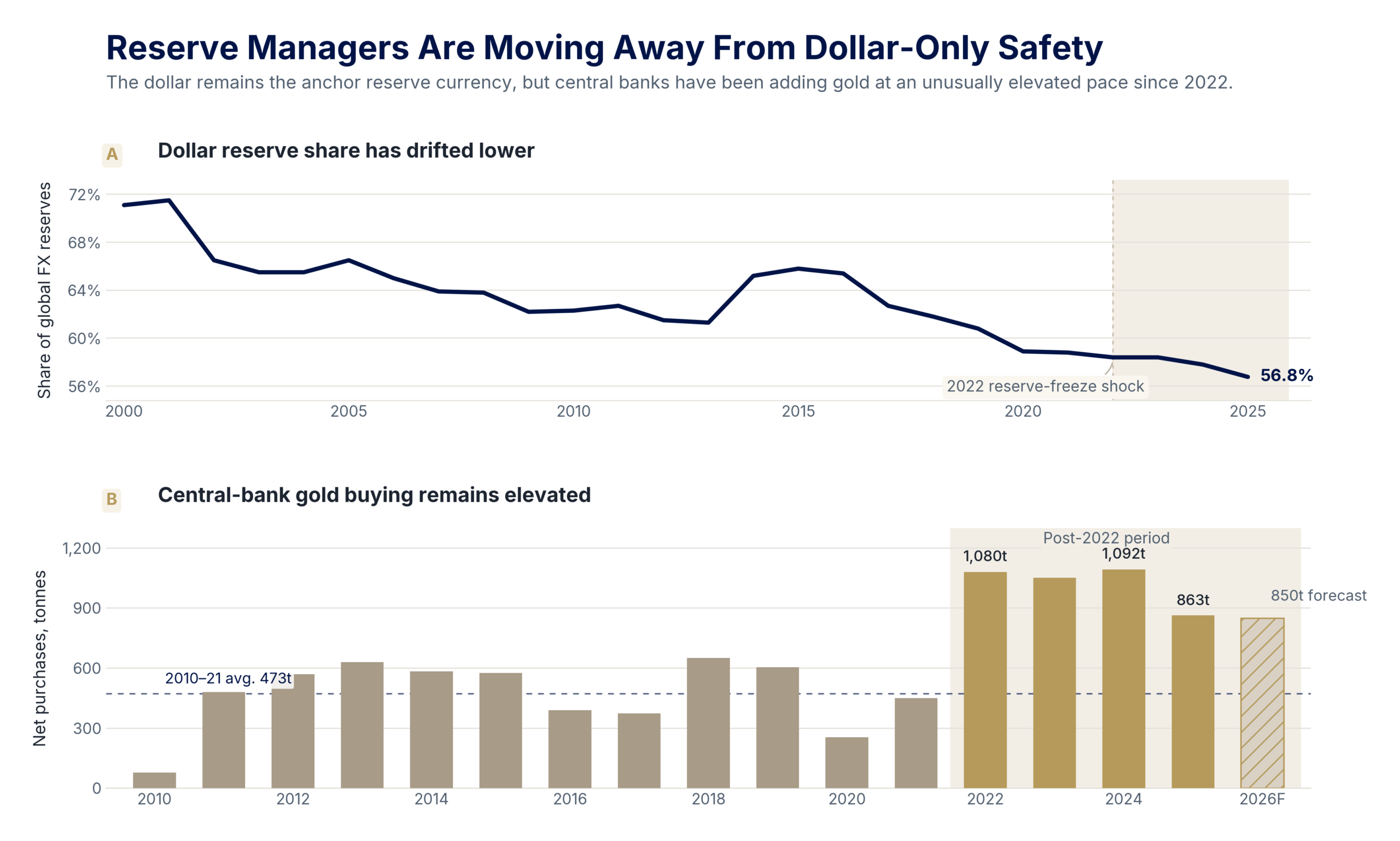

The Strait of Hormuz has been formally closed since March 4. Brent crude briefly climbed above $114 a barrel in early May before easing back toward one hundred one. The thirty-year Treasury yield crossed 5% in early May. The IMF’s most recent reserve survey, released on March 27, showed the dollar share of allocated foreign-exchange reserves drifting toward 56.8% at the end of 2025.

None of those numbers, taken alone, marks a regime change. Read together, against the backdrop of the war that began with coordinated American and Israeli airstrikes on Iran in late February, they describe a global financial system that’s being repriced in slow motion.

The conflict hasn’t changed the rules of global finance overnight. It’s changing them through accumulated decisions by central bankers, finance ministries, and corporate treasurers who have noticed, often quietly, that the assumptions they had been operating under no longer apply. By the time those decisions show up in IMF reserve tables or in the relative weights of payment networks, the rewriting is well advanced.

Much of Washington still behaves as if a global system organized around dollar settlement were the default state of the world. Gulf oil ministers, Chinese state banks, Indian refiners, and reserve managers from Riyadh to Brasília are operating as if it were a feature under negotiation. The closure of Hormuz has pushed both sides into the same conversation at the same time.

Sanctions as Settlement Risk

The US sanctions program has expanded into something close to an industrial process. The Office of Foreign Assets Control has designated more than 1,000 Iran-related persons, vessels, and aircraft since February 2025, with monthly enforcement actions branded under the Treasury campaign “Economic Fury.”

Recent rounds have targeted shadow banking networks moving currency for Iranian counterparties and the independent Chinese refineries known as teapots, which absorb roughly 90% of Iran’s crude exports, according to Treasury Department alerts. Those alerts warn the global financial sector that secondary sanctions are now plausible against any foreign bank, insurer, or shipper with material exposure to that trade.

The posture is familiar to anyone who watched the response to Russia’s invasion of Ukraine four years earlier. The lasting consequence wasn’t the seizure of $300 billion dollars in Russian reserves itself. It was the demonstration effect. Reserve managers in capitals from Riyadh to New Delhi saw how rapidly assets parked in dollar instruments could be reclassified as instruments of policy enforcement and they began slowly reducing single-jurisdiction exposure.

Sanctions designed to cut Iranian financial flows reach across borders into the Chinese banks, Indian refiners, Emirati commodity traders, and Turkish intermediaries that handle the underlying transactions. Each of those institutions then faces a choice. They can continue the trade and accept compliance risk in dollar markets, or they can rewire the trade so the relevant balances are settled outside the dollar system entirely. For an increasing share of the world’s oil flows, the second answer has become operationally feasible in a way it was not five years ago.

Hormuz and the Energy-Finance Link

When Iran formally closed the Strait of Hormuz on March 4, global markets experienced something they had not contemplated for decades. Roughly a fifth of the world’s oil and a comparable share of liquefied natural gas suddenly stopped moving through a single narrow passage.

The International Energy Agency reported that global oil supply contracted by 10.1 million barrels per day in March and authorized the release of 400 million barrels from emergency stockpiles, the largest coordinated draw in its history. Brent crude punched through $120 in the immediate aftermath before drifting lower in early May. West Texas Intermediate has tracked Brent’s moves within the same range.

Fatih Birol, the IEA’s executive director, told the Financial Times in March that the conflict represented “the greatest global energy security threat in history,” a formulation he has repeated in subsequent interviews. Strategic releases buy weeks, not months. Refineries that normally process Persian Gulf grades can’t easily substitute and have throttled output.

The disruption is now visible in parts of the economy that directly touch American households. Jet fuel prices in many markets have more than doubled within weeks. Diesel costs have risen enough to feed through to trucking rates, freight insurance, and the operating expenses of any business with meaningful energy exposure. American mortgage rates near 7%, business borrowing tied to long-end Treasury yields, and homeowner-insurance premiums repricing for the third consecutive year all sit atop the same shock. The energy and financial stories are becoming harder to separate.

The Hormuz shock first appeared in crude prices, but the financial transmission has been broader. As energy prices repriced, long-end Treasury yields also moved higher, tightening the same borrowing conditions that feed into mortgages, corporate debt, and federal interest costs. Source: FRED, Market Yield on U.S. Treasury Securities at 30-Year Constant Maturity; FRED/EIA, Brent crude oil price.

Nondollar Oil Routes Move From Symbolic to Practical

Behind the energy headlines is a parallel financial story. Iran is reported to be charging yuan-denominated transit tolls on tankers permitted to pass under emerging informal arrangements. Indian refiners, no longer able to source Iranian volumes, are settling alternative Russian crude purchases in yuan and Emirati dirhams, bypassing dollar clearing. Taken alone, none of these moves changes the scale of dollar invoicing in oil. Taken together, they describe a meaningful slice of trade now operating outside U.S. banking infrastructure.

The petrodollar arrangement was already weakening before the war. A handful of pilot transactions between China and Saudi Arabia in renminbi had been treated as symbolic. The closure of Hormuz, layered on top of secondary sanctions enforcement, has turned some symbolic alternatives into operational ones. The cost of routing around dollar settlement appears to have fallen below a threshold that matters for some counterparties.

Reserve Managers Were Already Adjusting

The slow reweighting of central bank reserves is the clearest evidence that the dollar’s primacy is being adjusted in real time. The IMF survey published on March 27 placed the dollar share of allocated foreign-exchange reserves at roughly 56.8% at the end of 2025. That share was above 70% at the turn of the millennium. The euro, the renminbi, and a broader category of nontraditional reserve currencies have absorbed the difference at varying speeds.

Gold has been the most visible beneficiary of the trend. The World Gold Council reported that central banks bought roughly 863 tonnes of bullion in 2025, modestly below the postwar record set the prior year but well above the historical average. The Council’s industry forecast points to roughly 850 tonnes of additional purchases in 2026.

Central banks have not abandoned the dollar, but their reserve behavior has changed. The dollar’s share of allocated reserves has drifted lower over the past two decades, while official-sector gold buying has remained unusually elevated since the geopolitical shock of 2022. Source: IMF COFER; World Gold Council, central-bank gold demand.

Poland’s central bank alone added 102 tonnes last year and has continued to accumulate. Buyers in Turkey, India, and a quiet but persistent set of Middle Eastern and Southeast Asian central banks have followed similar paths. The motivation, by their own statements, is the desire to hold a reserve that cannot be frozen by a foreign jurisdiction.

Central bank reserve surveys conducted by groups such as the Official Monetary and Financial Institutions Forum, which tracks reserve managers and sovereign investors, point in a consistent direction. A substantial majority of reserve managers polled over the past year have expected the dollar’s share of reserves to decline moderately or significantly within five years, with most identifying geopolitical fragmentation and sanctions risk as the primary drivers. The pattern reflects a constituency whose forward intentions are now being supplied by mainstream institutions rather than contrarian analysts.

Former Treasury Secretary Janet Yellen acknowledged the trajectory in remarks at the Brookings Institution in January. “If market participants lose confidence in the likelihood of serious future deficit reduction,” she said, “rising risk premia could trigger a debt spiral and pressure the dollar.” Coming from a former Treasury principal, in a year when the federal deficit has run above 5% of GDP and net interest has crossed the trillion-dollar threshold, that’s closer to a warning sign than academic framing.

Dollar Dominance Still Has Defenses, For Now

The opposite case still has some weight. Dollar liquidity remains unmatched in scale, and U.S. capital markets are deeper by an order of magnitude than those of any competitor today. The renminbi remains only partially convertible, and Chinese capital controls limit the size of any reserve allocation that international managers are willing to commit. The Gulf currency pegs, the Saudi riyal at 3.75 since 1986 and the Emirati dirham at 3.67 since 1997, impose limits on how aggressively those economies can move into yuan settlement without unwinding their own monetary frameworks. Dollar invoicing in global trade has barely moved over the past two decades.

Secondary sanctions are powerful in part because they’re difficult to defy openly. A Chinese state bank, a Turkish trading house, or an Indian energy firm can’t easily ignore a credible threat of exclusion from dollar markets. The cost of a single enforcement action against a major foreign institution would cascade across that institution’s correspondent banking relationships and import financing for years. Compliance has long been cheaper than designation.

Inside the New Payment Pipes

That math shifts when the universe of compliant counterparties grows large enough to support an alternative payment route. The BRICS expansion to eleven members, including Saudi Arabia, the United Arab Emirates, and Iran, has given that route political coherence.

The mBridge cross-border platform, jointly developed by the central banks of China, Hong Kong, Thailand, and the United Arab Emirates with the BIS Innovation Hub before the BIS exited the project, has reportedly processed payments in the tens of billions of dollars, most denominated in digital yuan.

None of these platforms is a substitute for dollar pipes. But a reserve currency doesn’t have to be replaced all at once to begin losing its grip. Each marginal transaction that clears outside the dollar reduces the habit, the necessity, and eventually the political leverage embedded in the system.

The Iran war has stress-tested those assumptions. Independent Chinese refineries continue to take Iranian crude through obscured supply chains despite repeated Treasury alerts. The financial settlement for those purchases has, by necessity, migrated into renminbi clearing channels. Indian refiners have replaced Iranian barrels with Russian alternatives, again clearing in nondollar currencies.

Even Gulf actors have begun to hedge their structural dollar dependence. In April, Khaled Mohamed Balama, governor of the Central Bank of the United Arab Emirates, warned American officials that depleted dollar liquidity could force Abu Dhabi to sell oil in yuan.

The warning carried weight because of the policy response that followed. Treasury Secretary Scott Bessent publicly endorsed an emergency dollar swap line for the United Arab Emirates. Within days, Abu Dhabi announced its departure from OPEC and OPEC+. A public American offer of dollar liquidity, followed almost immediately by a Gulf decision to exit a dollar-anchored cartel, captured the asymmetry of the moment. Washington still has enormous power to supply dollars. The problem is that it increasingly has to use that power to keep partners inside the system.

Gulf pegs to the dollar remain in place, and the structural constraints they impose mean any move into yuan settlement would be incremental rather than wholesale. But reserve systems usually weaken this way. Not through a single declaration, but through exceptions that become tolerable, then routine, then expected. Each yuan-priced cargo, each rupee invoice, each dirham settlement leaves a record that aggregates over time.

War Premiums Reach the Treasury Curve

The most direct financial transmission of the conflict back into the United States runs through the Treasury borrowing calendar. The thirty-year yield crossed 5% in early May for the first time in months. The benchmark ten-year sits above 4.4%. Some Wall Street strategists argue that a significant share of the recent move reflects a geopolitical risk premium that has widened since the strikes on Iran began, though the exact breakdown is disputed. The thirty-year is trading near the top of its five-year range.

These yield levels don’t principally reflect the Federal Reserve’s policy stance. They reflect a combination of higher inflation expectations from the oil shock, a rising fiscal financing requirement, and a more reluctant marginal buyer. Each force was present before the war. Each has sharpened since. The bear-flattening pattern visible across the curve in April and early May is the kind of move that traders associate with supply concerns at the long end rather than with shifts in the policy path.

A repricing of that size has consequences far beyond the federal balance sheet. Mortgage rates respond. Corporate borrowing costs respond. Refinancing decisions inside private equity portfolios respond. Each percentage point of higher long-term yields adds tens of billions of dollars to projected federal interest expense over the rolling refinancing window. Net interest is already running above $1 trillion per year on a public debt stock of over $32 trillion. A persistent shift higher in long-end yields converts a heavy fiscal burden into a constraining one.

Demand-side dynamics are where the war’s effect on de-dollarization meets the mechanics of Treasury auctions most directly. Foreign private investors now account for a larger share of foreign Treasury holdings. That makes the foreign bid more sensitive to hedging costs and relative-value comparisons than when official reserve managers held the dominant share.

If hedging costs rise, foreign demand may adjust. If alternative reserve assets attract more flows, it may adjust again. A sanctions episode that reprices the legal risk of holding U.S. paper could have the same effect. Those shifts would show up at the margin, through weaker auction demand and larger concessions.

The dollar borrowing calendar, which absorbed roughly $20 trillion in net issuance over the past two decades, was designed under different assumptions about who the marginal buyer would be. Nothing here points to a failed Treasury auction or a sudden loss of market access. Investors are still buying U.S. debt. They’re just demanding more compensation to hold longer-term bonds. That higher cost now includes a clear war premium. And that premium may not disappear just because a ceasefire is announced.

A Pricier Dollar Franchise

The dollar isn’t collapsing. That framing isn’t useful for understanding what’s actually changing. The better question is what the dollar is turning into. Its status is no longer considered settled. It’s becoming something other countries negotiate around, hedge against, and price more carefully. Reserve managers in major capitals have already adjusted their balance sheets. U.S. households and private investors are moving more slowly, partly because the daily experience of using dollars at home doesn’t feel different.

The connection between abroad and home is real even when it’s invisible. A war premium and a fiscal premium are not separate inputs when both appear on the same yield curve. Mortgage rates, insurance premiums, fuel costs, and the cost of corporate borrowing all bear the weight of decisions made by distant central banks.

The institutional response to all of this has converged on a vocabulary that’s decades old. Central banks talk about diversification. Sovereign wealth funds talk about regime uncertainty. Insurers discuss asset-liability matching in fatter-tail scenarios. Pension trustees talk about real-asset overlays. The wording changes, but the instinct remains the same. They’re looking for assets that don’t depend on one government’s funding calendar or one sanctions regime staying stable.

Gold has had a specific role in that shift. Central bank buying accelerated after 2022 because many reserve managers learned the same lesson. Assets held inside another country’s financial system can be frozen, restricted, or repriced by political decision. Continued gold buying through 2025 and into 2026 doesn’t make gold the only hedge for this environment. But it does make it one of the few assets whose appeal rises with the exact risk now being repriced.

The war with Iran will eventually find a settlement. Oil will find a price. Auctions will continue to clear. What will be harder to sustain is the assumption that the dollar’s central role can be drawn on as a free resource for sanctions enforcement without affecting the underlying franchise. The dollar’s role isn’t inherited. It must be maintained.