By Preserve Gold Research

For much of the last two years, the idea of a soft landing has rested on a quiet kind of confidence. Inflation was no longer spiraling as it had earlier in the decade. Labor markets began easing. Central banks seemed to be moving toward a stage where restraint could gradually give way to normalization. It was never an easy outcome to engineer. It was one, however, that still seemed within reach.

That confidence now looks less like a settled judgment and more like a price set under narrower assumptions. The soft landing story hasn’t collapsed outright, but it’s being repriced because the world that was supposed to deliver it has changed. An energy and shipping shock tied to conflict around Iran and the Strait of Hormuz has widened the range of plausible outcomes exactly when policymakers were hoping the distribution of risks would narrow. That matters because a soft landing depends on more than inflation drifting lower. It depends on the system remaining governable while it slows.

A Calm Baseline Starts to Fray

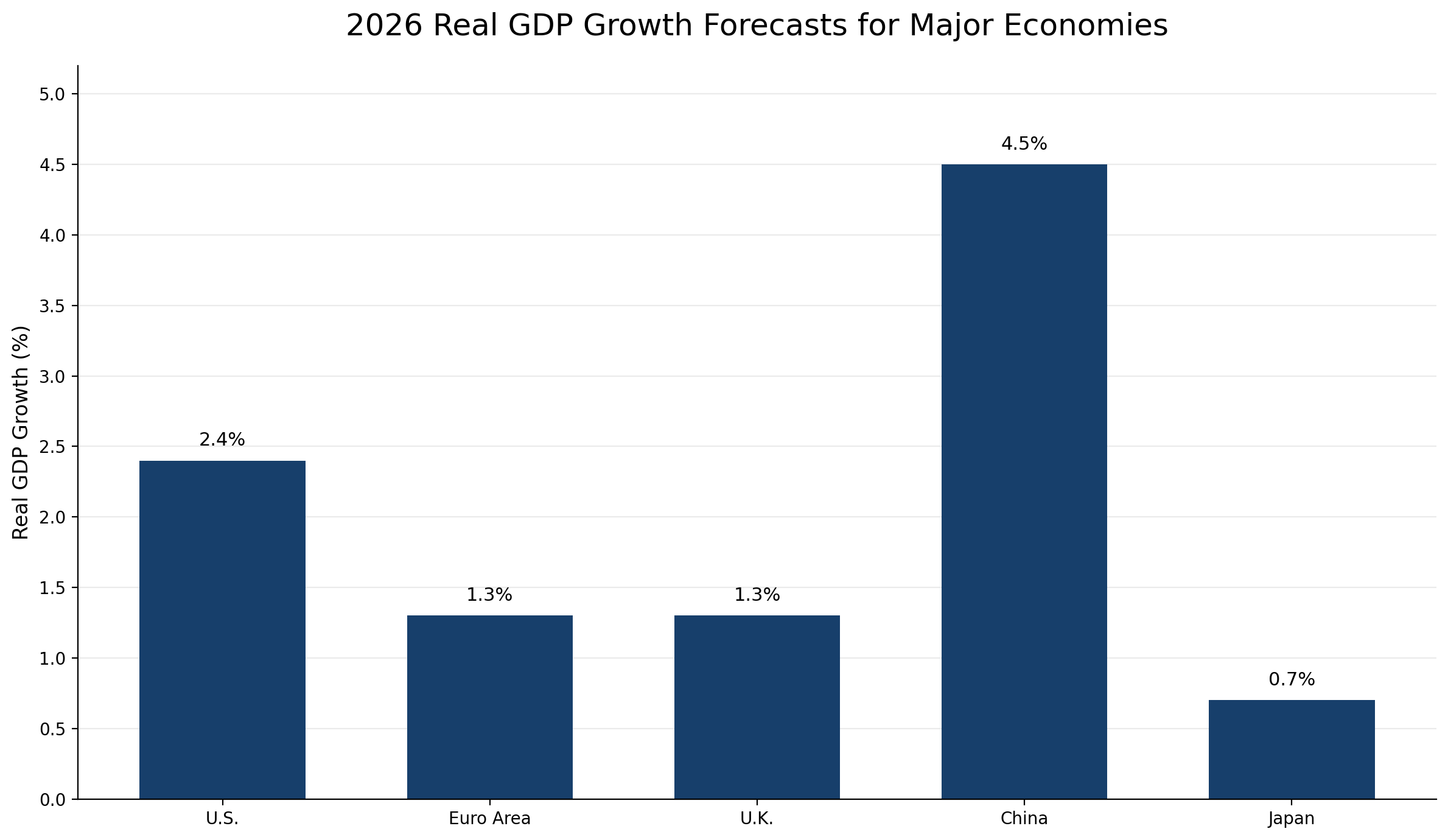

The original case for optimism wasn’t irrational. By late 2025, the broad trend in many advanced economies was encouraging enough to support the view that disinflation could continue without a deep contraction. The International Monetary Fund (IMF) still expected “resilient” growth in 2026 across the major economies, including about 2.4% for the United States, 1.3% for the euro area, 1.3% for the United Kingdom, 4.5% for China, and 0.7% for Japan. Those aren’t booming numbers, but that is the point. A soft landing doesn’t require a strong expansion. It requires just enough growth to absorb tighter financial conditions without tipping the entire system into a self-reinforcing downturn.

IMF 2026 GDP forecasts show why the soft landing narrative survived into this year, even as global growth became too thin to absorb another shock easily. Source: IMF, World Economic Outlook Update (January 2026).

That baseline also depended on a subtle but important assumption. It assumed that the next phase of the cycle would be driven mainly by demand management. In other words, central banks could stay focused on the familiar problem of cooling demand, guiding inflation expectations, and deciding when policy had become restrictive enough. Once that was the frame, the path ahead seemed difficult but manageable. Inflation could fall. Rates could eventually come down. Labor markets could soften in an orderly way. The economy could glide rather than break.

From Demand Cooling to Supply Shock

The problem with 2026 is that the frame has changed from demand normalization to supply disruption. Supply shocks don’t give policymakers clean trade-offs. They raise prices while simultaneously weakening real activity. The result is a different kind of macro tension.

Higher energy costs work like a tax on households and firms. They lift headline inflation, compress margins, disrupt shipping, and reduce disposable income simultaneously. Monetary policy can’t produce more oil, reopen a chokepoint, or instantly repair global logistics. It can only try to prevent the inflationary effects of the shock from spreading into wages, services, and expectations.

That’s why the repricing of the soft-landing narrative is showing up not only in commentary but also in markets. Breakeven inflation moved higher in the shock window, high-yield spreads widened, and long-end sovereign yields became more erratic. Those moves suggest investors are assigning more weight to outcomes that had previously been treated as tails. The market is no longer pricing a smooth transition from restrictive policy to gentle easing. It’s pricing a world in which inflation can reassert itself even as growth loses momentum.

Less Cushion, More Inflation Risk

The most important point here is not that the economy has suddenly become weak in a conventional sense. In several places, it hasn’t. The US entered this period with real GDP growth in late 2025 still running at a solid pace, and labor-market deterioration remained limited rather than disorderly. The euro area was still growing, if modestly. China’s early-2026 activity data pointed to a reasonably firm start. Japan remained in its own distinctive position, with lower inflation than many peers but meaningful sensitivity to imported energy costs and exchange-rate pass-through. None of that looks like an economy already in recession. What it looks like is a global system with less margin for error than the soft landing consensus had assumed.

That lost margin is what makes central banking in 2026 so constrained. If policymakers ease too quickly into an energy-driven inflation hump, they risk sending the message that any renewed price pressure will be tolerated. If they hold policy tight for too long, they can turn an external supply shock into a broader income and credit shock.

In previous phases of the cycle, there was at least some hope that incoming inflation data would steadily improve, allowing a more straightforward policy transition. Now the task is more defensive. Central banks are trying to distinguish between a temporary impulse and the beginning of a more durable inflation problem without causing damage in the process.

Michael S. Barr of the Federal Reserve has been explicit about the danger in that distinction. During a late-March speech, Barr warned that a shock initially seen as temporary can seep into expectations and become persistent. “We have had five years now of inflation at elevated levels, and near-term inflation expectations have risen again, so I am particularly concerned that yet another price shock could increase longer-term inflation expectations.“ A central bank can often live with a first-round rise in energy prices if it believes the effect will wash out. What it can’t easily tolerate is a second-round process in which wage setting, services pricing, and market expectations begin to absorb the shock and extend it. Once that happens, the cost of restoring credibility rises sharply.

The International Energy Agency (IEA) has added an equally important perspective from the real side of the economy. It described the Middle East conflict and the disruption through Hormuz as “the largest supply disruption in the history of the global oil market.” That language matters because it captures the scale of what policymakers are being forced to absorb. This isn’t a routine commodity fluctuation. It’s the kind of event that can reshape inflation expectations, alter capital flows, and expose the fragility of growth forecasts that looked reasonable under calmer assumptions.

The OECD’s interim assessment pointed in the same direction. Its emphasis was not on a simple inflation scare or a simple growth scare, but on the uncomfortable coexistence of both. That’s exactly what makes the current environment so difficult to map. In a classic slowdown, falling yields and weaker demand can eventually create the conditions for relief. In a classic inflationary problem, central banks can tighten policy amid strong economic activity. A supply shock scrambles that logic. It can leave policymakers facing weaker output and stronger price pressure at the same time, which is why the language of risk management has become so prominent.

Central Banks Are Managing Exposure, Not Certainty

That phrase can sound evasive, but in this context it’s actually revealing. Risk management means policymakers no longer feel they are steering toward a known destination along a mostly known road. They are trying to preserve optionality in a landscape where each move creates new exposures.

The Federal Reserve’s cut-and-pause sequence fits that pattern. So does the Bank of England’s reluctance to move quickly in the face of still-firm wage growth. So does the European Central Bank’s dilemma as an energy-sensitive economy contends with weak trend growth and renewed price pressure. Even the Bank of Japan, operating in a very different domestic setting, is pulled into the same global logic through imported inflation and exchange-rate transmission.

That same constraint also shows up on the labor side of the equation, because it determines whether an energy shock remains external or becomes domestic. In the US, labor conditions have cooled from the extreme tightness of the earlier post-pandemic period, but not in a way that suggests a broad collapse in demand.

In the United Kingdom, wage growth has remained relatively firm even as headline inflation has fallen from its peak, making it harder to extinguish services inflation fully. In the euro area, growth has been softer, yet energy sensitivity and wage dynamics still complicate the path back to target.

Japan adds a different wrinkle, because even moderate inflation can matter more after a long period of very low price growth, especially when imported costs and the exchange rate are doing much of the work. These differences matter because there’s no single global reaction function anymore. Each central bank faces the same shock through a different domestic transmission mechanism.

That heterogeneity is one reason the next few quarters are likely to be defined less by bold policy pivots than by hesitation, qualification, and conditional language. Investors often want central banks to offer a clean map, but no such thing exists today.

If oil stabilizes and shipping adjusts, policymakers may be able to resume the slow normalization that had seemed plausible before the shock. If not, they may have to spend months explaining why policy can’t respond as markets had expected. Central banks understand that once credibility is weakened in an inflationary environment, the cost of restoring it is usually paid later and at a higher price.

Headline CPI and core CPI have moved closer together in 2026, but the gap still shows why households feel energy-driven price shocks differently from the inflation measures policymakers emphasize. Source: U.S. Bureau of Labor Statistics via FRED, Consumer Price Index for All Urban Consumers: All Items and All Items Less Food and Energy in U.S. City Average.

From there, the difference between headline and core inflation can’t be treated as a footnote. Households don’t consume the core index. They experience energy, transport, food, and rent in real time, and those experiences shape sentiment, wage demands, and political pressure.

Central banks may argue that a supply shock should be looked through in part, but if households begin to believe that the overall cost structure of the economy is rising again, that belief can become self-fulfilling. Expectations aren’t abstract. They influence the timing of purchases, the aggressiveness of pay demands, firms’ pricing decisions, and markets’ tolerance for policy patience.

Three Outcomes Now Compete for the Cycle

This is where the soft landing narrative becomes less a forecast than a probability distribution. A true soft landing is still possible. If shipping disruptions ease, oil flows stabilize, and wage growth cools before expectations begin to drift, the inflation impulse could prove temporary enough for central banks to hold their ground without tightening further.

In that world, growth slows but stays positive, credit stress remains manageable, and the shock becomes a hump rather than a regime change. The soft landing survives, but in a thinner form than before. It would no longer mean a smooth descent. It would mean the system absorbed an external shock without losing control.

Yet there is another path in which the shock operates less through headline prices and more through household and corporate balance sheets. Higher energy costs drain purchasing power. Higher shipping and input costs eat into profit margins. Wider credit spreads make refinancing harder. Consumers pull back. Firms cut investment.

A sequence that begins as inflation pressure ends by looking more like a recession. That’s the hard landing path, and what makes it dangerous is not merely lower growth. It’s the possibility that financial conditions tighten endogenously, amplifying the shock beyond what central banks intended.

The third path, and arguably the one markets are beginning to take more seriously, is stagflation. That word is often used too casually, but its relevance here isn’t hard to see. If inflation remains elevated while energy and logistics constraints persist, and growth weakens under their weight, then the policy framework becomes much more uncomfortable.

Duration hedges don’t work as cleanly as they would in a normal recession. Equities face pressure from both margins and discount rates. Credit suffers from wider spreads and slower activity. Policy itself becomes politically and institutionally harder because every tool seems to solve one problem by worsening another.

The reason these scenarios matter is that they shift attention away from point forecasts and toward the system’s transmission channels. The key variables now are not only headline CPI or one month of payrolls. They are pass-through, expectations, and resilience. How much of the energy shock shows up in consumer prices? How much gets absorbed by firms? Do households start behaving as if inflation will remain structurally higher? Do workers bargain for compensation that locks the shock into services inflation? They determine whether the shock fades or settles into the cycle’s structure.

They also explain why market behavior since late February has been so informative. Higher breakevens suggest inflation compensation is rising. Wider high-yield spreads suggest investors see more downside risk in growth and credit quality. Elevated volatility suggests confidence in a narrow macro outcome has weakened.

Even the behavior of long-term yields has reflected the tension between two fears that would normally move markets in opposite directions. One fear says inflation persistence requires tighter policy and higher premia. The other says weaker growth will eventually drag yields lower. When both stories are live at the same time, repricing becomes more violent because the old macro map no longer provides a clean signal.

Fiscal and Trade Fault Lines Reappear

Beyond markets, there’s also a political dimension that shouldn’t be ignored. Over the last several years, many advanced economies have run with larger deficits, higher debt loads, and less fiscal room than markets had become accustomed to before the pandemic era. The IMF has warned that larger deficits and elevated debt can push long-term rates higher and tighten financial conditions. In a benign disinflation environment, that’s manageable.

In a shock environment, it matters much more. Fiscal vulnerability can magnify the pressure already created by energy prices and monetary uncertainty. It can turn what would have been a temporary strain into a longer-lasting premium on risk assets and sovereign debt.

Trade fragmentation adds another layer. Even before the latest Middle East disruption, the global economy was already operating with more geopolitical friction, more industrial policy, and less certainty about supply chains than in the pre-pandemic period. A soft landing was easier to imagine in a world where trade remained broadly efficient, and logistics were resilient enough to absorb shocks. It becomes harder to imagine when the same system is also coping with energy chokepoints, strategic rivalry, and a more fractured investment backdrop. The economy doesn’t need to stop growing for these pressures to matter. It only needs to become less adaptable.

Before this shock, the optimistic case already required central banks to keep expectations anchored while labor markets cooled gently and financial conditions remained stable. Now it requires all of that plus a contained energy disruption, limited second-round inflation, and no serious spillover into credit or fiscal stress. The destination is the same, but the bridge leading to it has become narrower.

Repricing Forces a Different Kind of Strategy

For investors, that means regime insurance matters more than narrative loyalty. Portfolios built on the assumption that disinflation will continue in a straight line are more exposed than they were a few months ago. Inflation hedges no longer look like relics of an earlier phase.

Duration needs to be thought of conditionally, not automatically, because it behaves differently in a hard landing than in a stagflationary slowdown. Credit quality matters more than broad beta when the distribution of outcomes widens. None of that implies panic. It implies humility about the way macro regimes can change when a supply shock collides with a fragile policy transition.

For companies, the challenge is more operational but no less strategic. Pricing power matters again. So does balance-sheet durability. Firms that assumed logistics costs would normalize smoothly may now have to think more seriously about hedging, inventory, refinancing windows, and the geographic concentration of suppliers. An energy shock doesn’t hit every sector equally, but it pushes almost every management team back toward questions they hoped were fading: how much cost can be passed through, how fast, and at what demand penalty? When the macro backdrop becomes less predictable, corporate margins for error tend to shrink faster than consensus expects.

For policymakers, the lesson is not that they must choose between growth and inflation in a dramatic one-time decision. It’s that credibility now depends on clarity about what kind of shock they are facing and how they will react if it persists. They can’t treat every rise in headline inflation as proof that policy must tighten further. Nor can they assume that a supply-driven surge will harmlessly fade on its own. They have to separate first-round effects from embedded persistence while preserving financial stability. That’s a narrow corridor, and the fact that it’s narrow is itself the signal.

More broadly, the post-pandemic economy was already teaching policymakers a difficult lesson before this year’s escalation in the Gulf. Inflation had become more sensitive to supply conditions, geopolitics, labor tightness, and fiscal posture than the old models were comfortable admitting. The latest shock reinforces this lesson. A soft landing in this environment is not just about calibrating rates correctly. It’s about whether the broader system can absorb repeated disruptions without allowing them to bleed into expectations, pricing behavior, and long-term risk premia.

That’s why a growing number of analysts, like PWC’s US Chief Economist Dr. Alexis Crow, believe the economy has entered a phase in which stability can no longer be taken at face value. Growth may still hold up for a time. Labor markets may still look serviceable. Inflation may even remain near tolerable levels in some jurisdictions. But beneath that surface, the balance has become more precarious. The narrative has shifted from confidence in a managed slowdown to recognition that the slowdown is now being negotiated under external stress.

Ultimately, that is what repricing means. The market, policymakers, and businesses are all being forced to admit that the old baseline was built for a calmer world. A soft landing remains possible, but it’s no longer the default story that everything else bends around. It’s one scenario among several, and the others have become harder to dismiss. When a cycle reaches that point, the real signal is that the system no longer has the luxury of assuming that time alone will solve the problem.