By Preserve Gold Research

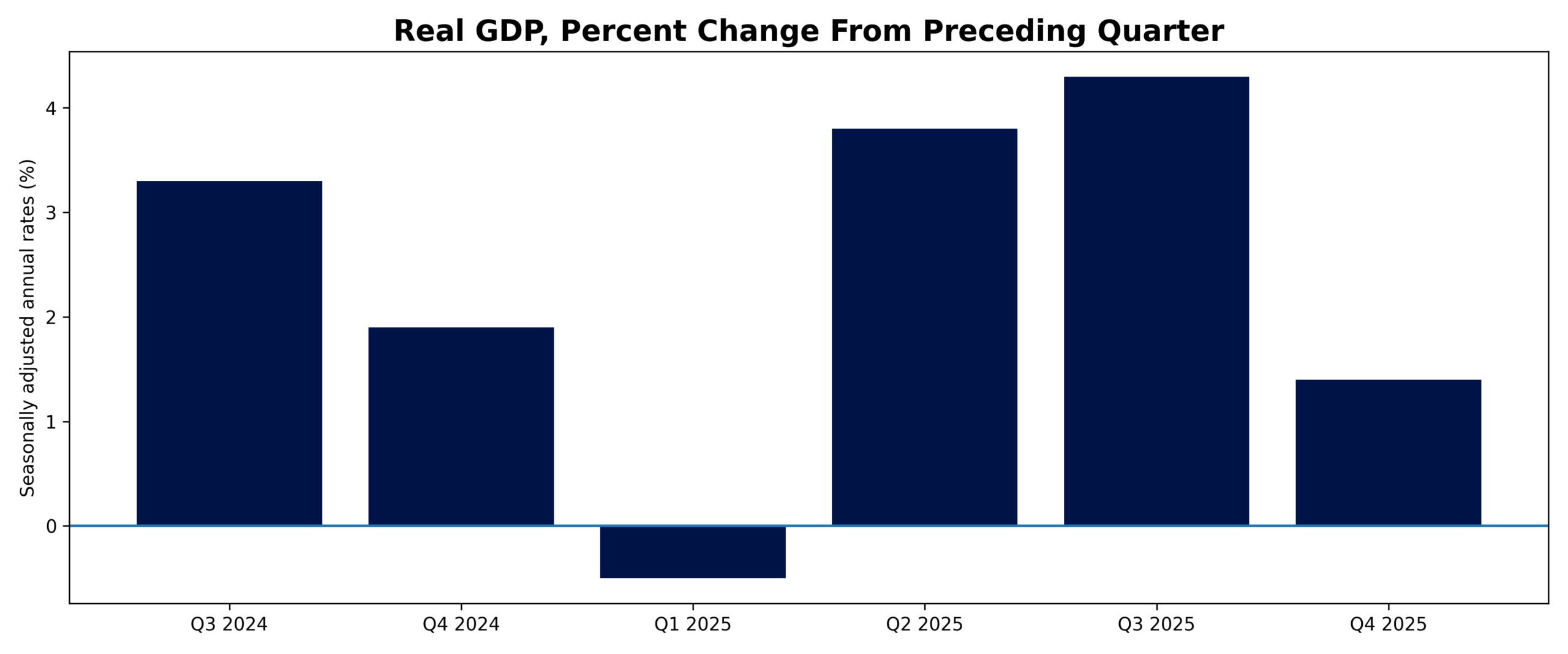

The U.S. economy nearly hit the brakes at the end of last year, expanding at an annualized pace of only 1.4% in the fourth quarter. That marked a sharp drop from the 4.4% surge seen in the summer and was well below forecasts of around 3%. This weaker-than-expected finish represents a dramatic downshift from the July-September quarter’s 4.4% growth and the 3.8% rate notched in Q2. Analysts attribute the abrupt slowdown largely to a six-week federal government shutdown and a late-year pullback in consumer spending, both of which took a noticeable toll on economic momentum.

The temporary halt in federal operations (the longest in U.S. history at 43 days) proved to be a self-inflicted drag on growth. The Commerce Department estimated that the spending freeze and lost work hours shaved roughly one full percentage point off fourth-quarter GDP. At the same time, American consumers grew more cautious as autumn turned to winter. Consumer spending rose at a modest 2.4% rate for the quarter, a decent gain but far slower than the 3.5% jump recorded over the summer. Many households have relied on credit and dwindling savings to sustain their purchases, something that economists warn may not be sustainable going forward. The personal saving rate fell to one of its lowest levels since 2008’s recession, reflecting the financial strain on families even as they keep spending.

Despite the headline slowdown, underlying economic activity remained resilient. A core measure of private-sector demand (which combines consumer outlays and business investment) still grew at a “mostly healthy” clip in the quarter, even after volatile trade swings are set aside. “Consumers and companies spent at a ‘reasonably solid’ pace,” observed Martha Gimbel, an economist at Yale, noting that “this is not a disastrous report” overall. Nevertheless, the stark loss of speed from earlier in 2025 has laid bare growing cracks beneath the surface.

AI-Driven Investment Masks Broader Business Caution

Households remained the engine of growth in late 2025, but their power waned. Consumer spending increased 2.4% in Q4, down from a robust 3.5% gain in the prior quarter. In practical terms, Americans kept shopping, but not with the same vigor as over the summer. Economists note that more consumers are leaning on debt and reducing savings to finance purchases.

By the end of the year, the nation’s saving rate had slipped to 3.6%, a level last seen only during the 2008 Great Recession. This suggests many families are stretching their finances to maintain living standards. Rising prices for essentials like food and gasoline earlier in the year, coupled with higher borrowing costs, have left households with less budgetary cushion. While holiday sales held up decently, the downshift in consumption growth hints at fragility. If wage gains slow or credit tightens, consumer spending, which comprises about 70% of the economy, could weaken further.

That vulnerability in private demand might have been manageable on its own. Instead, it has collided with a sudden retreat in public spending. Business on Capitol Hill ground to a halt last fall, and so did a sizable chunk of federal outlays. A funding impasse led to a six-week partial government shutdown from early October to mid-November. Thousands of federal employees were furloughed, and many services were suspended. Federal government expenditures plunged nearly 17% on an annualized basis in the fourth quarter as everything from agency payrolls to procurement contracts was delayed or reduced.

According to the Bureau of Economic Analysis, this collapse in public-sector activity directly knocked roughly 1 percentage point off GDP growth. Absent the shutdown, fourth-quarter growth might have been closer to 2.4% instead of 1.4%. Much of that damage should be temporary as agencies resume spending and back pay is distributed. Even so, the episode underscores the real economic costs of political stalemates. As EY-Parthenon chief economist Gregory Daco describes it, the shutdown amounted to a “self-inflicted” wound that left the economy hobbling on one less leg.

After a late-2024 slowdown and a brief contraction in early 2025, growth rebounded sharply through mid-year before cooling again into Q4. The headline numbers suggest resilience. The quarter-to-quarter swings suggest fragility. Source: U.S. Bureau of Economic Analysis.

After a late-2024 slowdown and a brief contraction in early 2025, growth rebounded sharply through mid-year before cooling again into Q4. The headline numbers suggest resilience. The quarter-to-quarter swings suggest fragility. Source: U.S. Bureau of Economic Analysis.

With both consumers and government spending losing momentum, greater weight fell on corporate America to sustain growth. Businesses did continue investing, but not evenly. Overall, fixed investment posted moderate gains in late 2025, but most capital outlays were concentrated in a narrow cluster of booming sectors. Companies poured money into data centers, artificial intelligence infrastructure, and related equipment.

Outside of the high-tech arena, investment was noticeably softer. Many firms held back on expanding capacity or upgrading facilities, reflecting caution amid higher borrowing costs and uncertain demand. “The report reflected a ‘one-legged’ economy boosted mostly by artificial intelligence,” observed Diane Swonk of KPMG, noting that AI-related spending is fueling business growth while lifting asset values for investors.

An outsized share of 2025’s economic vibrancy has come from what economists describe as the “three A pillars”: affluent consumers, AI-driven investment, and asset price appreciation. These narrow drivers have propped up growth even as more traditional capital outlays languish. The risk is that if the tech frenzy cools or wealthier households pull back, there are few other pillars as sturdy to support the economy’s weight.

External trade, meanwhile, offered little reinforcement. Unlike earlier in the year, trade was neither a major tailwind nor a serious drag in the fourth quarter. Net exports were neutral for growth after swinging wildly in previous quarters. Over the summer, U.S. GDP had been artificially lifted by a one-time quirk. Imports plunged as businesses front-loaded purchases earlier in 2025 to get ahead of new tariffs. That import drop flattered the Q3 growth numbers (since fewer imports mathematically boost GDP).

By Q4, however, those effects faded. Companies were no longer stockpiling foreign goods, so imports stabilized. Exports, meanwhile, faced headwinds from a slowing global economy and a strong dollar, offsetting the modest decline in imports. The result was that trade neither added to nor subtracted much from growth at the end of last year. For an economy that had briefly benefited from shrinking trade deficits, the return to the status quo meant no extra buffer against domestic weakness. Looking ahead, the trade outlook remains murky. With tariff policy still evolving after recent court rulings and global growth uneven, the external sector remains a variable rather than a safeguard. Any escalation of trade tensions or a global slowdown in 2026 could quickly turn trade into a more significant drag on growth.

Renewed Inflation Pressures Delay Rate Cuts

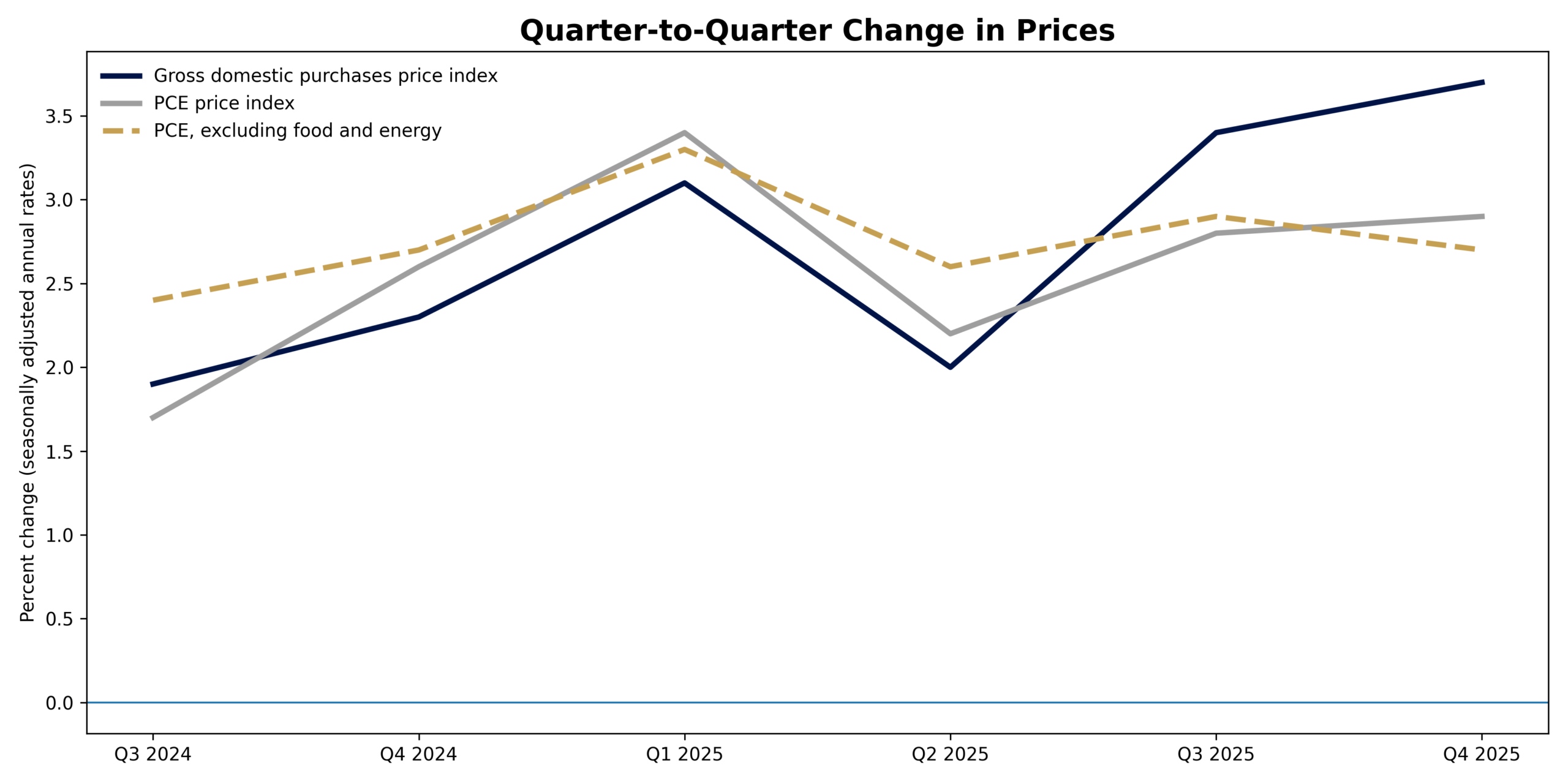

After cooling for much of last year, inflation showed unwelcome signs of acceleration at the end of 2025. The Federal Reserve’s preferred price index accelerated in December, with costs for goods such as furniture, clothing, and groceries rising more briskly than in prior months. This firming of inflation coincided with the GDP slowdown, creating a bind for policymakers.

After cooling in mid-2025, price pressures began firming again into Q3 and Q4. Headline PCE remains elevated, while core inflation shows persistence beneath the surface. Source: U.S. Bureau of Economic Analysis.

Normally, a cooling economy would ease price pressures, but underlying inflation appears sticky, driven in part by rising wages and still-resilient consumer demand. The late-year uptick dashed hopes that the Fed might start cutting interest rates early in 2026. Instead, officials have signaled they will likely hold rates high for longer, or even consider additional hikes, until price growth convincingly eases. The combination of a cooler economy and persistent inflation has echoes of stagflation, though not quite at crisis levels. For households, however, any renewed rise in everyday prices is unwelcome news, further straining budgets already thinned by a low saving rate.

GDP Growth Without Job Gains Raises Concerns

One of the most peculiar features of the current expansion is the modest job growth despite solid output. In 2025, U.S. GDP grew a respectable 2.2%, yet employers added fewer than 200,000 jobs over the entire year, the smallest gain since the pandemic downturn in 2020. Typically, growth that strong would be accompanied by millions of new hires. Instead, inflation-adjusted economic activity has risen without the typical surge in payrolls. This disconnect reappeared in the fourth-quarter data as the economy expanded, but unemployment actually edged up from 4.0% to 4.3% by year’s end. Businesses are producing more without proportionally increasing headcount.

Economists have proposed several explanations for this growth-jobs gap. One factor is demographics and policy. The Trump administration’s crackdown on immigration sharply curtailed the inflow of new workers, slowing labor force growth. With population growth subdued, the labor force is expanding only gradually, thereby inherently limiting the number of jobs that can be filled.

Another force complicating the labor picture is technological substitution. Companies are turning to automation and artificial intelligence instead of hiring for a growing number of roles. Layoff data at the start of the year sent an uncomfortable signal. Employers announced over 100,000 job cuts in January, more than triple the prior month’s total and more than double the level recorded a year earlier. The only January that registered worse came in 2009, during the depths of the Great Recession. Of those cuts, over 7,000 were directly attributed to AI.

“It’s difficult to say how big an impact AI is having on layoffs specifically,” said Andy Challenger, Chief Revenue Officer at Challenger, Gray & Christmas, but “the market appears to be rewarding companies that mention it.” Since 2023, tens of thousands of job cuts have been linked, at least in part, to artificial intelligence, and some analysts believe the true number is higher than reported. The broader implication is not that machines are suddenly replacing entire workforces overnight, but that firms are steadily recalibrating how much labor they truly need. If productivity can be lifted through software and automation, output can expand without proportional increases in payroll. For job seekers, that shift may prove more consequential than any single round of layoffs.

Automation, however, hasn’t happened in isolation. The same executives weighing AI efficiencies are also navigating tighter profit margins. Lingering cost pressures from tariffs, wage demands, and higher input prices have forced companies to scrutinize expenses more closely. Policy uncertainty adds another layer of hesitation, discouraging long-term hiring commitments. Taken together, these forces reinforce the view of an economy that continues to produce and even grow, but with a thinner layer of new employment beneath it. That can hold for a period. Over time, though, an expansion that fails to translate into broader income growth risks eroding its own support.

Policy Uncertainty Weighs on Business Confidence

The fourth-quarter slowdown has unfolded amid contentious economic policymaking in Washington. In February, a major White House trade initiative was upended when the Supreme Court struck down many of President Donald Trump’s sweeping tariffs, ruling that he had overstepped his authority. Those tariffs, imposed on a wide range of imports, had slightly lifted inflation and complicated supply chains. After the court’s decision, Trump vowed to reinstate tariffs under different legal grounds, seeking to continue his protectionist agenda. The uncertainty around trade policy has left many businesses in limbo, unsure whether tariff relief will be lasting or whether new import taxes will loom.

At the same time, the partisan standoff that caused the government shutdown became fodder for a blame game. President Trump lambasted congressional Democrats for the funding lapse, claiming the “Democrat Shutdown cost the U.S.A. at least two points in GDP” in lost growth. (Most economists consider that figure exaggerated, though the shutdown’s drag was significant.) Trump also renewed pressure on the Federal Reserve, berating Fed Chair Jerome “Too Late” Powell for not slashing interest rates and insisting that high rates were holding the economy back. The central bank, for its part, has maintained that its policies are necessary to curb inflation despite political pressure.

These crosscurrents came to a head as President Trump prepared to deliver his State of the Union address in early 2026. Just weeks before the speech, he had confidently predicted a “blowout” GDP growth figure above 5%, even accounting for the shutdown. Instead, the official data told of a sharp slowdown.

Nevertheless, the administration signaled it would tout the economy as “booming” and at its “strongest point in history,” highlighting low unemployment and stock market records while downplaying the weak year-end figures. This disconnect between rhetoric and reality is not lost on observers. It underscores how economic data can be spun in different ways heading into an election year: one narrative emphasizes resilience and prosperity, another sees warning signs of sputtering momentum. For Americans, the truth likely lies in between—the economy is growing, but it’s far from invincible.

Why Strong GDP Feels Weak to Many Americans

Beneath the aggregate numbers, 2025’s economy feels less like a single story and more like two unfolding at once. On the surface, key indicators looked strong, with output growing steadily, inflation easing from its highs, and joblessness remaining low. Yet many Americans say they feel squeezed, uncertain, or simply tired of waiting for relief. Consumer confidence in January fell to its lowest level since 2014, a reminder that official strength doesn’t always translate into lived security. The question is not whether the economy is growing. It’s why so many people feel as though it isn’t working for them.

Part of the answer lies in the uneven distribution of the gains. Economists often describe the pattern as “K-shaped,” but the lived reality is simpler. Some households are moving ahead quickly, while others are holding their ground at best. Families with investments have benefited from rising asset prices and the surge in technology spending. Portfolio gains create confidence, and confidence supports spending.

Meanwhile, many lower- and middle-income households are barely treading water. Their spending has held up, but often out of necessity rather than optimism. Credit balances have climbed while Pandemic-era savings cushions have thinned. For many workers, pay increases have struggled to keep pace with housing, insurance, and food costs. The headline growth rate fails to reflect this nuance.

This divide helps explain the sour mood. Americans still see high grocery bills and hear about layoffs in rate-sensitive industries. Many confront rents or mortgage payments that consume a larger share of income than they once did. Lingering memories of past downturns (from the 2008 crisis to the brief 2020 plunge) have also heightened people’s caution.

In surveys, respondents cite concerns about political instability, rising costs, and the sustainability of the expansion. Their caution shows in behavior too: even as they spend, people are seeking cheaper alternatives, scaling back big purchases, or postponing major life decisions. Until the benefits of growth broaden and the threats (inflation, job insecurity) clearly recede, optimism is likely to remain restrained.

A Fragile Expansion Beneath the Headline Numbers

Step back from the quarterly swings, and a clearer picture emerges. The economy is still growing, but many experts say that it’s growing more fragile. On the surface, the United States has avoided recession. Output is rising, consumers are spending, and businesses are investing in select areas.

Yet the underpinnings of that growth look increasingly precarious. Households have propped up consumption by burning through savings and amassing debt. But that bridge won’t stretch forever. Government spending, usually a stable contributor, was so volatile that it whipsawed the quarterly figures. Business investment is imbalanced, reliant on a tech-centric boom that may or may not spread benefits across the economy. And the labor market’s peculiar stall raises concerns about the economy’s capacity to generate broad-based prosperity.

As economist Diane Swonk cautioned, “The economy looks golden on paper, but beneath the surface is lead.” What appears healthy in aggregate glosses over pockets of weakness and structural stress. For Americans warily eyeing the road ahead, the message is clear. All that glitters in the headline figures is not gold, and preparation for leaner times may be wise.