By Preserve Gold Research

Few areas of the economy make the gap between headlines and lived reality clearer than housing. The data can say the pressure is easing. The index rises. The median household income again clears the qualifying threshold. The deepest part of the shock appears to be over. But that doesn’t mean the market feels any more accessible to the people trying to enter it. In 2026, that’s the real tension in housing. Affordability is improving by the measures that create optimistic headlines. But for a large share of Americans, it doesn’t feel improved at all.

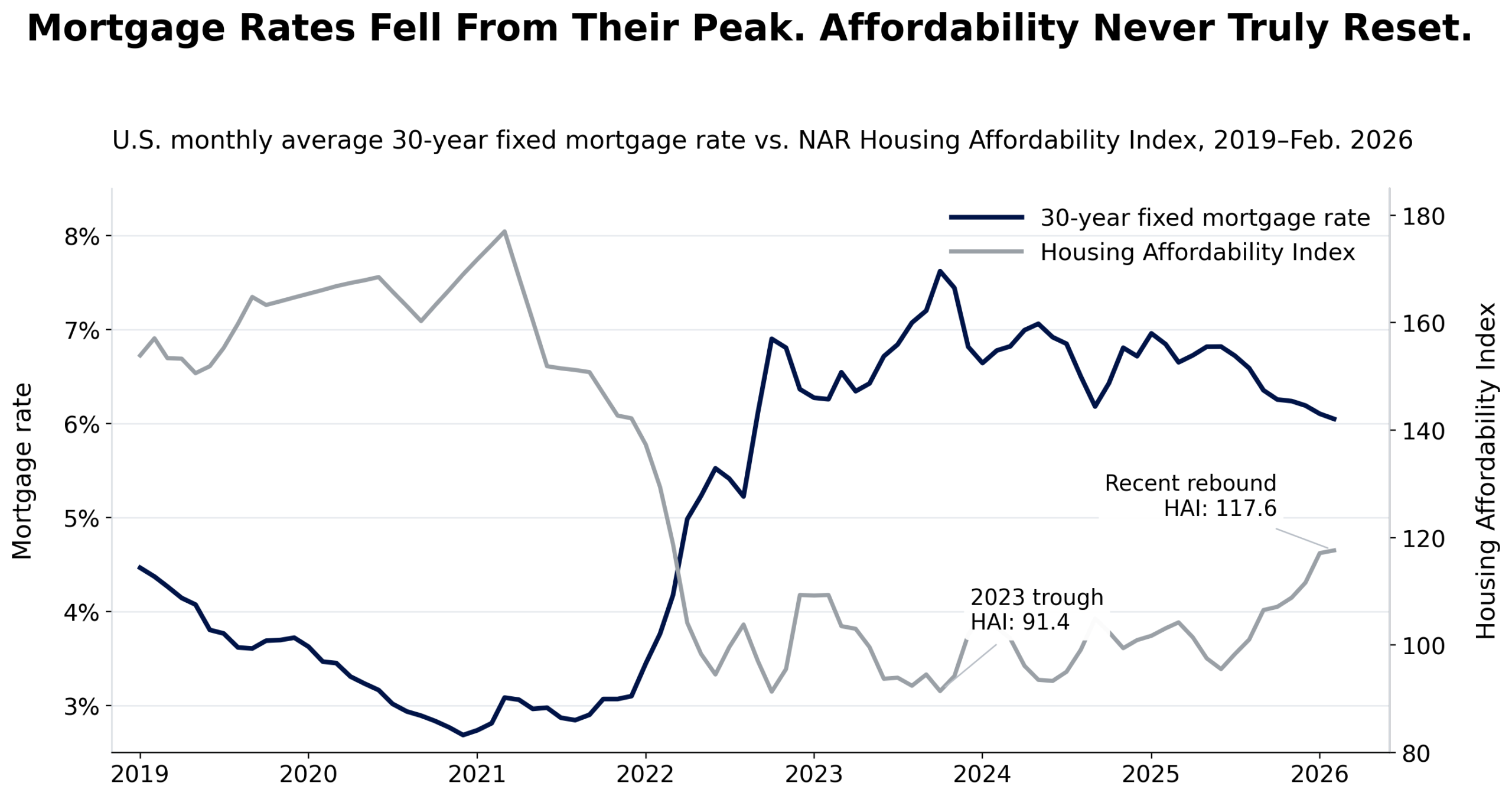

That disconnect matters because it gets at something deeper than a monthly data point. February 2026 showed a rebound in the National Association of Realtors’ Housing Affordability Index, with the fixed-rate reading rising to 117.6, the strongest level since March 2022. Under the organization’s framework, that means the median-income family now earns enough to qualify for a mortgage on a median-priced home. On the surface, that looks like relief. It looks like a market that’s begun to heal. But the emotional and financial reality of housing does not reset the moment a median threshold is crossed. A market can improve from crisis conditions and still remain inaccessible, fragile, and psychologically punishing for the people living through it.

Headline Progress Meets Household Reality

That’s especially true because the recent collapse was anything but mild. NAR’s 2023 affordability reading came in at 96.9, below the level that signals whether the median family can qualify under its assumptions. The payment-to-income ratio exceeded the group’s own cost-burden benchmark. By modern standards, it was one of the harshest affordability episodes in decades. So when current data show improvement, what they’re really saying is that conditions are less severe than they were at the bottom. They aren’t saying that the market has become comfortable again. They’re not even saying it’s become broadly workable.

That distinction is where much of the current confusion begins. The housing story is often told through the language of stabilization. Rates are off their peaks. The affordability index has bounced. Credit conditions are not as restrictive as they were during the worst phase of the shock. But most households don’t live inside a stabilization narrative. They live inside monthly payments, down payment requirements, insurance bills, moving costs, and a broader sense that ownership keeps drifting farther away, even as the data technically improve. What looks like progress in aggregate can still feel like paralysis at ground level.

Rates Have Fallen, but Borrowing Still Hurts

Mortgage rates remain one of the clearest reasons for that gap. The violent rate shock of 2022 and 2023 changed the market structure long before prices had time to adjust meaningfully. Housing is unusually exposed to that kind of move because it’s typically financed with long-duration debt. When borrowing costs jump by several percentage points in a short period, affordability can deteriorate even if home prices merely stop climbing. The financing cost does the damage first. That’s why so many would-be buyers experienced the market not as mildly more expensive, but as suddenly and fundamentally unattainable.

Those financing pressures have eased somewhat, but not nearly enough to restore the conditions people remember from the low-rate years. In the February 2026 affordability calculation, NAR used a mortgage rate of 6.12% on a median-priced existing single-family home of $401,800, resulting in a monthly principal-and-interest payment of $1,952. Freddie Mac’s weekly survey put the average 30-year fixed rate at 6.46% as of April 2, 2026. Those figures are lower than the most punishing spikes of the tightening cycle, but they’re still far above the rates that shaped buyer expectations just a few years ago. The technical direction is better. The lived experience is still one of expensive money.

Home prices have done little to close that emotional gap. The median existing-home price stood at $398,000 in February 2026, while Census and HUD data placed the median price of new homes sold in the fourth quarter of 2025 at $405,300. Those aren’t the numbers of a market that has meaningfully reset. They are the numbers of a market that absorbed a rate shock, slowed down, and then continued operating under conditions of scarcity. Buyers are being asked to finance expensive assets with expensive debt, and then accept that the resulting strain counts as an improvement because it’s less brutal than before.

That’s why so many Americans hear that affordability is improving and instinctively reject the claim. In a narrow statistical sense, the claim is true. In a broader household sense, it feels false. A family that could not justify the payment in late 2023 may now find the math slightly less impossible. But “slightly less impossible” isn’t how people experience hope or access. It’s how they experience continued exclusion with better marketing around it. The improvement is real. It is simply not large enough, widespread enough, or durable enough to register as meaningful relief for much of the country.

Scarcity Still Sets the Terms

Supply constraints are a major reason the market has not reset more forcefully. Existing-home inventory stood at 1.29 million units in February, equal to a 3.8-month supply. That’s better than the most depleted conditions of the post-pandemic period, but it’s still not what most analysts would consider a balanced market. A housing market can’t become broadly affordable very quickly when the stock of available homes remains limited. It can become less overheated. It can become less chaotic. But it doesn’t become easy.

That shortage has several layers. Some of it is physical, tied to years of underbuilding and the slow pace of new supply. Some of it is financial, driven by higher costs for land, labor, materials, and insurance. Some of it is behavioral, because millions of existing owners remain locked into mortgages originated at rates dramatically below today’s levels. Selling a home now often means giving up financing near 3% and replacing it with debt in the mid-6s. That lock-in effect suppresses resale inventory even when households might otherwise want to move. The result is a market that stays tighter than standard economic logic would suggest. People are not only priced out of buying. Many current owners are disincentivized from selling.

Builders have continued to add homes, with housing starts running at a 1.487 million annualized pace in January 2026 and permits at 1.386 million, but that’s not the same thing as a catch-up boom. The market is not experiencing the kind of supply surge that would materially reset affordability, especially for entry-level buyers. In many places, builders are still pushed toward larger or more expensive homes because that’s where margins are more defensible.

Easier Credit Does Not Mean Real Relief

Credit conditions complicate the story further. During the worst phase of the affordability shock, the banking system did tighten meaningfully. The Federal Reserve’s Senior Loan Officer Opinion Survey showed standards for GSE-eligible mortgage loans shifting from mild easing in early 2022 to clearer tightening by late 2023, with the net share of banks tightening peaking in the fourth quarter of that year. That mattered because it made an already expensive market harder to access. Yet by late 2025 and into early 2026, the same survey showed a return to net easing for conforming mortgages.

That sounds encouraging, and in one sense it is. But it also reveals why people don’t feel much better. Credit access can improve even as housing remains unaffordable. Easier lending standards don’t undo the arithmetic of elevated prices and still-high mortgage rates. They may help some marginal borrowers cross the line. They don’t, however, restore a sense of margin, comfort, or safety. The market is not only asking whether a household can qualify. It’s asking whether that household can absorb the full cost of ownership without feeling overextended from the beginning.

That is where headline measures begin to lose contact with lived experience. NAR’s index assumes a 20% down payment and a 25% qualifying ratio for principal-and-interest costs. Those assumptions are useful for standardization. They are less useful for describing how buyers actually experience the market. Many households are constrained not only by the monthly payment but also by the cash needed to enter at all. Others may technically qualify but still feel exposed once taxes, insurance, maintenance, commuting costs, and other household expenses are factored in. Qualification is a threshold. Affordability, in real life, is a cushion. And cushions remain thin.

The First-Time Buyer Squeeze

That helps explain why the housing narrative feels so dissonant right now. The middle of the market may look better on paper, but the broader distribution still looks bleak. NAR’s own work estimates that only about a third of households can afford a median-priced home under its qualifying framework, and that only 17% of renters can afford the median-priced starter home. Those figures get closer to the reality people recognize. The problem is that the path to ownership now depends more heavily on prior wealth, accumulated equity, family assistance, or the ability to tolerate a severe payment burden. Today, the market isn’t just sorting by income. It’s sorting by balance sheet.

The worst of the affordability shock has passed, but the rebound has been modest relative to the scale of the mortgage-rate surge that broke buyer math in the first place. Source: Freddie Mac, 30-Year Fixed-Rate Mortgage Average; National Association of Realtors, Housing Affordability Index.

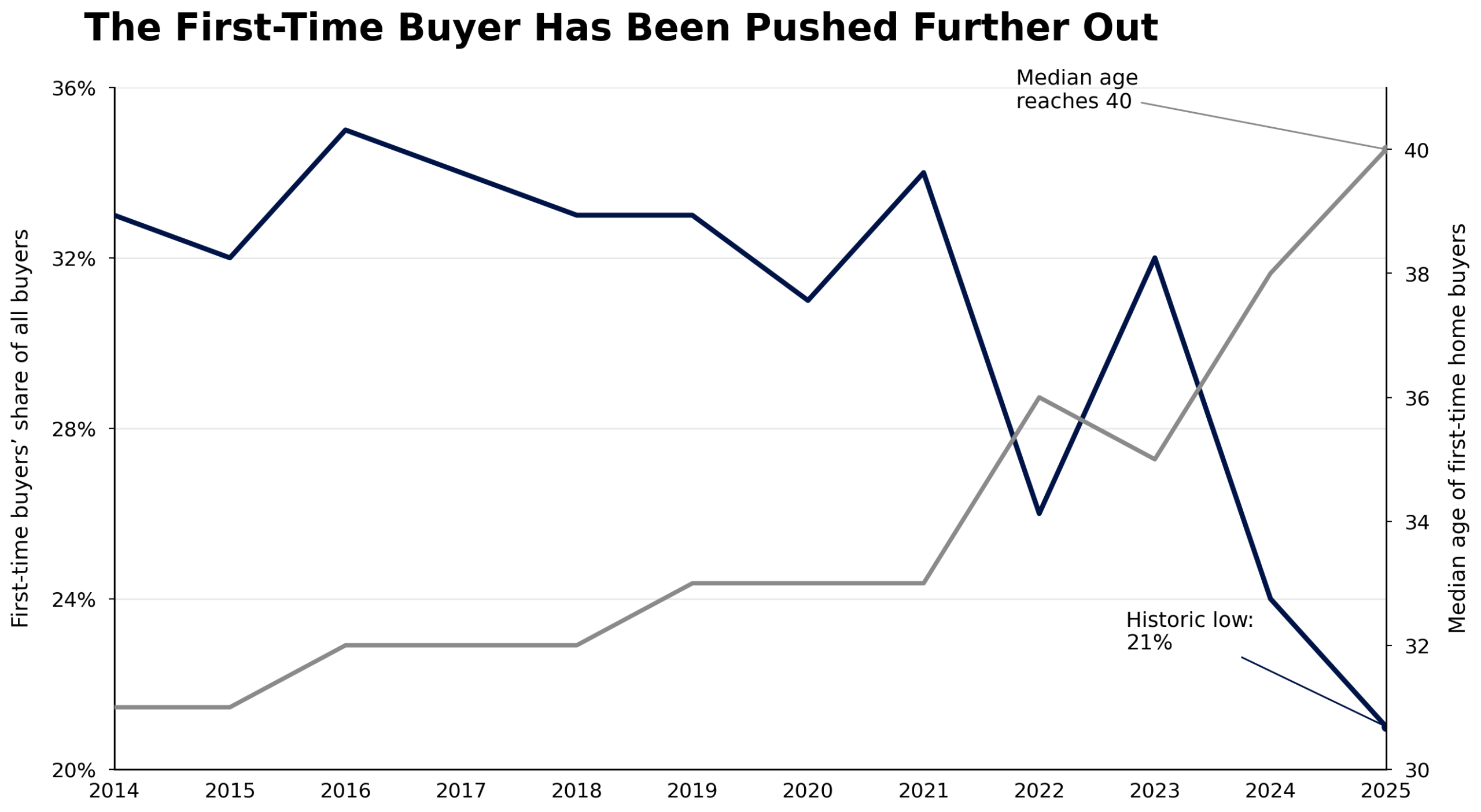

That sorting is most visible in the first-time buyer data. Traditionally, the first home didn’t need to be perfect. It needed to be reachable. It was the rung that let households convert rent into equity and begin building their own financial stability. In the current market, that rung has moved higher and become harder to grasp. NAR’s survey evidence showed first-time buyers falling to 21% of all buyers, a historic low, while the median age of a first-time buyer rose to 40. Repeat buyers arrived with stronger positions, whether through equity, larger down payments, or the ability to pay cash. Nearly a third of repeat buyers paid cash.

That’s more than a quirky market statistic. It’s a sign that the ownership ladder is being restructured around preexisting advantage. When the people succeeding in the market are disproportionately those who already own assets, the claim that affordability is improving sounds almost beside the point. Improving for whom is the more relevant question. Improving relative to what is the second. For households trying to buy their first home with earned income and limited savings, the answer often feels like not enough and not really.

Regional differences make the same point in sharper form. In February 2026, NAR’s fixed-rate affordability index stood at 150.2 in the Midwest, 121.4 in the South, 105.6 in the Northeast, and just 84.5 in the West. The national story, therefore, conceals enormous variation in how the market is actually lived. A median-based national reading can imply that conditions are improving while large parts of the country remain functionally exclusionary. The West, in particular, continues to show how little comfort there is in national averages when local prices are doing most of the speaking.

The first-time buyer has been pushed further out, with the share of first-time purchasers falling to a record low even as the median age of entry rises. Source: National Association of REALTORS®, Profile of Home Buyers and Sellers, annual reports, 2014-2025.

When Housing Strain Spreads Through the Economy

That matters because housing stress doesn’t remain confined to the housing sector. When ownership becomes harder to reach, households don’t just downgrade their ambitions and move on unchanged. They delay marriage. They postpone children. They stay in smaller rentals longer. They move farther from job centers. They become more dependent on family help or accept longer commutes and thinner savings cushions. The strain begins as a shelter issue but quickly spreads to labor mobility, family formation, consumer behavior, and wealth transmission. Housing is not only a monthly payment. It’s one of the main ways a society organizes stability over time.

The rental market absorbs part of that pressure. If would-be buyers remain renters longer, demand in rental housing stays firmer than it otherwise would. Rent growth has slowed from the earlier inflation surge, but it remains positive, and the rental vacancy rate of 7.2% in the fourth quarter of 2025 does not describe a market flooded with slack. Housing stress has a sideways quality. If a household can’t buy, it pays through rent. If it can’t move, it pays through a forgone opportunity. If it can’t qualify with enough breathing room, it pays through permanent financial anxiety. The cost is redistributed, not removed.

That’s why the current improvement feels so fragile. The system is telling people conditions are better, but the underlying structure that made housing feel punishing is still largely intact. Rates remain elevated relative to the last cycle. Prices remain high. Supply remains constrained. Entry-level stock remains limited. Down payment barriers remain significant. Insurance and carrying costs remain heavy in many markets. Even where the formal numbers say the market is healing, households face a reality that still feels brittle and unforgiving.

A Recovery That Still Does Not Feel Real

Simple explanations, therefore, fail. The problem isn’t just the Federal Reserve, though the rate shock mattered immensely. It’s not just underbuilding, though supply scarcity is central. It’s not just tighter credit, though that deepened the pain when affordability was already collapsing.

It’s the interaction of multiple constraints that reinforce one another. Years of insufficient supply left the market with little room for error. Then the inflation fight drove mortgage rates sharply higher. Then, owners stopped moving because their old loans were too attractive to surrender. Then prices proved sticky because the supply shortage never truly disappeared. The result is a market that can improve at the edges while still feeling fundamentally broken to the people who need it most.

A March 2026 Brookings analysis framed part of the issue in structural terms, arguing that affordability problems are unusually difficult to resolve in supply-constrained markets because price pressures are being generated by local scarcity as much as by national financial conditions. That helps explain why the current phase feels so unsatisfying. Lower rates alone would help, but they would not create enough homes in the areas with the most entrenched shortages. More supply would help, but it would come slowly and unevenly. Income growth would help, but often not fast enough to keep pace with home prices and financing costs in the hardest-hit regions. Every path to relief exists. None of them is clean.

That leaves the next phase of the housing market looking less like a recovery than a negotiation. If mortgage rates stay in the mid-6% range and incomes continue to rise, the burden can keep easing at the margins. The recent affordability reading suggests that normalization is possible. But normalization is not restoration. A market that becomes less punishing can remain out of reach for the households who most need a workable entry point. That’s the mistake in much of the current commentary. It treats the absence of further deterioration as if it were the return of genuine access.

The downside risk isn’t hard to imagine either. Housing remains highly sensitive to rates. If inflation proves sticky, if broader market volatility lifts mortgage spreads, or if financing costs return to 7%, affordability could deteriorate quickly again. The experience of 2023 showed how abruptly buyer math can worsen and how quickly the market mood can change. A renewed tightening in bank standards would only intensify that effect, especially for households with thinner savings or more fragile credit profiles. In other words, the improvement people are being told to appreciate is not only limited. It’s conditional.

The more optimistic path is real, but narrower than many headlines imply. It would require sustained disinflation, lower mortgage rates, continued income growth, and a more convincing supply response, particularly in entry-level housing. Even then, the gains would be uneven.

Regions with lower price levels and fewer supply constraints would recover more quickly. High-cost coastal markets would remain difficult unless something changed more fundamentally in land use, permitting, and the economics of building smaller, cheaper homes. The best-case scenario is a slower, partial repair that leaves major access problems unresolved.

That’s also why demand-side policy on its own tends to disappoint. If the bottleneck is scarcity, subsidies can temporarily make the market seem easier to enter while still pushing prices higher in constrained areas. The more durable response is a supply-first one, but that phrase becomes much harder once it has to pass through zoning fights, permitting reform, infrastructure demands, financing realities for builders, and local political systems that have often spent years defending less housing rather than more. Affordability isn’t a single national number waiting to be nudged upward. It’s a local governance problem, a balance-sheet problem, and a structural supply problem layered together.

For lenders and regulators, the challenge is more subtle. The goal is to avoid turning a structurally difficult market into an even more procyclical one. Safe borrowers shouldn’t be shut out indiscriminately during periods of stress. But neither should policymakers pretend that access alone can solve the math of high prices and expensive financing.

Better Numbers, Same Emotional Reality

This cycle has made one thing clear: access and affordability are related, but they’re not the same. That may be the most important truth beneath the current housing story. The market is no longer falling under the force of a fresh rate shock. By some headline measures, it’s stabilizing. But most Americans don’t evaluate housing based on whether the emergency is technically over. They evaluate it by whether ownership feels any closer, any safer, or any more realistic than it did before. For many, it doesn’t. The numbers are improving. The feeling is not.

That’s why the current optimism around affordability rings hollow to so many households. A system can stop getting worse without becoming healthy. It can stabilize without becoming fair. It can post better numbers while still feeling deeply misaligned with the lives it is supposed to support. Until supply broadens meaningfully, financing costs come down decisively, or incomes begin to outrun housing costs in a sustained way, much of the country will continue to hear that the housing market is improving while having little reason to believe it.