By Preserve Gold Research

When OpenAI closed a $122 billion funding round at an $852 billion post-money valuation in late March, the figure was hard to miss. But it did not immediately read like a warning. Private markets had already become used to huge valuations for frontier AI companies. The more important signal was what was happening around it.

Brent crude climbed to $138 a barrel by April 7, according to the EIA’s May 2026 Short-Term Energy Outlook. The Federal Reserve finished a stability assessment that described the equity premium as “well below its historical average.” At the same time, private credit was showing a quieter but more unusual strain. For the first time since perpetual business development companies were created, accepted redemptions exceeded new inflows. These funds pool private loans and sell access to investors, and the shift suggested that confidence in one of the fastest-growing corners of credit was starting to weaken.

Inside the Fed’s Stability Warning

The Fed’s May 2026 Financial Stability Report brought those risks together. Asset prices were still stretched. The S&P 500’s price-to-earnings ratio remained near the high end of its historical range. Geopolitical risk and a possible oil shock drew the most concern in the Fed’s survey of market contacts. But they weren’t alone. AI valuations, private credit strains, and the risk of a sharp correction in risk assets had entered the same conversation.

The report’s language was careful, but not casual. The Fed stated that AI capital spending is increasingly “funded by debt, creating leverage in the system.” It warned that stress in private credit could “spill over into broader credit markets.” While the statements were brief, they carried weight. Together, they suggested that today’s optimism in public markets may be resting on a growing base of leverage, and that pressure in private credit could travel faster and wider than investors expect.

The concentration in public stock markets is already clear, even if investors may not fully grasp what it means. As of mid-May 2026, Nvidia’s market value was near $5.52 trillion. Alphabet stood at $4.81 trillion, Microsoft at $3.14 trillion, Amazon at $2.87 trillion, Broadcom at $2.07 trillion, and Meta at $1.57 trillion. The S&P 500 shows the same pattern. The largest company now makes up 7.9% of the index by itself. The top 10 companies together account for 38.5%. Semiconductor and semiconductor-equipment stocks add another 18%.

That gives a small group of companies enormous influence over the broader market’s direction. For investors in passive funds or index-based portfolios, this is not a short-term imbalance. It is now built into the market’s structure.

Passive investing, by design, puts more money into the companies that are already the largest. That means many investors are betting that today’s biggest companies will stay on top. The concern is that today’s biggest companies are tied to one powerful technology cycle, AI, in a way that has few clear historical comparisons.

Debt Behind the AI Buildout

The financing behind those companies adds a further layer. The four major hyperscalers (Alphabet, Amazon, Microsoft, and Meta) are on track to spend more than $600 billion on AI-related infrastructure in 2026. Alphabet has guided for full-year capital expenditure of $175 billion to $185 billion, most of which will be allocated to technical infrastructure. Meta raised its own 2026 guidance to $125 billion to $145 billion, then sold $25 billion of investment-grade bonds. Public debt markets are now directly helping to finance the AI spending race.

A BIS bulletin published in early 2026 made that shift clear. Major AI hyperscalers have nearly doubled capital spending over the past two years. They’re also relying less on internal cash flow and turning more to long-term debt.

The BIS March 2026 Quarterly Review added another concern. Some AI infrastructure is being financed through deals with private-credit investors and insurers, while banks provide funding lines or guarantees. The BIS said these arrangements can act like debt even when they do not appear directly on corporate balance sheets. That means risk may be building in areas that normal financial reports do not clearly show.

Microsoft’s AI business was reported to have passed the $37 billion annual revenue run rate, suggesting real demand behind the investment boom. But spending is still moving at a pace that even strong revenue growth may struggle to support. If confidence in AI were to weaken for an extended period, the damage would not stop with stock prices. It could also tighten credit conditions for companies that borrowed heavily to keep up.

Private Marks, Public Consequences

Private market valuations have followed a similar trajectory. When Anthropic closed a $30 billion funding round in mid-February at a $380 billion post-money valuation, the number was striking on its own. xAI had already raised $20 billion in January. The two rounds were not outliers so much as anchors for what the first quarter became.

Venture deal value for Q1 2026 reached $267.2 billion, according to PitchBook and the National Venture Capital Association. Five transactions accounted for nearly three-quarters of that total. The AI-specific figure for the quarter surpassed the full-year 2025 AI venture total in three months.

Numbers at that scale carry a structural implication. Private market valuations are set infrequently and rarely contested between funding rounds. A company marked at $380 billion may or may not trade near that price in continuous markets. The marks still matter regardless. They shape what lenders will extend, set the floor for future round negotiations, and, in some cases, directly determine the stated asset values of funds with concentrated exposure. Valuation revision doesn’t need to be sudden to have consequences.

From Niche Credit to Systemic Exposure

Private credit has grown alongside this. The Federal Reserve estimated that U.S. private-credit loans reached approximately $1.4 trillion in the second half of 2025, equal to roughly 10% of total U.S. nonfinancial corporate debt. The FSB’s May 2026 report on private credit vulnerabilities placed the global figure at between $1.5 trillion and $2 trillion. Moody’s projects that private-credit assets under management will approach $4 trillion by the end of the decade. That growth has carried the market from a niche alternative into territory where its behavior affects broader credit conditions.

Borrower leverage within that market runs high. The FSB estimated debt-to-EBITDA ratios, the ratio of what a company owes relative to what it earns before standard accounting deductions, of 5x to 6x across the sector. With earnings adjustments common in leveraged deals factored in, the effective figure is potentially closer to 7x. S&P Global Ratings put median leverage at 6.64x in 2025, confirming the trend holds across the market as a whole. At those levels, a market of that size is no longer insulated from broader financial conditions.

Bank of Canada Governor Tiff Macklem has said publicly that private credit is genuinely difficult to assess from the outside. “Our oversight was built for banking,” he said. “Non-bank players generally don’t have the same reporting requirements or level of monitoring. That gap poses a challenge for global standard-setters, national regulators, and central banks.” The terms lenders attach to loans, and the leverage embedded in individual deals, are not readily visible in available reporting.

The FSB’s report identified a further complication. Leverage is layered across a chain. It sits at the portfolio company, the private-credit fund, the sponsor, and the investor financing the fund. Each layer seems manageable on its own, but together they can amplify a shock well beyond what any individual participant anticipates.

The regulated banking sector’s exposure to these structures isn’t trivial. Bank credit commitments to nonbank financial institutions reached $2.6 trillion in Q4 2025, the Federal Reserve reported. A reclassification update found that roughly a quarter of those commitments went to private equity, business development companies, and private credit. That segment grew faster than overall bank commitment growth to nonbanks in 2025. Banks do not hold these assets on their loan books directly. They provide the funding lines, warehouse facilities, and backstops that keep the nonbank credit structure running. The exposure is real even when it does not appear as a conventional loan.

A segment of private credit has also reached retail investors directly. Funds that allow periodic withdrawals but hold largely illiquid underlying assets had grown to several hundred billion dollars in net assets by early 2026. The Fed’s report found that redemption requests rose materially in late 2025 and into Q1 2026. Managers used contractual caps. The system held. But the episode made something visible: when retail sentiment shifts and questions about credit quality surface, even structures with built-in redemption limits face genuine pressure.

Software’s New Collateral Problem

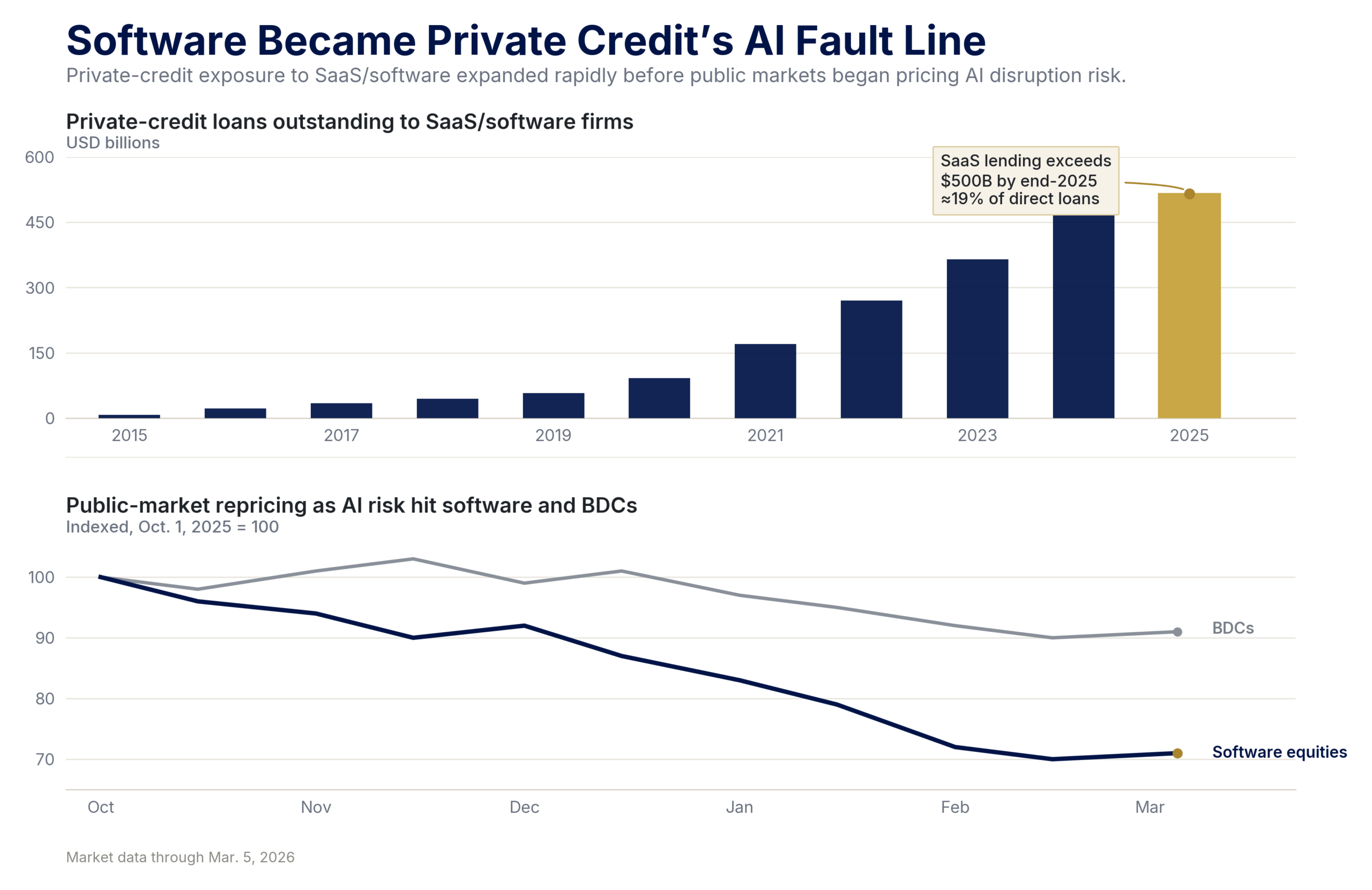

The AI story and the private-credit story intersect most directly at the sector level. Research from the Bank of International Settlements found that private-credit lending to software companies grew from a small niche a decade ago to more than $500 billion by the end of 2025. Software has become the single largest sector in private-credit portfolios.

That shift has carried real implications. Software companies aren’t traditionally thought of as leveraged-credit candidates. They generate relatively predictable recurring revenues, have low capital intensity, and have limited physical collateral. This has been key to attracting private-credit lenders seeking stable cash flows. AI disruption has begun to challenge the recurring-revenue assumptions that made software an attractive borrower in the first place.

Private credit’s exposure to software expanded rapidly just as AI began challenging the recurring-revenue assumptions that made the sector attractive to lenders. Source: BIS Quarterly Review, March 2026; BIS, “Private credit’s software lending meets AI disruption.”

Software equities fell approximately 30% between October 2025 and February 2026 as markets absorbed the implications. Business development company stocks fell around 10% over the same period, and discounts to reported net asset values deepened. The Fed’s own report noted that investor sentiment in private credit deteriorated after high-profile defaults and growing concern that AI could reshape entire industries, particularly software. The link between public AI sentiment and private-credit marks is imperfect and lagged. It’s also real.

Near-term stress indicators are trending in the same direction, though they remain short of crisis levels. Moody’s estimated the 2025 direct-lending default rate in a range that reflects uncertainty about how to classify distressed debt exchanges. More than 10% of private-credit loans, according to MSCI data, had been marked below 50 cents on the dollar. Fitch revised its outlook on Goldman Sachs BDC to negative after non-accrual rates rose and a growing share of interest payments came in the form of additional debt rather than cash. These are not crisis numbers. They are the kind of early deterioration in an opaque market that accumulates silently before it appears in aggregate reported defaults.

Oil Pressure Enters the Credit Cycle

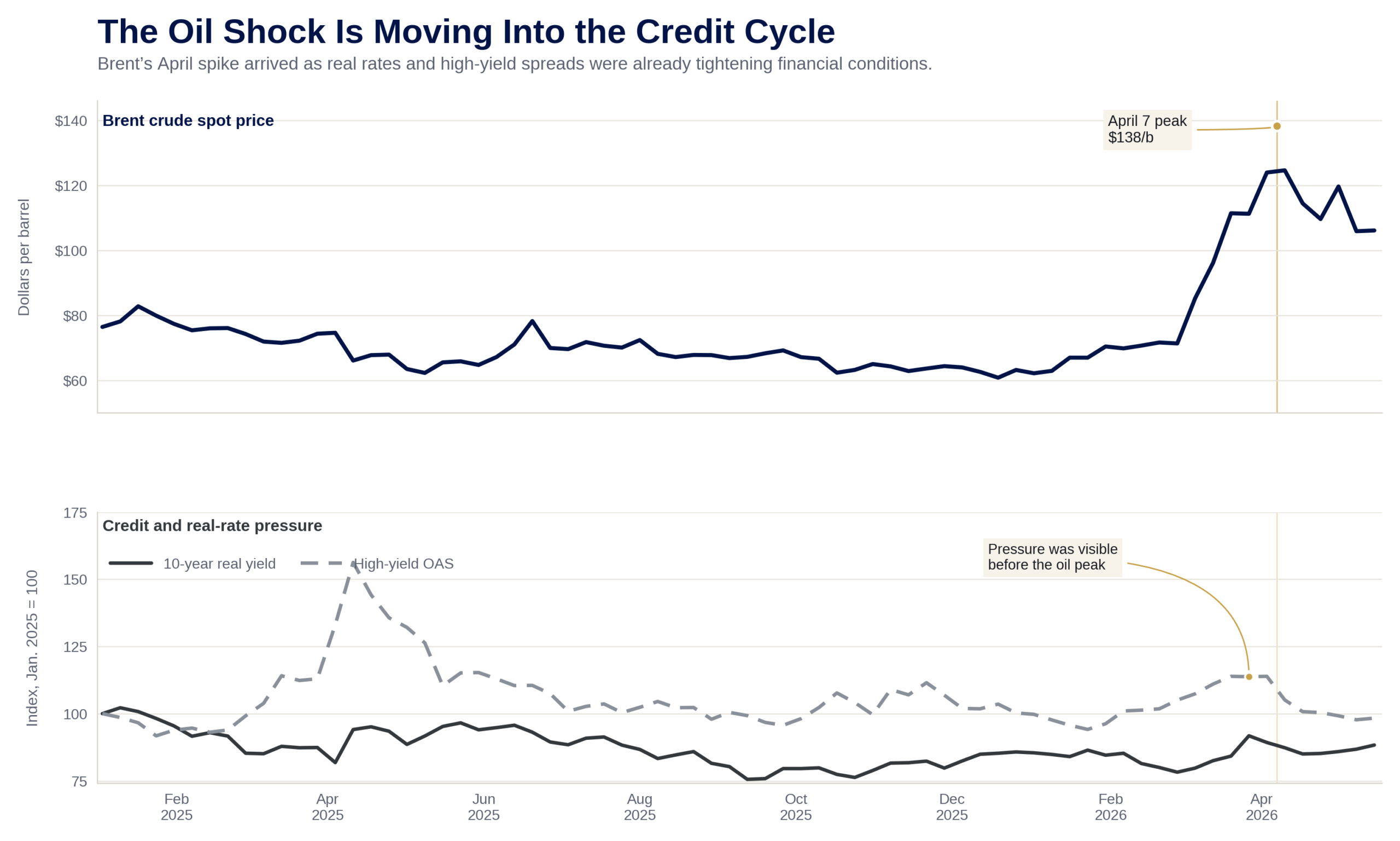

Oil adds a dimension that other risks alone don’t have. Brent crude reached $138 per barrel on April 7 before pulling back, according to the EIA’s Short-Term Energy Outlook. The EIA expects prices to average around $106 through early summer, then decline in the second half of the year. A sustained closure of the Strait of Hormuz, the EIA noted, could push near-term prices roughly $20 above those projections.

Higher fuel costs move quickly into household energy bills, transportation expenses, and business input costs. Higher real rates then compress equity multiples at the same moment that floating-rate private-credit borrowers face rising debt-service burdens. In the IMF’s April 2026 World Economic Outlook adverse scenario, an oil shock of that size lifts inflation expectations, widens corporate credit spreads, and pushes the U.S. policy rate path above baseline. Earnings and valuation assumptions face pressure from both directions at once.

The oil shock matters because it does not hit valuations in isolation. Higher energy costs, real rates, and credit spreads can tighten financial conditions at the same time. Source: U.S. Energy Information Administration, Short-Term Energy Outlook; FRED, ICE BofA U.S. High Yield Option-Adjusted Spread; FRED, 10-Year Treasury Inflation-Indexed Security yield.

Philip Lane, the European Central Bank’s chief economist, warned that “an abrupt repricing of frontier AI valuations could generate spillovers into the euro area financial system.” Stress in AI-linked debt and private-credit markets, he added, could reach banks and nonbank financial intermediaries through channels that are difficult to fully anticipate in advance. The IMF’s April 2026 Global Financial Stability Report described stretched valuations and concentration in AI-related firms as a material downside risk. Rising borrower stress combined with growing retail exposure could test the resilience of private-credit structures under adverse conditions, the report warned.

When Separate Risks Move Together

The combined risk is what matters most. An AI stock selloff on its own might trigger a large but manageable market correction. The losses would likely fall on investors who accepted high valuations in exchange for the chance of big growth. A private-credit slowdown by itself might stay mostly inside the funds that hold those loans. An oil shock by itself would mainly be an economic problem. But when all three happen at the same time, the risks begin to connect. That’s what makes the situation more dangerous than it may look in isolation.

The chain reaction isn’t guaranteed, but the path isn’t hard to see. Falling stock prices reduce the market’s appetite for risk. Higher real rates make debt harder to service while also putting pressure on valuations. Private-credit portfolios tied to software and AI infrastructure are beginning to look weaker as investors question the assumptions underlying them. Retail-facing credit funds face more redemption pressure and may limit withdrawals. Banks and insurers face more strain through credit lines, guarantees, and risk-sharing deals. Credit becomes harder to get for smaller borrowers. Household financing conditions tighten.

Those effects can move through the economy before anyone notices enough to make a change. Companies may slow investment. Hiring may soften. Lenders may pull back. The damage can spread quietly before it becomes obvious.

The FSB’s May report warned that regulators still don’t have a clear enough view of private credit. They lack consistent data on leverage, liquidity gaps, insurer exposure, borrower cash flow, and cross-border links. The IMF and BIS have reached similar conclusions.

Better data is the first step. Stronger oversight of private-credit funds sold to retail investors would also help. So would more careful valuation practices, regular stress tests, and clearer warnings about redemption limits and illiquidity risks. These steps wouldn’t be about controlling stock prices. They would be about making sure regulators can see stress as it builds, rather than figuring out what went wrong only after it has already spread.

Diversification Without Certainty

For investors, this raises a simple question. Many portfolios are built on the idea that the biggest companies are also the safest long-term places to hold wealth. That idea worked well when interest rates were low, credit was easy, and growth looked steady. It feels less safe when many of those same companies depend on one major story, AI, and are borrowing more money to fund it.

If rates stay high and oil keeps pushing inflation higher, pressure could come from several directions at once. Stock valuations could fall. Borrowing costs could rise. Credit could become harder to get. Even the strongest companies may start to look less like safe anchors and more like part of a larger market risk.

Precious metals don’t depend on a tech company’s earnings, a borrower’s ability to refinance, or private credit markets staying calm. They’re not someone else’s promise to pay. That matters when the Fed, the FSB, the BIS, and the IMF are all warning about risks that may build on each other during stress.

Gold and other precious metals aren’t perfect. Their prices can swing and be affected by real interest rates. But the case for owning them isn’t about certainty. It’s about balance. Many portfolios today are more concentrated, more connected, and more dependent on a small group of companies than investors may realize. Holding assets outside that chain may offer a measure of independence when confidence in the system becomes harder to trust.