By Preserve Gold Research

In March, billionaire investor Ray Dalio declared that the United States just experienced its “Suez moment.” The phrase carries weight because it points to more than a single military event. Dalio was describing a larger test of American power, one that asks whether the country’s financial credibility and strategic authority can hold together when both are tested at a critical chokepoint.

The Strait of Hormuz is where his argument becomes real. EIA data shows oil flows through the strait averaged 20 million barrels a day in 2024, roughly one-fifth of global petroleum liquids consumption. About one-fifth of global LNG trade passed through it, mostly from Qatar. That volume gives Hormuz enormous economic weight. When a waterway this important comes under pressure, the effects often show up quickly in oil prices, shipping costs, insurance premiums, and inflation expectations. For countries that depend on imported energy, it becomes a direct economic risk.

Dalio’s thesis is that a failure to guarantee passage would send a clear signal to allies and creditors. It would suggest that the U.S. can no longer fully enforce the commercial order that supports the dollar and its global commitments. He wrote that when a dominant power is “overextended financially” and shows weakness at a strategic trade route, “allies and creditors” begin losing confidence. Debt assets get sold, the currency weakens, and gold strengthens relative to paper assets. His assertions deserve a closer look because of the history they invoke and the data behind them.

What Suez Did to Britain, and Why It Still Resonates

The Suez crisis began in July 1956, when Egyptian President Gamal Abdel Nasser nationalized the Suez Canal Company. Britain and France, working in secret coordination with Israel, launched a military intervention. State Department records show the Eisenhower administration opposed the attack.

Without American backing, sterling came under immediate selling pressure. Britain lost $102 million in gold and dollar reserves in a single week, according to a November 1956 memorandum in the Foreign Relations of the United States. Total reserves had fallen to just over $2 billion. The same memo warned that without outside aid, Britain faced a “most serious financial crisis” and cautioned that sterling “would probably never recover” as an international currency if confidence collapsed.

Britain didn’t collapse. It remained wealthy, democratic, and militarily active in NATO for decades afterward. What it lost was something subtler and more permanent. It lost the ability to act independently at the points where the empire still required judgment, unless Washington approved first.

The years that followed bore that out. Defense spending was cut, and sterling was devalued in 1967. The empire wound down faster than British planners had expected. The financial impact didn’t show up in a single announcement. It showed up as a series of retreats from commitments that could no longer be funded at scale.

An IMF study of the crisis noted that Britain needed emergency financial support and that Washington’s stance mattered because sterling was already under intense strain. Suez wasn’t settled by force alone. It became a confidence run that made an existing vulnerability impossible to ignore.

That’s the structural parallel Dalio is drawing. The US doesn’t need to repeat Britain’s experience step by step for the warning to matter. The deeper issue is the mismatch between inherited strategic commitments and the fiscal room to honor them. That’s what Suez exposed for Britain. The pressure had been building for years before 1956 made it visible. That historical frame matters because the modern version of the problem begins with fiscal capacity.

America’s Debt Load Is Narrowing Its Options

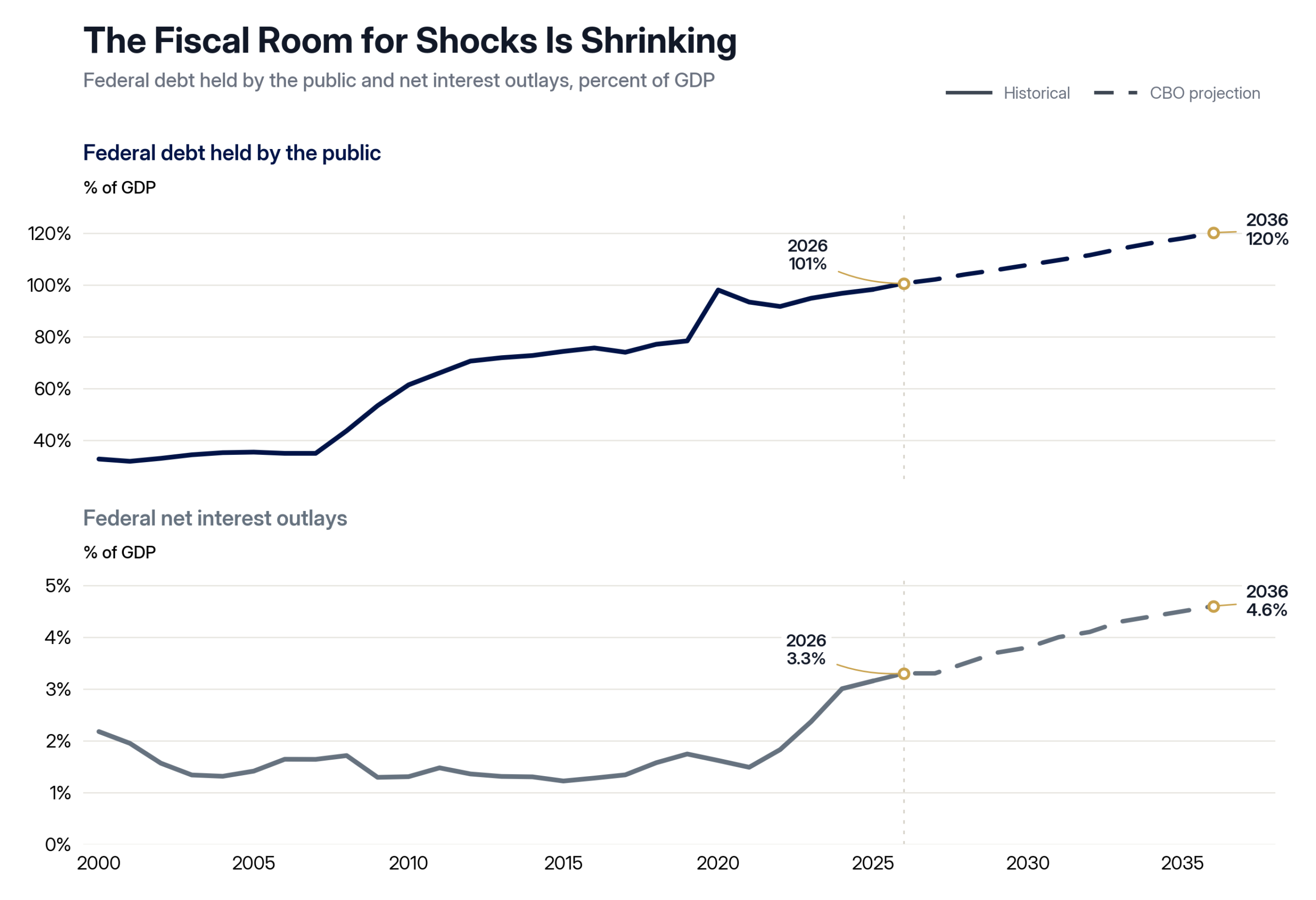

Start with the numbers. The CBO projects that federal debt held by the public will rise from 101% of GDP in 2026 to 120% by 2036, surpassing the historical record set in 1946. The annual deficit is projected to grow from $1.9 trillion to $3.1 trillion over the same period. CBO Director Phillip Swagel described the trajectory as “not sustainable.” Net interest on the debt alone would rise from $1.0 trillion in 2026 to $2.1 trillion by 2036. Treasury data showed total public debt outstanding at $39.3 trillion or more in late June 2026.

Debt is already near historic highs, but the sharper constraint is the interest bill rising with it. The risk is that every new geopolitical commitment arrives with less budgetary slack. Source: CBO, The Budget and Economic Outlook: 2026 to 2036; FRED/OMB, Federal Debt Held by the Public as Percent of GDP and Federal Outlays: Interest as Percent of GDP.

At $2.1 trillion, net interest would consume more than every major discretionary spending line combined. When debt service, defense outlays, and domestic obligations compete for the same constrained budget, the tension becomes acute. Geopolitical threats don’t arrive at convenient fiscal moments. They compound the pressure that’s already there.

The U.S. borrows in its own currency, and the dollar’s depth in global markets gives it options Britain never had. But debt on this scale shrinks the margin for error. Every geopolitical shock costs more to absorb. Every inflation flare-up is harder to contain without triggering a market reaction. Every rise in long-term rates bites more deeply into the federal budget. The IMF’s April 2026 World Economic Outlook warned that rising defense outlays, persistent inflation pressures, and high public debt could weaken growth and destabilize financial markets. Those risks tend to compound when they arrive together.

Many American households feel some of this already. Mortgage rates, small-business lending, and municipal bond financing have reflected a geopolitical and fiscal risk premium that wasn’t visible in the decade before 2022. That premium isn’t catastrophic, but it’s structural, and shows no signs of reversing. It’s also the point where Dalio’s warning becomes strongest, and where the analogy needs further explanation.

Where Dalio Is Right and Where the Analogy Strains

Dalio is strongest when he describes the feedback between fiscal and strategic pressure. The IMF’s April 2026 outlook found that defense buildups typically raise fiscal deficits by roughly 2.6 percentage points of GDP and push public debt up about 7 percentage points within three years. Wartime shocks produce larger debt jumps and sharper cuts to social spending. If the U.S. faces compounding defense requirements across multiple theaters while running a $1.9 trillion annual deficit, those dynamics stack.

The 2024 report of the Commission on the National Defense Strategy was blunt. It said the United States faces “more, and vastly more serious, challenges” than at any point since the Cold War. The commission warned the U.S. “could in short order be drawn into a war across multiple theaters with peer and near-peer adversaries, and it could lose.” That’s a preparedness assessment from analysts with full classified access, not advocacy rhetoric.

Where the analogy breaks is in the structural comparison. Britain in 1956 was operating beneath an overseeing power that could deny support and accelerate the crisis. America faces no equivalent. No friendly creditor sits above it in the hierarchy. The dollar also remains far more entrenched than sterling ever was. ECB researchers noted in 2023 that there was “no significant evidence” that geopolitical fragmentation had reduced aggregate demand for major reserve currencies, and concluded the reserve market still showed strong inertia effects favoring the dollar. There is still “no obvious alternative” to deep, liquid U.S. dollar debt markets.

How a Hormuz Shock Reaches Every U.S. Household

The United States imported only about 0.5 million barrels a day of crude through Hormuz in 2024, roughly 2% of domestic petroleum consumption, the EIA reported. That gives the U.S. insulation protection from a direct supply cut. About 84% of crude and condensate moving through the strait went to Asian markets that year, along with 83% of LNG. A sustained disruption would hit China, Japan, South Korea, and India first and hardest.

But global oil prices don’t stop at national borders. When energy prices spike, the signal moves through freight rates, airline fares, petrochemical inputs, fertilizers, and manufactured goods. A food-aid organization shipping supplies through the region pays more per gallon of diesel. A Midwest manufacturer using chemical feedstocks absorbs higher input costs. A trucking company recalculates its contract rates.

None of those firms imported a drop through Hormuz. Yet, all of them still feel the repricing within weeks. It happened in 2022, when energy prices spiked after the Russia-Ukraine war and the inflationary shock spread across supply chains faster than energy consumption data predicted.

That’s why Dalio’s argument focuses on price-setting authority rather than American energy dependence. A dominant power doesn’t have to import most of a commodity directly to be exposed when its influence weakens in the waterway that helps set the world’s price for that commodity. Asia’s dependence is what makes Hormuz a global pressure point. A global pressure point is, by definition, everyone’s problem. The same logic shows up in reserve behavior. Countries don’t have to abandon the dollar to start hedging against a more fragmented system.

Reserve Managers Are Already Hedging at the Margin

The ECB’s June 2026 report on the international role of the euro is worth a close read. Central banks are increasing gold holdings “amid persistent geopolitical tensions,” and some countries are advancing alternative cross-border payment systems. The ECB’s press statement said these trends “highlight growing fragmentation in the international monetary system.” The same report noted that the outbreak of war in the Middle East coincided with a surge in activity on China’s Cross-Border Interbank Payment System, suggesting geopolitical shocks are nudging some payment flows toward non-Western channels.

None of this means that the dollar will be replaced soon. IMF COFER data showed the dollar still accounted for 56.77% of allocated global foreign exchange reserves in Q4 2025, versus 20.25% for the euro and 1.95% for the renminbi. In a 2024 speech at Stanford, IMF First Deputy Managing Director Gita Gopinath said that despite rising geopolitical risk, “the U.S. dollar remains dominant.” She pointed to SWIFT data showing the dollar accounting for more than 80% of trade finance. Treasury data for April showed foreign investors increasing holdings of long-term U.S. securities by $206.0 billion in a single month. Foreign official institutions accounted for $41.6 billion of that total.

The ECB also noted that gold’s share of total official reserves had reached 27% at the end of 2025, broadly on par with the euro’s share in allocated reserves. The agency was blunt about the limitations. Much of that shift reflected gold’s rising price, not large-scale portfolio restructuring. Adjusted to end-2023 gold prices, U.S. Treasuries still held a markedly larger share of reserves. Still, the ECB explicitly linked the accumulation trend to hedging against geopolitical risk.

Why the Realistic Risk Isn’t World War III

When a strategic challenge gets framed as the start of imperial decline, the conversation can quickly jump to “World War III.” That reaction is understandable, but it also points readers toward the wrong frame.

The IMF’s April 2026 outlook laid out three possible scenarios. In a limited conflict, world growth slows to 3.1% in 2026. In an adverse scenario with sharper energy price increases and tightening financial conditions, growth falls to 2.5%. In a severe scenario in which energy supply disruptions persist and financial conditions tighten sharply, growth declines to 2%, and inflation exceeds 6%. None of these requires a formal declaration of war. The economic damage arises from price shocks, elevated borrowing costs, and trade disruptions.

Stockholm International Peace Research Institute reported that world military expenditure already reached a record $2.887 trillion in 2025, the eleventh consecutive year of increase. Governments don’t usually allocate at that scale because they expect stability. They’re pricing a more dangerous environment.

Dalio’s mechanism, described in his Hormuz essay, is more incremental than a clean military defeat. He describes a chain of pressures where one crisis strains a navy, another depletes missile inventories, another pushes energy prices higher, another divides allies, and another widens deficits.

At some point, the balance sheet becomes part of the battlefield. Gopinath has separately estimated that, in an extreme trade-fragmentation scenario, global output losses could reach 7% of world GDP. That’s depression-scale damage without a formal world war.

For American households, that slower scenario may prove nearly as consequential as any single event. The pressure would come through everyday costs: higher prices, more expensive borrowing, and weaker real income growth. By the time it looks like a crisis, much of the damage may already be built into household budgets.

What This Means for Portfolios and Long-Term Savings

Energy is the most immediate transmission channel. The U.S. may have limited direct exposure to crude moving through Hormuz, but American households and businesses are still exposed to global oil price volatility. Utility bills, fuel, freight, and food costs all carry an energy component. If major sea lanes become less reliable, that uncertainty can move into consumer prices and stay there. Businesses that once treated energy spikes as temporary may start building that risk into contract rates and lease adjustments.

Rates are the second channel, and they’re already visible. CBO shows federal interest expense consuming an increasing share of the national budget over the next decade. In a high-deficit, geopolitically stressed environment, long-term borrowing costs can remain elevated even while the dollar stays dominant. That has been the experience since 2022. The fiscal and geopolitical premium on long-duration assets only has to persist to keep pressure on borrowing costs, valuations, and household balance sheets.

Reserve managers are acting on a similar concern. The World Gold Council reported that official-sector gold purchases totaled 863 tonnes in 2025. Central banks added 244 tonnes in Q1 2026 alone, the fastest pace in more than a year. The ECB links these purchases to balance-sheet resilience efforts and geopolitical risk hedging, including the risk that financial assets held abroad can be immobilized overnight. Russia’s foreign reserves made that risk real in 2022.

The point isn’t to treat gold as a bet on collapse. It is to recognize why major institutions are adding assets outside the conventional financial system at a time when geopolitical risk has changed. Reserve managers are making those decisions with national balance sheets in mind. Individuals looking at the same environment are not dealing with the same scale, but they are weighing the same basic facts. A measured allocation to assets less dependent on smooth financial intermediation can be a reasonable response to genuine fragmentation risk.

The United States isn’t Britain in 1956. It has deeper markets, a stronger currency, broader alliances, and energy self-sufficiency that Britain never had. But Dalio’s warning still points to a real structural strain. A system built on confidence has to be maintained, and fiscal overextension makes that harder. Suez exposed that constraint for Britain. The United States is increasingly running into its own version of it.