By Preserve Gold Research

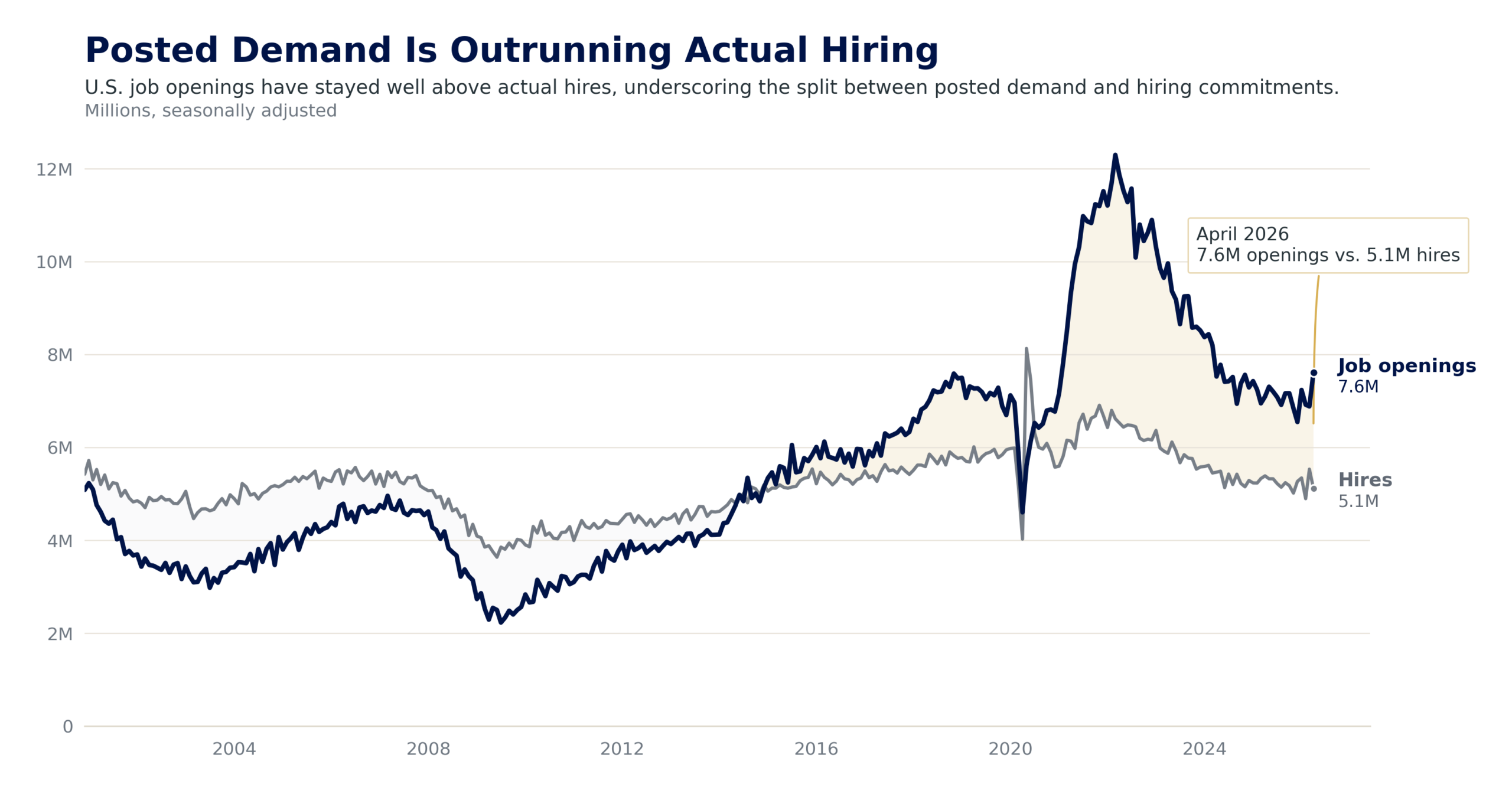

In May, the Bureau of Labor Statistics reported that 172,000 nonfarm jobs were added to payrolls, with unemployment holding at 4.3%. Three days before that report was released, the same agency put job openings at 7.6 million for April, even as actual hiring fell to 5.1 million. That gap between what employers are willing to post and what they’re willing to commit to is, in short, the current labor market story.

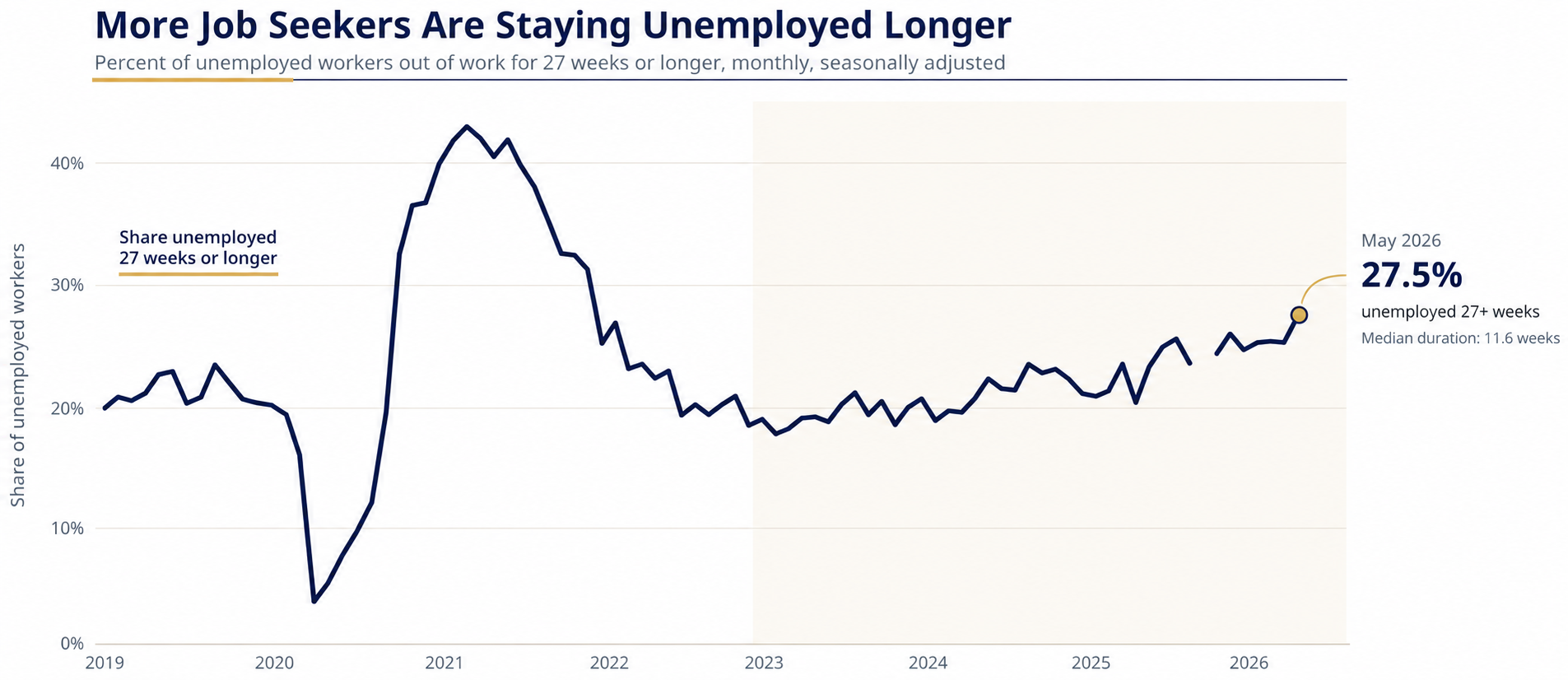

The headline number is real. So is what it doesn’t capture. Today’s market has split into two distinct groups. Workers who already have jobs are mostly stable. Workers trying to enter, re-enter, or switch are running into a system that’s slower, more opaque, and more selective than any unemployment rate implies. BLS data for May showed long-term unemployment at 2.0 million, up 524,000 from a year earlier. Median unemployment duration rose to 11.6 weeks from 9.5 weeks in May 2025. The aggregate labor market is holding. The transition back into work for many Americans is not.

The Gains Are Real. The Distribution Isn’t.

Where May’s job growth landed tells more than the total. Leisure and hospitality added 70,000 jobs, local government 55,000, with food services and drinking places driving most of the leisure gain. These are real jobs held by real workers. However, this concentration doesn’t solve the problem facing a recruiter in Chicago, a software engineer in Seattle, or a finance associate in Charlotte trying to move up or change firms.

The other side of the same BLS report is harder to ignore. Financial activities lost 22,000 jobs in May and are down 107,000 from their recent peak in May 2025. Information, professional and business services, manufacturing, and retail all showed little change. April’s and March’s counts were both revised higher, ruling out the narrative of sudden collapse. The composition of gains still points squarely away from the office-based economy most credentialed workers navigate.

For a finance associate three months into a search with no second-round interviews, or a tech program manager cycling through dozens of applications, the differences in where job growth is happening hit close to home. They help explain why the labor market can feel hostile in ways the 4.3% unemployment rate simply doesn’t reflect. The leisure and hospitality gains are happening somewhere else entirely.

Extending this view, LinkedIn’s 2026 labor market data put U.S. hiring 23% below its pre-pandemic pace overall. White-collar sectors were hit hardest, with most large professional categories running 20% to 29% below their pre-pandemic hiring levels. That breadth matters because it means the shortfall isn’t confined to one or two unlucky sectors.

The data showed a month-to-month rebound in May hiring, but the pace remained 4.8% below a year earlier and roughly 22% below February 2020. That’s not a stalled economy, but it’s one still running well below the speed many workers remember.

Indeed Hiring Lab’s April snapshot shows the split from a different angle. Postings across its platform sat just 2.4% above the February 2020 baseline at the end of April. Software development and IT roles were roughly 30% below that baseline. Healthcare postings remained well above it. If you work in acute care or parts of local government, the labor market may feel workable. If you work in white-collar digital fields, the same economy can feel broken.

The government hiring story requires careful reading, too. May’s gain came from local government, not federal. Federal employment has fallen by 348,000 since October 2024, reflecting a mix of attrition, restructuring, and hiring restraint. The practical effect follows from the scale of that decline. Experienced government workers and contractors have been entering private-sector applicant pools for policy, legal, compliance, and administrative roles that were already crowded. That adds competition in the white-collar segments where hiring was already running cold.

Openings Are Up. Actual Hiring Has Stalled.

The April JOLTS report is where the mismatch is most visible. Openings rose to 7.6 million, up 731,000 from March, the largest monthly rise since 2021. Professional and business services openings alone surged 668,000. Yet hires fell to 5.1 million. Total separations also fell.

Openings are intentions. Hires are commitments.

Employers are still posting jobs, but the conversion into actual hires has weakened. That gap helps explain why the market can look active from the outside while feeling stalled to people trying to move, re-enter, or break in. Source: FRED/BLS, Job Openings and Labor Turnover Survey: Job Openings: Total Nonfarm and Hires: Total Nonfarm.

Most job seekers experience the labor market through posted listings. They see vacancies. They see the same posting reappear three weeks later. They see “we’re growing” messaging on LinkedIn. Then they don’t get a phone screen. When budgets, demand forecasts, or internal approvals remain uncertain, employers convert requisitions into actual offers slowly. That dynamic may explain why professional and business services postings spiked so sharply while actual hiring didn’t.

Quits held at 3.0 million in April, with the quits rate steady at 1.9%. That’s not the behavior of a confident workforce. Workers are taking fewer risks in part because they know landing the next role may take considerably longer than it did two years ago. Low quit rates reinforce low hiring. Fewer people leave, fewer slots open organically, and the market for people trying to get in stays thin even as the aggregate looks stable.

In his June analysis, Cory Stahle of Indeed Hiring Lab argued that the labor market is “pulling off something that shouldn’t quite add up.” Payroll growth has stayed positive even as the hiring rate hovers near its weakest level since 2013. His explanation is simple: employment keeps rising less because companies are aggressively bringing on new workers and more because relatively few people are leaving. That’s how you end up with workers who are dissatisfied but staying, and employers who are cautious but posting.

How the Job Count Rises Without Much Hiring

When turnover slows, fewer positions open organically. Existing workers don’t leave, so fewer slots appear, and the market for people trying to get in stays thin even as the aggregate count inches higher. The labor market can simultaneously look stable from above and feel static from within.

Low layoffs anchor the headline unemployment rate. The April JOLTS report showed layoffs and discharges little changed at 1.7 million, with a layoff rate of 1.1%. That’s genuinely good news for people with stable jobs. But it offers nothing to the person who’s been out of work for six months, or the one waiting on a posting that never turns into a call.

Laura Ullrich of Indeed Hiring Lab described May as “one strong headline, but two realities.” Subdued separations keep the aggregate from deteriorating. They don’t help the people stuck outside the gate.

One detail from the April JOLTS that Stahle surfaced in a separate analysis clarifies this. Job openings at establishments with 5,000 or more employees were 81% above pre-pandemic levels in April. But those large employers account for a small fraction of all JOLTS openings. Roughly 90% of openings are tied to employers with fewer than 1,000 workers. Large firms can post loudly. Smaller and midsize employers still do most of the real hiring, and their pace hasn’t moved.

A hiring manager watching applications per role triple while her headcount budget stays flat is caught in the same dynamic from the other side. She sees the posted demand. She also sees the internal approval process slow down whenever the macro environment becomes ambiguous. The openings stay open. The hires don’t happen.

The New York Fed’s March Survey of Consumer Expectations labor module captures how this affects household behavior. The share of respondents who’d searched for a job in the previous four weeks fell to 22.5%. The expected likelihood of moving to a new employer dropped to 9.7%, the lowest reading since March 2021.

The same survey found the average reservation wage, the minimum someone would accept to take a new job, rose to a record $84,762, with the largest increases among college-educated respondents. People are less willing to move, and more expensive to move cheaply.

Those trends fit together. When mobility feels risky, workers demand more to take the risk. The threshold for leaving a decent but limiting job rises when the alternative is a long, uncertain search. That’s how you end up with workers who are dissatisfied but staying, and employers who are cautious but posting.

White-Collar Fields Are Stuck in Slow Hiring

“White-collar recession” overstates the macro picture. The labor market as a whole isn’t in recession. But many credential-heavy occupations are living through an extended drought. The BLS payroll report didn’t show a broad white-collar collapse in May so much as stasis. LinkedIn and Indeed fill in what the headline misses. Professional services, technology, information, media, human resources, and finance are all operating at hiring rates that appear considerably weaker than the national unemployment rate suggests.

For recent graduates, the slope is steeper. The New York Fed’s college labor market tracker put unemployment among recent graduates at about 5.7% in the first quarter of 2026, with the underemployment rate at 41.5%. The first rung of the professional ladder has gotten more crowded.

A separate New York Fed media advisory showed the unemployment rate for graduates aged 22 to 27 was 5.6% in March 2026, up from 3.6% in March 2019. Those numbers don’t mean college stopped mattering. They do, however, show how sharply the entry-level job market has shifted from the pre-pandemic baseline.

At 41.5%, underemployment is hitting young job seekers in ways many never anticipated. It’s a finance major managing spreadsheets at a staffing agency. Or an economics graduate driving for delivery apps while building an application portfolio.

These cases don’t show up as unemployment. They show up as suppressed wages, delayed career trajectories, and student loan pressure on households that expected higher earnings with a college degree. They also show up in rental markets, in delayed household formation, and in buying patterns that fall short of what the education investment implied. The macro data doesn’t capture that directly. The consumer spending data eventually will.

A 27-year-old with a finance degree applying for analyst roles in New York is feeling this firsthand. More applications, fewer responses, longer timelines, and competition from experienced candidates quietly displaced from contracting sectors. The credential still matters over a long career. Yet, in a market with low churn and cautious hiring managers, it does less to separate candidates in the near term than it did when white-collar hiring was expanding.

The emotional weight of this moment stems from the gap between what people were told to do and what the labor market now rewards. Many of those struggling did exactly what they were told to do: earned degrees, held internships, learned digital tools, moved to expensive cities. Then the labor market shifted from one that rewarded movement to one that rewards incumbency.

Remote Work Weakened the First Rung. AI Is Removing Entire Parts of It

New York Fed researchers Natalia Emanuel, Emma Harrington, and Amanda Pallais found that remote work explains 64% of the post-pandemic rise in unemployment among young college graduates. Their analysis traced the cause to a direct cause. Mentoring and training inexperienced workers is harder on distributed teams. When remote arrangements became the norm, firms grew more reluctant to bring on workers who required hands-on training.

That matters because the entry-level labor market was already weaker before generative AI came along. The first rung of the professional ladder had been damaged by remote work, slower onboarding, and reduced tolerance for training costs. AI didn’t create that problem on its own.

But AI is now deepening it.

The clearest risk isn’t that every junior role disappears overnight. It’s that companies start needing fewer of them. Entry-level work has always included substantial routine drafting, research, customer support, reporting, scheduling, screening, and coordination. Those are the tasks companies are now trying to automate, compress, or push onto smaller teams with AI tools.

Amazon, among a growing list of other major corporations, hasn’t shied away from the shift. CEO Andy Jassy said, “I do believe that a lot of the jobs that we’ve thrown human beings at for the last 20 or 30 years, you won’t need as many human beings doing those same jobs.” Klarna has already shown what that can look like in a specific function. Its AI assistant handled the equivalent of hundreds of customer service agents’ work. Even if some of that work still requires human oversight, the staffing model changes once software can absorb a large share of the volume.

AI belongs in the labor-market story as it’s not just reshaping how people apply for jobs. It’s changing how many jobs companies believe they need, especially in areas built around repeatable information work. A company doesn’t have to announce mass layoffs for AI to weaken the opportunity. It can leave roles unfilled, combine two junior jobs into one, slow backfills, reduce support headcount, or expect existing employees to cover more work with AI assistance. The result is a labor market where the first rung isn’t only harder to reach. In parts of the white-collar economy, it’s being rebuilt with fewer people.

What Reduced Mobility Means for Household Finances

A positive payroll number no longer signals a fluid market. Stable unemployment no longer says much about the ease of changing employers. Rising openings no longer mean firms are matching quickly. The country can keep producing decent aggregate headlines while a growing share of workers experience the labor market as a bottleneck.

The second-order effects of that weakening are starting to show in spending patterns. Households that feel stuck in their current employment situation often cut back on discretionary purchases, delay major investments, and save more defensively. That behavior doesn’t require a recession to develop. It only requires the perception that mobility is limited, and the upside is harder to reach.

The risk in today’s low-hire, low-fire environment is a reduced cushion. When hiring is already running near 2013-era lows, there isn’t much room to absorb a rise in layoffs if conditions deteriorate. BLS data for May showed 27.5% of unemployed workers had been out of work for six months or more, up from 20.4% a year earlier. That’s the quiet vulnerability embedded in an otherwise respectable headline.

The unemployment rate has stayed relatively stable, but a larger share of unemployed workers are spending six months or more out of work. That is where the labor market’s transition problem becomes visible. Source: FRED/BLS, Of Total Unemployed, Percent Unemployed 27 Weeks & Over; Median Weeks Unemployed.

For the Federal Reserve, the situation has created a difficult bind. Inflation ran at 4.2% year over year in May, with average hourly earnings up 3.4% over the same period. The Fed’s June FOMC statement described job gains as keeping pace with the workforce and unemployment as little changed. As long as that holds, the central bank has limited reason to ease, even as workers feel squeezed in transition.

Borrowing costs for someone financing a home, a car, or a small business expansion remain elevated as a result. Corporate America, meanwhile, doesn’t need a wave of layoffs to produce a more defensive economy. It only needs slower decision-making, longer time-to-hire, and a workforce less willing to take risks. Those are features of the current environment.

The combination of low mobility, elevated inflation, and tighter financial conditions also changes how households may need to think about income risk. A worker earning $80,000 in a sector where hiring has slowed to a near standstill now has less protection than the salary suggests. That income has lost purchasing power in real terms, and there are fewer credible alternatives if the employer cuts headcount or restructures. The optionality that made a good job feel secure two years ago has narrowed.

A worker who can’t easily change employers or sectors carries an exposure that doesn’t appear in any national statistic. Income becomes less mobile. The longer someone stays in a sector that’s quietly contracting, or waits too long on a job search, the harder the recovery tends to be. Emergency savings and manageable debt remain the conventional answer to that risk. Experts tend to agree that they’re still important. But this environment also points toward something wider: holding assets whose value isn’t tied to a single employer, sector, or hiring cycle.

Institutional investors have already been moving in that direction. The World Gold Council’s full-year 2025 report put total gold demand above 5,000 tonnes for the first time on record. Investment inflows reached historic levels, while official-sector buying remained elevated. Central banks purchased 863 tonnes, the fourth-largest annual expansion of official reserves on record and more than double the pre-2022 annual average. That level of accumulation points to a clear view. When the headline economy looks stronger than the lived experience underneath it, hard assets with no counterparty exposure offer a different kind of resilience.

May’s 172,000 jobs were real, and subdued layoffs are genuinely good news for the employed. But the underlying weakness, concentrated in white-collar sectors, was already evident in long-term unemployment trends, near-record-low worker mobility, and historically slow hiring rates before this cycle. The current environment didn’t create the fragility. It revealed it.