By Preserve Gold Research

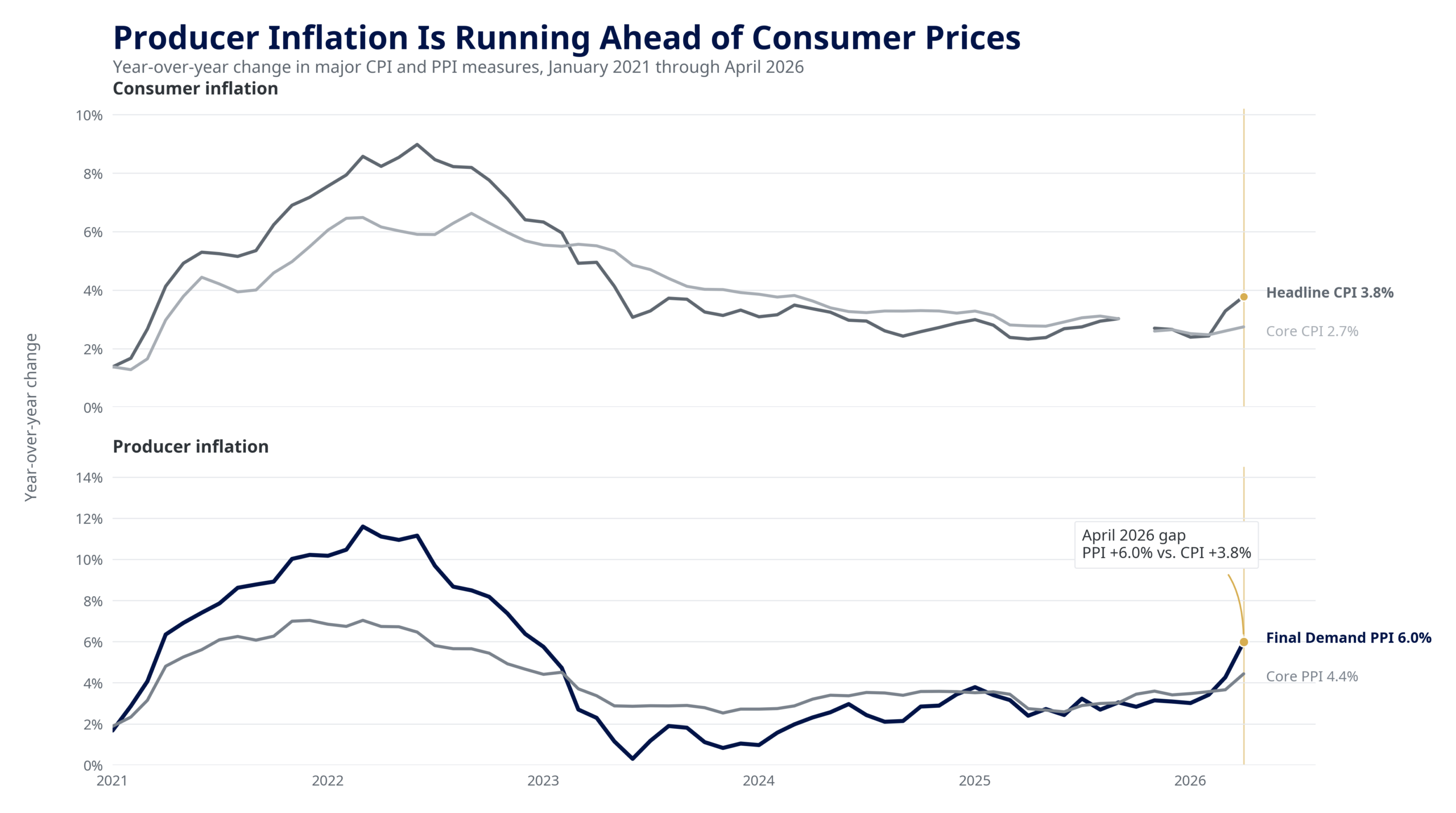

Headline consumer prices rose 3.8% in April, according to the Bureau of Labor Statistics. That’s the fastest pace since May 2023, and it came in well above market expectations after two years of gradual disinflation.

Gasoline drove a large share of the monthly increase, but the data showed inflation spreading far beyond a single category. Shelter costs climbed again. Trade services margins, the markup that wholesalers and retailers charge over their own acquisition costs, jumped sharply. Mortgage rates, already elevated by a Fed reluctant to cut, remained near multi-year highs for the fourth consecutive month.

The April report didn’t just disappoint optimists. It forced a more fundamental reassessment of the trajectory. The Federal Reserve had cut its benchmark interest rate four times between September 2024 and December 2025, lowering the target range from 5.25%-5.50% to 3.50%-3.75% over that period. Markets had largely assumed more relief was coming. Futures markets were still pricing meaningful odds of additional cuts into early 2026. Then April’s figures arrived, and those hopes were dashed.

Producer Prices Signal More Consumer Pain Ahead

Producer prices, the costs that factories, energy companies, and distributors charge before goods reach consumers, told an even more unsettling story. The BLS reported that the Producer Price Index for final demand rose 6.0% over the twelve months ending in April 2026, the strongest yearly reading since December 2022.

Final demand goods rose 7.4% year over year. Energy surged more than 22%, driven in part by a 15.6% monthly jump in gasoline alone. Trade services margins also contributed substantially to the monthly total, helping drive what the BLS described as a broad-based increase across categories. The BLS also measured the index for final demand less foods, energy, and trade services, a cleaner gauge the Fed watches closely, at 4.4% year-over-year, well above any reading consistent with price stability.

The intermediate production pipeline reinforced the same picture. The BLS reported strong acceleration across multiple production stages, with unprocessed goods for intermediate demand up 20.9% year over year. Central bankers closely watch this upstream pattern. When raw material and mid-production costs are rising faster than retail prices, it’s a signal that consumer inflation hasn’t yet absorbed the full pressure moving through the supply chain. In April, the answer was clearly no.

Producer prices have reaccelerated more sharply than consumer prices, suggesting that some cost pressure may still be moving through the supply chain rather than already showing up in household inflation. Source: FRED/BLS, Consumer Price Index for All Urban Consumers: All Items; Consumer Price Index for All Urban Consumers: All Items Less Food and Energy; Producer Price Index by Commodity: Final Demand; Producer Price Index by Commodity: Final Demand Less Foods, Energy, and Trade Services.

For households and businesses, that gap is not some abstract supply-chain detail. It shows up in the choices companies are forced to make every day. Every manufacturer, freight carrier, and retailer facing higher input costs must either absorb the margin hit or push some portion forward. Most can’t absorb indefinitely.

Diesel and fuel surcharges are already lifting delivery costs across industries from food distribution to industrial supply chains. Insurance premiums, sensitive to replacement-cost inflation in energy-linked materials and physical property, have risen in consecutive quarters. Businesses that locked in multi-year financing at post-2020 rates now face a harder refinancing environment, as short-term borrowing costs remain near the upper edge of the Fed’s target range. The inflation the PPI captures today is, for most of the real economy, the cost pressure that will appear in bills and receipts over the coming quarters.

Gasoline above $4 per gallon in most major metropolitan areas is a direct hit to disposable income, particularly for households in lower- and middle-income brackets who drive the most and carry the least financial cushion. Auto loan rates, closely linked to prevailing short-term benchmarks, have remained elevated enough that used-vehicle financing costs are near multi-year highs. Prices on used vehicles have stayed well above pre-2020 levels, compounding the strain.

For businesses that run vehicle fleets, including delivery companies, field service operations, and logistics firms, the cost structure today looks materially worse than it did 18 months ago. The housing market is under similar pressure. Mortgage rates have followed short-term rates upward, blocking refinancing for existing homeowners and pricing a meaningful share of potential buyers out of the market entirely. These conditions don’t show up in a single index reading. They build on the lived experience of the economy, and they compound.

The Fed’s Inflation Math Is Getting Uncomfortable

The core consumer price reading offered partial reassurance. The BLS measured the core CPI, which excludes food and energy, at 2.8% year-over-year in April, above the Fed’s 2% target but not by much. The more important signal is the direction. Core inflation had been cooling through late 2024 and into early 2025.

April appears to have halted that trend. The breadth of the PPI data suggests the disinflationary momentum that defined the prior eighteen months has stalled. Fed officials typically don’t react to single data points. They react to trend changes. The April combination of a reaccelerating headline, a sticky core, and PPI for final demand running three times the Fed’s target constitutes a trend change with several moving parts.

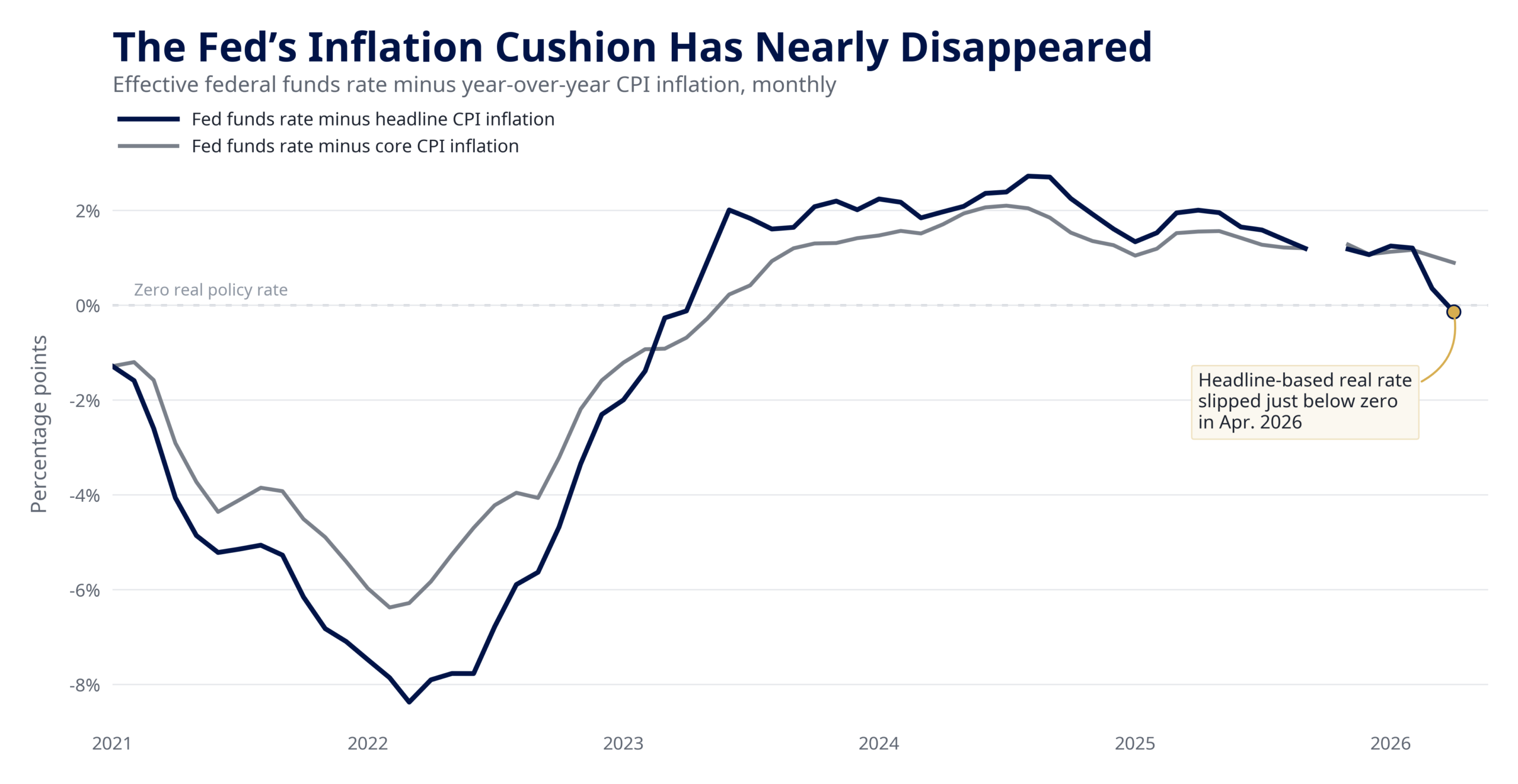

The math doesn’t look great regardless of which inflation measure is used. The Fed’s target range sits at 3.50%-3.75%, with a midpoint of 3.625%. Subtract the headline CPI of 3.8%, and the real policy rate turns slightly negative. Against core at 2.8%, it’s a modest positive. Neither reading suggests a clearly restrictive policy, especially if the Committee believes some of the current headline pressure will feed into core goods, services, wages, or longer-term inflation expectations over the following quarters.

The Fed has historically preferred to see the real rate clearly positive with some margin before concluding that policy is genuinely restraining demand. That margin is thin now, and on the headline measure it has disappeared entirely.

Once inflation is deducted from the policy rate, the Fed’s room to claim that policy is clearly restrictive looks much narrower than it did during the disinflationary phase. Source: FRED/Federal Reserve Board; FRED/BLS, Effective Federal Funds Rate, Consumer Price Index for All Urban Consumers: All Items, and Consumer Price Index for All Urban Consumers: All Items Less Food and Energy.

Fed Officials Are Now Openly Discussing Rate Hikes

The April 29, 2026, FOMC statement held rates steady, as expected. But the vote wasn’t clean. Stephen Miran dissented in favor of an immediate cut, arguing the labor market warranted relief. On the other side of the table, Beth Hammack, Neel Kashkari, and Lorie Logan supported the hold but declined to endorse statement language implying a continued easing bias.

The FOMC minutes, released three weeks later, captured the Committee’s internal evolution. A majority said some policy firming would likely become appropriate if inflation remained persistently above the 2% target. Several participants specifically raised concern that sustained elevated energy prices combined with tariff pressure could embed broader inflation expectations in a way that would be considerably harder to reverse.

That language is important because it ends the cycle’s assumed direction. For most of 2024 and 2025, the only live question at FOMC meetings was the timing of the next cut. The April minutes changed that framing. The Committee is now openly debating the conditions under which it might move in either direction, a genuinely two-sided policy stance absent from official communications for nearly two years.

Cleveland Fed President Beth Hammack had been telegraphing the shift before the April meeting. In an April 6 interview with the Associated Press, she said, “I could see where we might need to raise rates if inflation stays persistently above our target.” She noted that inflation had been above 2% for more than 5 years and described any further rise as “moving in the wrong direction, away from our 2% objective.” Her comments proved to be an accurate preview of what the full Committee discussed two weeks later.

By late May, several more officials had moved in the same direction. On May 29, Fed Vice Chair for Supervision Michelle Bowman, previously regarded as among the Committee’s more measured voices, acknowledged that persistent energy disruptions could change her thinking on rates.

Minneapolis Fed President Kashkari said it was “premature to conclude the Fed needs to be raising rates right away,” while adding that the inflation data had made him considerably more attentive to the risk that expectations could become unanchored. Kansas City Fed President Jeffrey Schmid offered less equivocation. His primary concern was an inflation rate that was “too hot and has been above target for too long.” The Committee isn’t uniformly hawkish. But it no longer operates under a shared assumption that the next move must be lower.

A New Chair Inherits a Two-Sided Committee

The leadership transition adds a separate layer of uncertainty. Powell chaired the April meeting, but Kevin Warsh was sworn in as Fed Chair on May 22, the first Fed chair to take the oath at the White House since Alan Greenspan in 1987.

At the ceremony, Warsh pledged to lead “a reform-oriented Federal Reserve, learning from past successes and mistakes.” Warsh built that reputation as a Fed governor during the 2008 crisis and the years that followed. He’s skeptical of rates held accommodative for too long, and his instincts lean toward operational discipline. Where Powell emphasized patience and data dependence, Warsh has historically favored clarity and preemption. In the context of April’s inflation readings, those instincts may be exactly what several Committee members were anticipating when they pushed for stronger language.

The formal reaction function doesn’t change overnight with a new chair, but markets have already begun recalibrating. Warsh inherits reaccelerating inflation, a Committee with active internal disagreement, and a market that spent most of 2024 and 2025 pricing further easing. His first months will involve testing from both the data and from observers seeking to understand how he weighs supply-shock inflation against any early signs of labor-market softening.

Bond Markets Have Repriced, but Stocks Haven’t

The futures market has already absorbed much of this repricing. CME FedWatch data from late May placed the probability of no change at the June meeting at approximately 99%. That part is settled. Farther out on the curve, the picture is more volatile and more consequential.

Contracts stretching through early 2027 have shifted away from pricing gradual cuts toward pricing a flat-to-modestly-tightening path. Analysts reported in mid-May that investors saw roughly a 60% chance of at least one rate increase by January 2027. CME-linked data from the same period put the probability of at least one year-end hike in a range from the high 30s to nearly 50%, depending on daily energy-market headlines. The bond market, in other words, has moved from pricing an easing cycle to pricing a prolonged pause with a hawkish tail attached.

Equities have remained surprisingly resilient through this repricing. The S&P 500 closed near 7,580 in late May, after hitting fresh record highs the previous session. The coexistence of near-record equity valuations and rising rate-hike odds is explainable, but not necessarily durable.

Market leadership has been tightly concentrated in large-cap technology, AI-related infrastructure, and dominant consumer platforms. All carry strong balance sheets, wide pricing moats, and direct exposure to demand trends that aren’t highly sensitive to short-term rate moves.

Those businesses can sustain high valuations even as discount rates edge higher, because their earnings power is less dependent on cheap financing or favorable economic conditions than the median listed company. Beneath that narrow cohort, the picture is considerably more strained.

Companies with thin margins, high energy or freight intensity, and limited ability to raise prices are already absorbing input cost pressure that the April PPI data suggests has not peaked. Many were still planning around the rate-cut assumptions that dominated market thinking through late 2025. The S&P’s resilience at record levels reflects the composition of its top-heavy index, not the breadth of corporate health.

The transmission from producer prices to equity earnings cuts two ways. If firms successfully pass on higher input costs, margins survive in the near term. But the resulting stickiness in consumer prices extends the Fed’s constraint, keeps discount rates elevated, and makes broad multiple expansion difficult.

If firms absorb costs to protect volume and competitive position, CPI may moderate faster, but earnings compress. The sectors best positioned to navigate this are those with contractual pricing that adjusts automatically, low direct commodity exposure, or brand authority strong enough to take pricing without losing significant volume. For most of the industrial, manufacturing, and consumer staples economy, the margin arithmetic over the next two to three quarters will be harder than recent earnings seasons suggested.

Three Rate Scenarios, One Dominant Tail Risk

Analysts suggest the most likely near-term path remains a prolonged hold rather than an immediate rate increase. The April minutes make clear the Committee wants more data before acting. Major institutional forecasters, including JPMorgan and UBS, both envision some portion of the current inflation shock fading if energy conditions stabilize in the second half of 2026.

JPMorgan’s baseline assumes the Fed can hold without hiking and eventually resume cutting if growth softens. UBS sees a similar path, with cuts only re-entering the picture if the inflation shock fades and labor markets weaken clearly. But the base case is now a hawkish hold, not a comfortable pause. The question for the second half of the year is whether the PPI-to-CPI pass-through broadens, whether energy remains elevated or retreats, and whether any early signals of inflation expectations drifting appear in survey data or market breakevens.

The hawkish scenario, one 25-basis-point increase by December 2026 or January 2027, carries meaningful odds based on current futures pricing, somewhere between 30% and 40% depending on the instrument and the day. In that scenario, April’s elevated PPI feeds progressively into consumer prices through distribution and services channels. Tariff-related goods prices stay sticky, and the Committee’s patience eventually runs out.

Mortgage rates, already pressing hard on housing affordability, would move higher still. Long-duration assets, highly leveraged industrial companies, and businesses with weak margin cover would face the deepest re-rating. The index-level effect on the S&P might look limited if technology leadership held, but the dispersion beneath it would be severe, and the experience of the median equity investor would diverge sharply from headline index performance.

A cleaner resolution remains possible, but it’s increasingly demanding of evidence. In that scenario, energy falls back, inflation breadth narrows quickly, and the labor market softens enough to give the Fed cover to cut. Getting there requires several favorable developments simultaneously: energy prices retreating materially, tariff-related goods pressure easing, and demand softening without triggering a recession signal that would force a different and more complicated policy response. None of those developments is visible in the April data.

The base case, a sustained hold with an explicitly revived tightening option, is itself a form of tighter effective conditions relative to what markets were pricing as recently as late 2025. When the expected policy path shifts from cutting to holding indefinitely, real financing costs rise even if the nominal rate doesn’t move.

Businesses that planned capital expenditure around the expectation of cheaper money in mid-2026 now face a different cost environment. Fixed-income instruments that priced in a yield cut must reprice toward a longer hold. The shift doesn’t require an actual rate increase to have real consequences for spending, investment, and portfolio positioning. The repricing already underway in the bond market carries its own tightening effect, even before the Fed acts.

What Prolonged Inflation Means for Real Returns

The numbers alone don’t capture the full cost of prolonged inflation. Real purchasing power—what a given dollar of savings or earnings actually buys—has eroded faster than short-term interest rates can compensate. And that gap that compounds quietly across quarters and years.

Workers who received nominal wage increases during 2024 and 2025 have seen much of those gains absorbed by energy, insurance, food, and housing costs. Savers holding cash or short-duration instruments are earning real returns that are positive on paper and questionable in practice. Businesses that passed costs through maintained margins in the near term, but did so at the expense of customers who adjusted behavior in ways those businesses haven’t yet fully registered. The inflation environment of spring 2026 is not crisis-level by historical standards. But it’s sustained enough to alter what conventional financial exposures actually deliver.

For businesses planning capital expenditures, hiring, or committing to long-term contracts, the current environment makes forward projections considerably more uncertain than they were 18 months ago. Energy costs are harder to budget around. Financing costs are harder to assume to be stable. Consumer demand, still nominally strong in technology-adjacent sectors, shows early signs of compression in discretionary categories that are more sensitive to fuel and insurance costs.

Companies with the most exposure to energy, logistics, and rate-sensitive consumer spending are already adjusting guidance, but those changes haven’t fully translated into index-level earnings estimates. The gap between winners and losers in this environment could widen before it narrows.

The practical question for anyone managing a portfolio in this environment is what it means to remain concentrated in assets whose returns depend on rates staying low, nominal growth remaining strong, or policy credibility remaining intact. For two years, those exposures produced strong results. But the April inflation data, the Fed’s own minutes, and the current futures-implied rate path all point to a period when those conditions become less reliable.

Policy guidance has become explicitly two-directional. The breadth of the current inflation signal, moving simultaneously through energy, trade services, intermediate manufacturing, and core goods, makes resolution harder to assume than a single-category shock would imply. When macro visibility narrows and real returns on conventional instruments compress, the allocation logic starts to change. Investors tend to look for assets that can hold value regardless of what central banks decide next. In that kind of environment, assets tied more directly to monetary and fiscal conditions can become harder to ignore.

The Fed hasn’t moved. The April data doesn’t indicate a crisis. But the conditions that made conventional financial exposure feel low-risk have deteriorated. Cooling inflation, a central bank committed to easing, and rate expectations anchored well below prevailing levels all look less dependable than they did before. April made that shift difficult to dismiss. What the data established, and what the Committee’s own language confirmed, is that those conditions should no longer be treated as the expected path.